From time to time these things keep happening. There was the Maggi controversy some time ago. Pepsi, Coca Cola, McDonald’s, KFC - all of them face variety of allegations all the time. There is no need to worry about such videos.

3 Likes

Its not only pizza…we have chowmein, burgers, Mccain products like smilies , samosa, mithai…choclates…pastry…cakes…its difficult to stop kids/young ones from consuming them…infact I have rarely seen kids parties happening without a pizza or burger…its a growing trend per my limited knowledge.

1 Like

HSBC has maintained ‘hold’ rating on Jubilant FoodWorksNSE 0.60 % and raised target price to Rs 2,600 from Rs 1,640. The firm said Jubilant FoodWorks’ exceptional success in turning around the same store sales growth and profitability has catapulted it into a solid growth story. Jubilant trades at FY20 EV/ EBITDA of 22 times, which still appears significantly below the other structurally attractive network rollout stories such as Titan and Avenue Supermarts.

Read more at:

//economictimes.indiatimes.com/articleshow/63874632.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

1 Like

In a dramatic twist to the ‘fake BBC video on Domino’s’ that went viral on social media last week, Jubilant FoodWorks on Monday filed a First Information Report (FIR) in Noida against Eeshaan Kashyap, who allegedly impersonated in the viral video as Domino’s chef.

“The accused person makes multiple false accusations against Domino’s and gravely harms the reputation by way of his impersonation and illegal act and conduct of forgery and cheating,” Jubilant states in the FIR, a copy of which was reviewed by Forbes India. Kashyap never worked with Jubilant FoodWorks as an employee or a consultant, Domino’s India spokesperson asserted. “Many statements in the viral video are false, misleading and damaging to the reputation of our brand,” the spokesperson added.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=4ffcb1fc-67c4-47d4-bff1-48223481cc13

As expected, very strong set of results by dominos. If you look at the market cap its close to 17000 cr which is pretty much the size of the entire Indian pizza segment ( as per NRAI its 6% of 3.5L cr food services market based on The Food service report 2016). However QSR chained restaurants are growing at 18%-20% - aided by the strong mall growth numbers

The growth in app downloads also augurs well as Online orders accounts for a major portion of the sales. In Q4 there were 9.6 mil app cumulative downloads and 0.6 million added during the 3 months. The % of Online to total delivery has also jumped significantly to 63% in Q418. It was 51% in Q4 17 and 68% of Online orders comes through mobile phones up from 58% in Q417. Clearly, the digital sales are driving the growth. There is also Bangladesh that is yet to be activated.

3 Likes

I visited my local Dunkin Donuts on Saturday. Surprisingly, they are localizing themselves to compete with smaller outlets. For example, Dunkin is now selling freshly brewed tea and dip-dip biscuits. It’s a big draw in a corporate environment. The price is about 40 bucks but a customer tends to spend more once acquired. More importantly, Dunkin is showing its ability to localize which is a big + for Jubilant.

4 Likes

Below could be one of the reasons that promoters need to desperately sell thier stake in Jubilant Foodworks:

Basic question. What is the contract terms (how long they can use dominos branding) between jubilant foods with dominos?

Jubilant FoodWorks reported strong numbers for Q1FY19 .

- Revenue for the quarter jumped by 26% yoy (on a favourable base) to Rs855.1cr,

- EBITDA grew strongly by 78.5% yoy to Rs142.1cr,

- Led by decline in employee, rent and other expenses as percent of net sales, the EBITDA margin expanded by 489bps yoy to 16.6%.

- Deprecation was down by 20.9% yoy and other income jumped to Rs7.1cr (against Rs3cr in Q1FY18).

- Thus, PAT for the quarter stood at Rs74.7cr against Rs23.8cr in Q1FY18.

<<Same store sales growth (SSSG) for the quarter stood at 25.9% yoy>>

1 Like

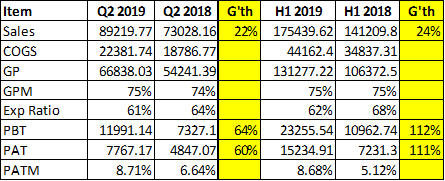

Good stack of numbers from Jubilant. Topline growth of 22%/24% and bottom line growth of 60%/111%.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/54d79172-2909-45e9-9ff8-bcdd7f8a5c43.pdf

2 Likes

Jubilant came out with good results. Sales were up 21% YoY, operating profit was up 44% and EPS was up 60% for the quarter. Yet, after the results the stock crashed on heavy volumes and is now down around 33% from its peak reached a couple of months ago. In the concall, the management admitted ‘competitive pressures’ in getting delivery personnel and a possible slowdown in growth in H2 due to high base effect. I have a tracking position in the stock for some time now, and since these points don’t seem serious enough, the question is whether it is time to load up.

I am not much of a ‘numbers’ guy and generally do not go beyond some basic back-of-the-envelope calculations. (Qualitative factors about Jubilant are well known and not mentioned in this post).

Based on some traditional parameters, the stock still seems expensive:

| Parameter | No. of times |

|---|---|

| P/E TTM | 49 |

| Market Cap to Sales TTM | 4.16 |

However, this is not the right way to value this company. Earnings can be volatile especially for low margin businesses, and Jubilant throws out far more cash than what its PAT indicates. Warren Buffet has said that growth in Book Value closely approximates growth in intrinsic value of a business in the long run. Using Net Worth as a proxy for Book Value, I get a CAGR of 26.65% for Jubilant:

| As of | Net Worth (Rs. Crores) |

|---|---|

| 31-Mar-10 | 157.74 |

| 31-Mar-18 | 1043.91 |

| CAGR | 26.65% |

In the last 8 years, Jubilant Book Value has grown at a CAGR of 26.65 % p.a. Using this for ‘G’ in PEG ratio, I still get a value far higher than 1, making the stock look expensive

Finally let us see DCF, which theoretically is the soundest method to value a business but requires making forecasts of cash flows and growth rates. Here, instead of forecasting far into the future, I try to see what future outlook the current market cap of Rs.14,000 crore has priced in.

I start with the current Free Cash Flow (FCF) of Rs.250 crore and use a discount rate of 13%. I calculate present value of future FCF in the format ‘Rs.250 crore growing at X % p.a. for Y years, and a terminal value at the end of Yth year’ . Terminal value is defined as present value of annual FCF from Yth year to perpetuity at zero % growth rate. For zero % growth rate, I use discount rate as 8% due to higher degree of certainty in achieving it.

Using the above and trying out various scenarios in excel, I get that the current share price of Rs.1,055 factors in the following:

| CAGR % | For Years |

|---|---|

| 15% | 27 |

| 20% | 15 |

| 25% | 11 |

*Plus Terminal Value thereafter

Can Jubilant deliver this – a 20% CAGR for 15 years or a 25% CAGR for the next 11 years? Looks on the higher side intuitively, but in the last 8 years, FCF has increased at 36% CAGR. And size of the opportunity is big, so there is still a long runway ahead.

If multiple valuation methods converge to a single value (rather a single range), one can have a higher degree of confidence in making the decision. I am not seeing that in all of this still. What do fellow boarders think? Comments are welcome.

8 Likes

I think the reason for jubilant price volatility is the its operating margins are near its peak. I guess when peak margins are combined with competitive pressures future expectations become muted.

However jubilant of the past can’t be compared with current as the pricing strategy was different and now after its move to edlv , it is better positioned to increase penetration and who knows where margins will settle if it continues to increase penetration further. Another tailwind acting in its favour are benign raw material prices. That said , since it’s business predominantly comes from delivery and aggregrators are also very aggressive it’s delivery costs have increased and that to me is a more important threat.

As far as penetration is concerned , I think as one moves to tier III towns like the one they have opened in ambaji this qtr, rentals costs become more manageable as rents are much lower in these places and if you are an early entrant you get a volume boost.

The future looks OK to me as of now with normal business challenges that all QSR chains face as they grow.

Best

Bheeshma

7 Likes

Few latest brokerage reports on Jubilant Foods:

Agree with you that these are normal business challenges which every business has to navigate. My post was more about understanding the valuation – what is the right price for Jubilant (and why).

Probably just a planted story for the papers

3 Likes

Gross margins for jubilant remain good and stable. However its the expense ratio that can go out of control. The improvement in the expense ratio that we have seen this qtr is probably a result of them closing down further dunkin donut stores. The main cost that needs to be checked is the rise in delivery costs which has ballooned in the wake of ecommerce offering lucrative remuneration to delivery boys. Several dominos outlets are short staffed for delivery talent. They have also terminated arrangements with third party delivery vendors to save some margins. I think they will have some pressure on that front which will impact cash flows. However, I think they will maintain their long term ROE of 21% but it will be difficult to exceed that in this sector which is a mix of two bad sectors - restaurants and online food delivery - both which we know have bad economics. At these levels even after the steep correction - perhaps it would be prudent to wait if looking at fresh investments.

On the plus side - its got a fabulous recall and a strong brand name , pizza eating culture is only intensifying and it remains the king of junk food, pizza is addictive due to it’s savory elements , dominos has the widest reach of any qsr chain in India and it has a strong balance sheet.

Best

Bheeshma

Disc - invested

7 Likes

I am just worried about the alternatives that people can now order through home delivery. Uber/swigy/zomato are expanding in tier 2 very aggressively. Though dominoes is also available on the app but 100’s of other options too which makes me believe that the best for Dominoe’s is gone. You wont believe its been 50% off on near about everything here in Indore on Uber eats, but not on dominoes. Every local place has its own pizza chain, though I like Dominoes the most but wide availability of choices may shift customers to other food items or restaurants.

Though these discounts will not be forever but people gets habitual to it and once they taste other food at a discounted price I think a part of people will shift to other items available to their doorstep.

Just my thoughts based on the business environment. I think margins are at peak and the SSG too.

2 Likes

For what its worth, Swiggy is attractive because of the large discounts it offers. Just like Amazon, it follows the dictum of ‘Build it and they will come’. This is possible due to the continuous gush of fresh funding. Their financials are nothing short of terrible:

So clearly, Swiggy will face huge headwinds while phasing out the ‘discount mode’. I think it’s already happening with Ola. Vehicle hiring prices are slowly climbing back and I can already see people hiring outside Auto/Car for some of their travels. Indian Startups have been playing the pricing game for a long time now. Only the D-Day will tell us how sustainable they are without the artificial support.

As far as Jubilant Foodworks is concerned, the brand is clearly an excellent strength. In my opinion, they only have to keep doing what they’re already. Any additional steps, such as discounts, to counter the likes of Swiggy is unnecessary.

Will they continue to face challenges because of discounts in food delivery Apps? Absolutely. Does this constitute a huge problem for them in the long term? No, in my opinion. The Apps become a threat when the companies behind them manage to get out of the pricing/funding game and establish themselves as ‘built to last’, rather than ‘built to sell’.