There is a simple explanation for reducing NIMs: cost of funds is rising since Dec’ 17 across the board. Leave alone NBFCs, even banks are feeling the heat.

The number of shares has decreased from 3,36,19,835 to 3,34,48,209 in April 2018. You can check the details here

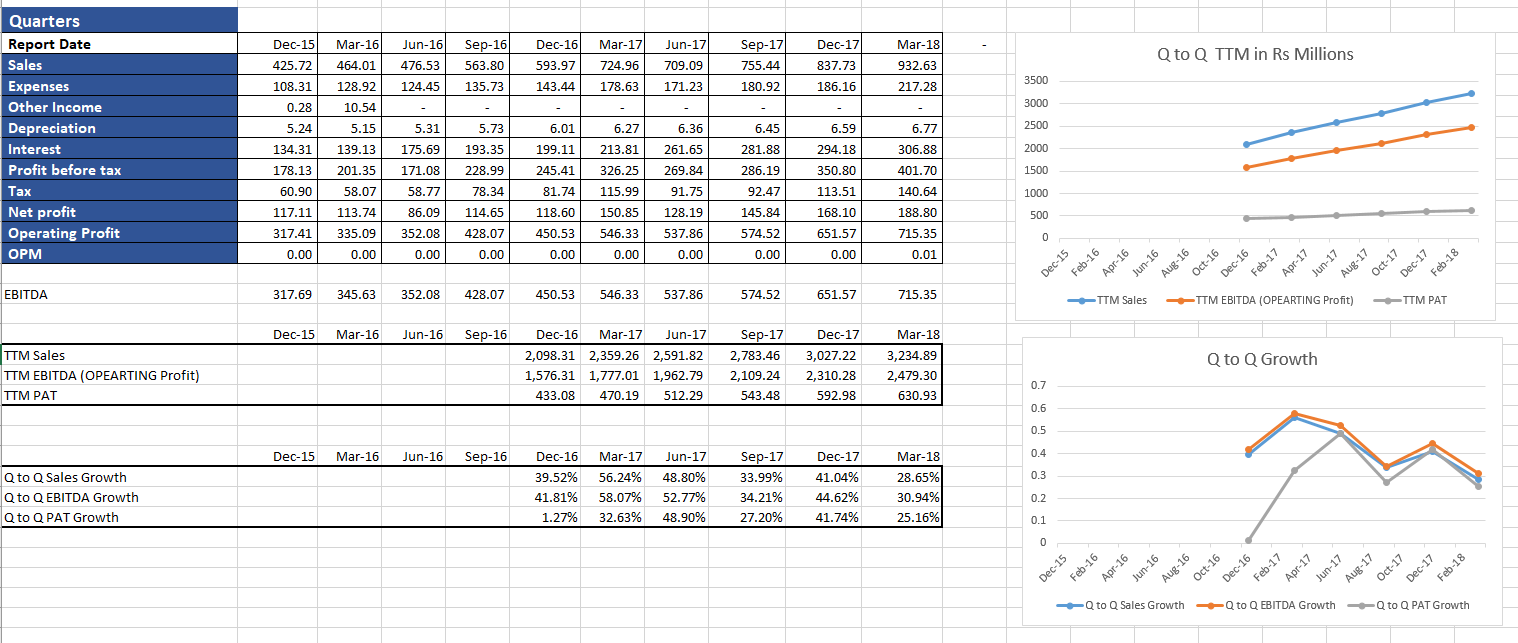

it is found interesteing while ploting the Quaterlly data from screener to see in big just click twice the image

disc: not invested

Asset Reconstruction Business.

As NPA stress has grown to new high, I think this should negatively impact ARC in operations since many years. ARCs who acquired assets say till 2016 or before will face more the expected depreciation of the recoverable value and decrease in resolution expectations.

2016-17, 17-18 has huge flow of new NPA assets. That will give much larger choice to final Buyers and effect resolutions. Prices of NPA assets i think have fallen significantly. Property prices are down over 30% in open market and NPA properties will get resolved only at 50% of the original value few yrs ago. Even if ARC acquire assets at 50% of the total outstanding, due to delays in resolution it will add significant additional interest burden.

Though new ARC will find it attractive to buy assets at even low price but older ones will see deterioration in their old assets and stop buying. This shall effect JM Financial also.

These are my thoughts but I want to get some data to validate them. Have any one of you done NPA and ARC related business analysis or know any data sources ? Also share your views.

Some highlights I made from FY18 concall.

-

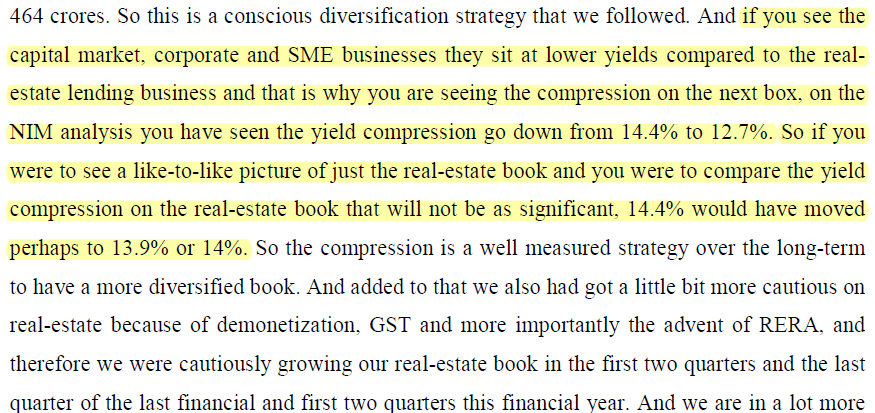

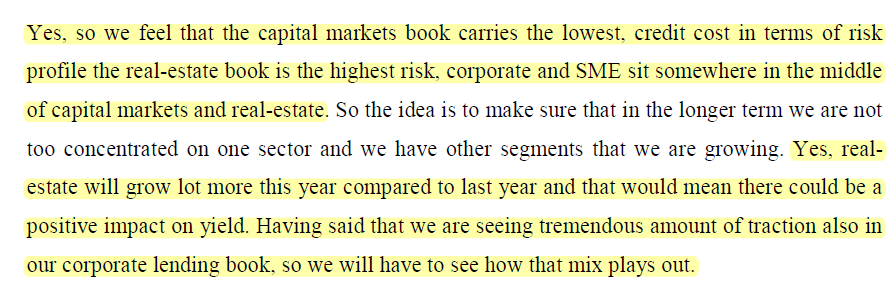

Contains some explanation of reducing NIMS…part of it was explained as product mix. Real estate lending which has highest NIMS had come down as a % of loan book.

-

Guided for much higher growth in real estate lending…all segments have potential of 30+35% growth

-

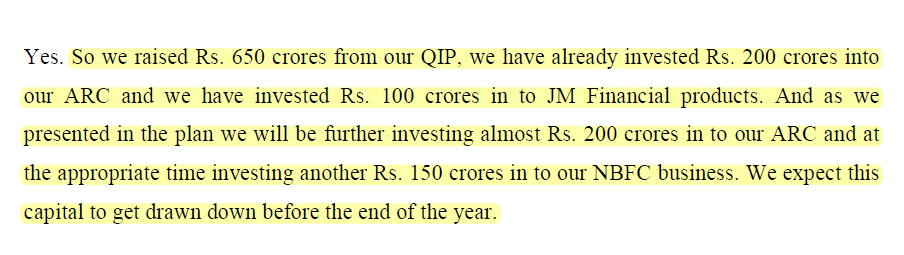

Management is very positive on ARC business. Deals moving more towards cash.

-

Asset management business may not grow fast. They are very profitable in their segment (more into institutions) and dont want to spend alot on building scale.

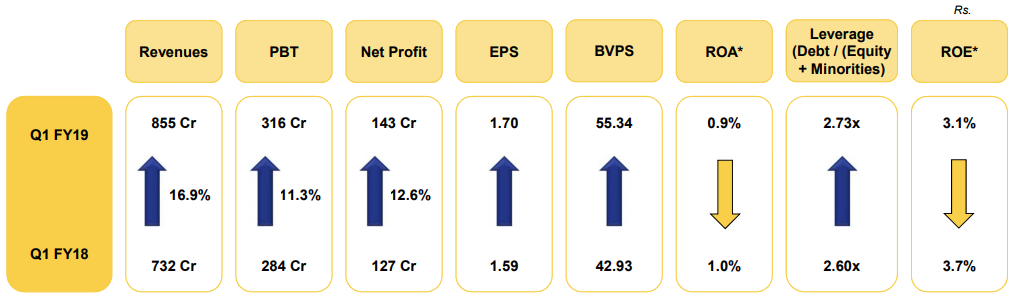

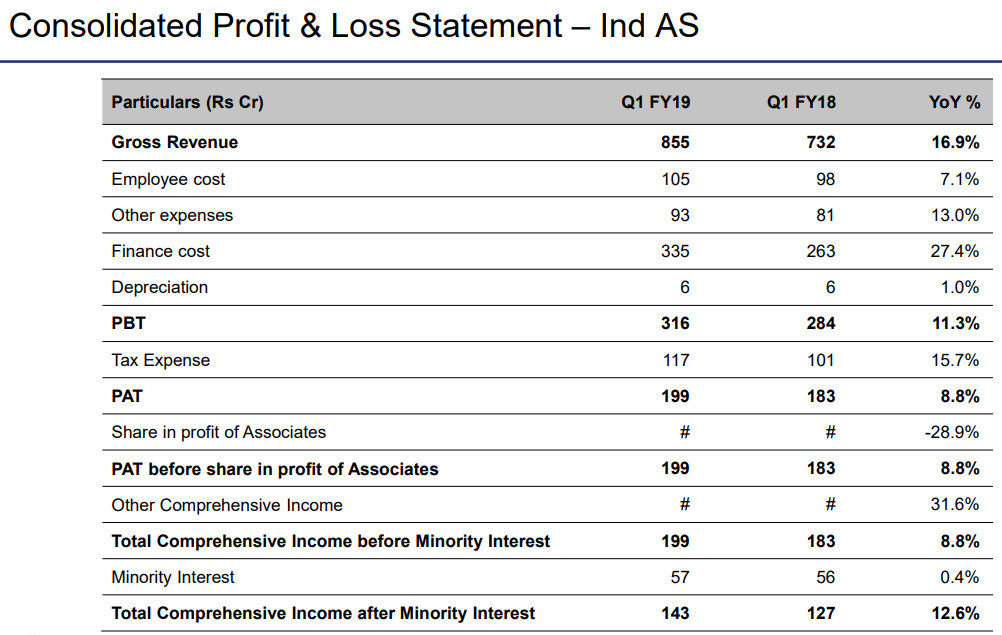

FY19Q1 results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/df14a5ea-16dd-4af2-b5fb-9f86c517275d.pdf

Haven’t gone through the results yet. But the stock has been taking a beating since late yesterday

TL growth of 17% and BL growth of 12%. Not great like other qtrs, but not bad either.

Even last year Q1 is a weaker compared of Q4 of the previous year.

Management in their AGM said this will be a challenging year for JM and in fact all other financial companies.

Management is not looking to grow their Housing loan book aggressively. They want to place all the systems and processes in place first. On the other hand we have Piramals who have entered HF sector and scaled up their loan book aggressively in less than a year.

Management when asked about declining NIMs said it is because of Asset Liability Mismatch. I have not checked their borrowings position but they were saying that it will take a year for them to rectify their short and long term borrowings.

So I guess this is not the growth year we were looking for.

Disc: Had a tracking position. Will look to re-enter at lower levels.

PAT grew slower than revenue as finance cost went up disproportionately (27%)

Gross loan book grew by 35% to 16442cr. Good to see that NIM has gone up QoQ from 5.6% to 6.1%. Yield was at 13.3% vs 12.7% in Q4.

Other observations

- IWS segment net revenues were up 10.6% (excl inter segmnet dividend last year), PAT was up 11.6%.

- Mortgage lending revenue were up 23% but PAT was down almost 5% as finance cost grew 50%. Mortgage lending loan book was at 8504cr vs 5678cr (up almost 50%).

- ARC acquired assets worth 657cr vs 339cr in Q1. JM contribution went up sharply to 526cr of 657cr vs 62 cr of 339cr. AUM stands at 13294cr now.

Why finance cost went up disproportionately? Market rate for money has not gone up by 27%, whats with JM?

Thanks

What I meant is that if the borrowing rates would have been exactly same as last yr, then finance cost would have also gone up about 16.9%, but it actually went up 27%. This additional amount can be because of higher borrowing cost or increased leverage.

I read the commentary on how growth will slowdown. Are there other threats for us to watch out in this scrip?

The funds will allow the non-banking financial company (NBFC) to reduce its leverage and grow the loan book. “The fund infusion comes at a crucial time when the sentiment around the NBFC space is not so positive. Our debt-to-equity ratio after fund infusion will stand at 2.1 from the existing 3.7,” Vishal Kampani, managing director of JM Financial group, said in a phone interview.

The target is to grow the loan book by 20-25% each year over the next three years, Kampani added. The shares were purchased via private placement, and the funds were raised at a pre-money equity valuation of ₹6,300 crore, valuing the lender at ₹7,175 crore.

Old Rating reports but worth looking

http://www.careratings.com/upload/CompanyFiles/PR/JM%20Financial%20Limited-10-08-2018.pdf

https://www.icra.in/Rationale/ShowRationaleReport/?Id=66953

Points for investing

- Margin is improving as expense is going down as a % of total sale

- Tax compliance is consistent

- consistent Dividend Payout

- Overall professional experience of the management is added advantage

- Group is mainly have three subsidiaries JM Financial Products Limited, JM Financial Credit Solutions Limited and JM Financial Capital Limited thus provide adequate asset quality and flexibility

last three year average Sales Growth is (3Yrs)34.07** % (screener )

Negative

Companies book having more than half exposure to loan to NBSC’s

recent panic in the market creating headwind on the sector but on the other hand provide more chances for accumulation

The dividend income from subsidiaries comprised around 70% of its overall revenues in fiscal 2017

disc : invested as the scrip is crying for purchase valuation this is not any recommendation please do the research before investing

Mouth watering valuations.

A few red flags:

- This margins improving happened with tailwinds, which are headwinds now

- Cyclical businesses: Wealth management, capital markets broking and investment banking

- Wholesale finance: Funding could be an issue here in current environment

So key thing here would be understand if these earnings can sustain and if they can continue to grow.

I understand they have a lot of direct exposure to builders in their real estate book - as in direct lending exposure. Since sales are not happening builders were using NBFCs to manage cash flow, with the entire liquidity crunch NBFCs are themselves not having liquidity so this is stopped (at least temporarily) so this may be a credit quality issue in a quarter or two. I would be careful on this stock.

FYI I have sold this end of last year so haven’t tracked results/ concalls since, info may be dated, but I doubt they have changed composition of book in a significant way in last 3 quarters. If they have apologies. Agree management is good and in all probability there is collateral though it is not liquid in nature.

Decent set of numbers by jm