Yes these start ups will not give discounts forever but habits change and a new startup will come namely xyz to compete with Uber now. At the start it was foodpanda, then swiggy came with huge discounts foodpanda is now dead, when swiggy stopped zomato turned its model from reviewing app to home delivery app, Zomato stopped a bit of discounting then here comes Uber eats, now when they will stop discounts a new player say Mr biyani or Mr Ambani will come or XYZ, the cycle will go along. Also people became habitual of discounts or home delivery they don’t worry whether its uber or swiggy.

These will be “build to sell” as if they dont do someone other start up with big funding will- not forever but atleast for next 10 years in India and I think that would be enough to take a hit on Dominoes. Just my opinion

In my view -

- Dominos has brand and aspirational appeal - its not just delivered food.

- Children like pizza more than any other food.

- The delivery experience and consistent quality of Domino’s beats others - the delivery boy cant have a bite out of your pizza and put it back without you not knowing. Domino’s in that respect has more skin in the game,.

- IMO Swiggy/Uber fills the cuisine gap of delivered Biryani and Chicken Tikka. You wont buy Pizza if you are in the mood for Biryani. This is the pie expanding.

4 Likes

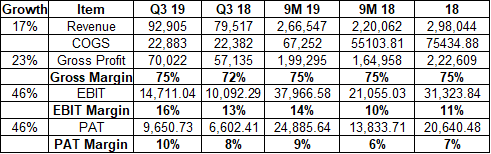

Strong set of results from Jubilant Foodworks.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/7a00c2a8-7b3b-4195-aed1-4013c4507eb6.pdf

2 Likes

In the online food ordering business, people like fewer choices and not more choices. What online food delivery apps have done is create a plethora of choices. In Behavoral Economics, this is called choice overload. In one of the most cited experiments in recent times - done by Sheena Iyengar (google the JAM experiment) - she discovered that when people are attracted to wide choices but are more likely to make a purchase when given fewer choices. Also, more choices mean less prices as you have to compensate people for the time they spend in making choices.

Here is an example of this

My sense is that Choice Overload is playing out in online food delivery and is an important tailwind for Dominos. Hence, more the competition the better it is.

Best

Bheeshma

7 Likes

Swiggy has figured out a way to capitalise on this. If you see Swiggy Access/Cloud Kitchen model, the businesses that participate have a limited set of options, are very affordable and they woo their customers by charging zero delivery for these and charge higher commissions from the restaurants. They also have their own private brands like Homely and Bowl Company in this space which run fixed menus.

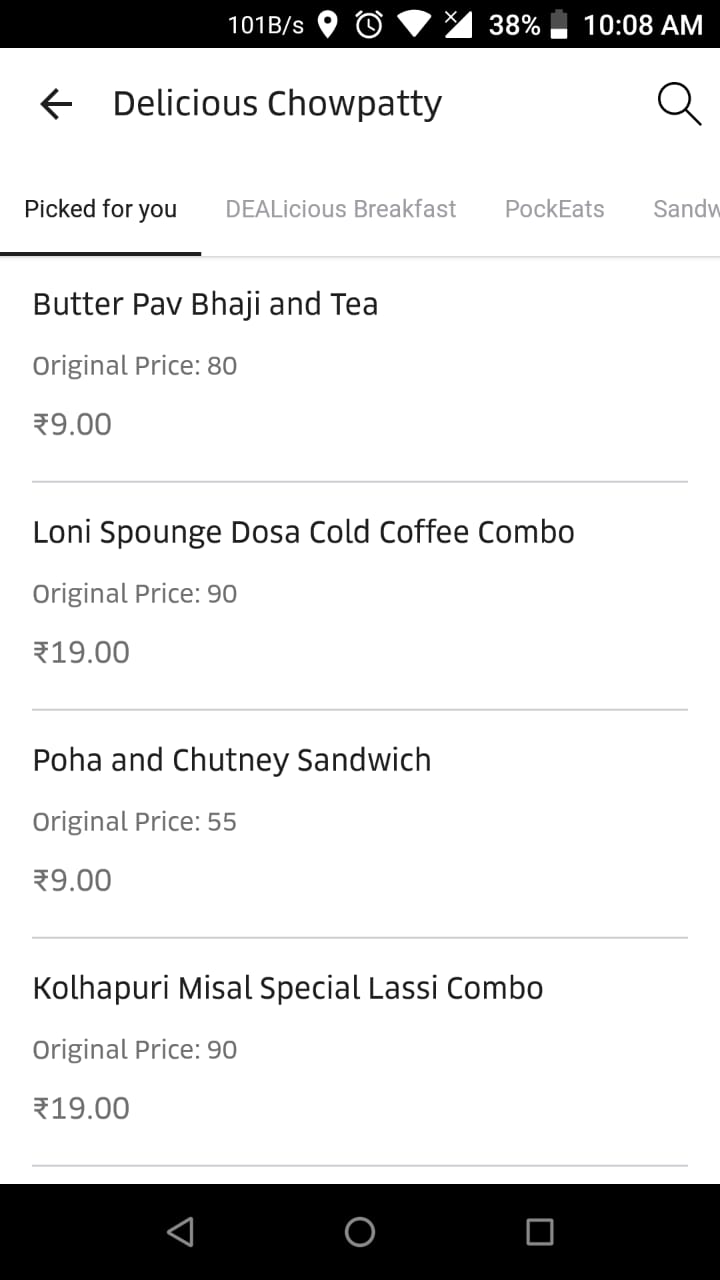

I think the Recommended section in the top works well for Swiggy. I guess most people would just go for one of the foods with appetising pictures instead of scanning the whole menu even for traditional restaurants. This whittles down the exhaustive menu to 10 highlighted items with pictures. Another thing I see from my personal behaviour is that I order 1 in 10 times that I order online, from Dominos. Earlier (Before Swiggy/Zomato) ordering food would mean Dominos 1/2 times. But the market size itself is expanding which is good for all the players.

Interestingly I almost never order through Zomato though I am invested in Info Edge  Just the fact that it takes an additional click to get to the Order workflow in Zomato I think subconsciously causes a mental block. Consciously of course Swiggy is burning more cash and so is beneficial for me as a Customer most times.

Just the fact that it takes an additional click to get to the Order workflow in Zomato I think subconsciously causes a mental block. Consciously of course Swiggy is burning more cash and so is beneficial for me as a Customer most times.

5 Likes

NAA imposed fine of 42 cr to Jubilant Foodworks .It have 600 cr cash in Balance sheet already.

Seems it is not promoter integrity issue as per this below article which published on on same notices issued to HUL.

What is your opinion on the impact ?

Not sure how these anti profiteering orders work. However, they will have to create a contingent liability for the amount

1 Like

This is unfortunate, but I wouldn’t treat this as an issue comparable to the governance issues plaguing other companies. I am sure Jubilant will appeal against this. In the worst case, this is a one-off hit.

The National Anti-Profiteering Authority (NAA) was setup because nobody knew exactly how the transition from pre-GST to GST would happen. There was no comparable precedent available, and the chaotic days of demonetization were fresh in everybody’s memory. You needed to have a stick ready to wield, if the need arose and if you found the situation getting out of hand. In reality, the transition to GST turned out to be quite smooth.

The NAA holds no relevance now and can be dissolved. Industry bodies like FICCI, CII, Assocham etc. should take it up and demand that it be abolished. It is well understood that the ultimate market price of any product is a result of complex interplay of various forces like input costs, taxes, competitive position, management strategy etc. and cannot be traced to one or the other alone.

There was no such body earlier to ensure that benefits of excise or sales tax cuts were passed on to the consumers. So why do you need one for GST now?

But until that happens, the guy sitting there needs to justify his salary (and perks).

Here is the full order:

Yes absolutely. The entire online food delivery ecosystem is a good setup for studying and understanding behavioral aspects of economics. For e.g there is now ubiquitious consensus on the fact the how people pay impacts their consumption. On one end you have Cash which makes you feel the pain of paying and at the end if you pay through digital wallets - the pain is significantly less which ends up increasing consumption. This category is well suited for these small value high consumption eating occasions

1 Like

market seems to be more worried on royalty demand by promoters not this anti profit order which is a one time thing.any views on that front

CNBC’s source based information hard to believe. They told earlier at May,18 that promoter is going to sell 10% which did not happened yet . So let us wait for Jubilant Food’s clarification on it…

Later Clarified…

fair enough lets wait for clarity

Jubilant Food approves royalty payment to founder company; to pay 0.25% of group revenue as royalty from FY20: Agencies

so its confirmed …this is bad optics

though amount involved is not much really to dent financials but still bad optics

Even Tata Sons collects 0.15% royalty from group companies using Tata name…need to see in this context…

It’s the attitude my friend, it’s the attitude.

Even Tatas came under heavy criticism when they introduced royalty. But at least the Tata name is well known across the country, has some reputation. So they had some takers for their argument.

Jubilant is not Tata, as Mr. Bhartia will discover tomorrow.

1 Like

The royalty notice stands withdrawn.

However, I think the damage has been done. The amount was too small… they could have done it in a better way… they do not withdraw salary. They could have taken salary, performance based… no one would have an issue but royalty for no brand???

If they want to take royalty for Jubilant as a brand then they have to show that they can sell on name of Jubilant. No one outside stock markets know them as Jubilant Foodworks, everyone says Domino’s Pizza… Never heard anyone say let’s eat Jubilant’s Pizza…

Disc: Not Invested

3 Likes

The intention of Promoter may be not a wrong one but the way they chose to convey is really not appreciated & does not go well with me in specific.

I always have a fascination & ground rule to be associated with Quality businesses with ethical Managements & 80% of my conviction on a business is on the Jockey & in this case it is on Mr Pota, the way he drastically changed the fortunes of Jubilant Foodworks, after his arrival, around 2 years which is clearly visible in past straight 6-8 Quarters.

Within a short span of 8 hrs there comes 2 Press releases to the exchanges which clearly challenges my own conviction.

Business may still do well, no doubt but I prefer to be sleeping peacefully.

Also it demonstrates either the Independent Directors did not do justice initially by questioning the Promoters on this immature & hasty decision making & both the boards (not 1 only)-Jubilant Foodworks & Jubilant Lifescience first approved the decision.

Later for just a meager amount of 8 odd Crs (on FY 18 Consolidated Sales Basis) as a royalty payment proposed to start from FY 20 (i.e April 2019) Promoters realize (after wiping off 850 Crs of MCap in a single day) their mistake & revert the decision by releasing another Press Release to exchanges to at least contain the further damage it would have continued today as well.

They would have done it more transparently by either taking the Salary or may be announcing any Performance Linked incentive or bonus for themselves which would have been well accepted by Markets & would have not raised an iota of credibility loss or doubt in minds of Investors, who were on a selling spree & brought it down during the Market to a level of 13% at one time, with still some recovery at closure.

13 Likes