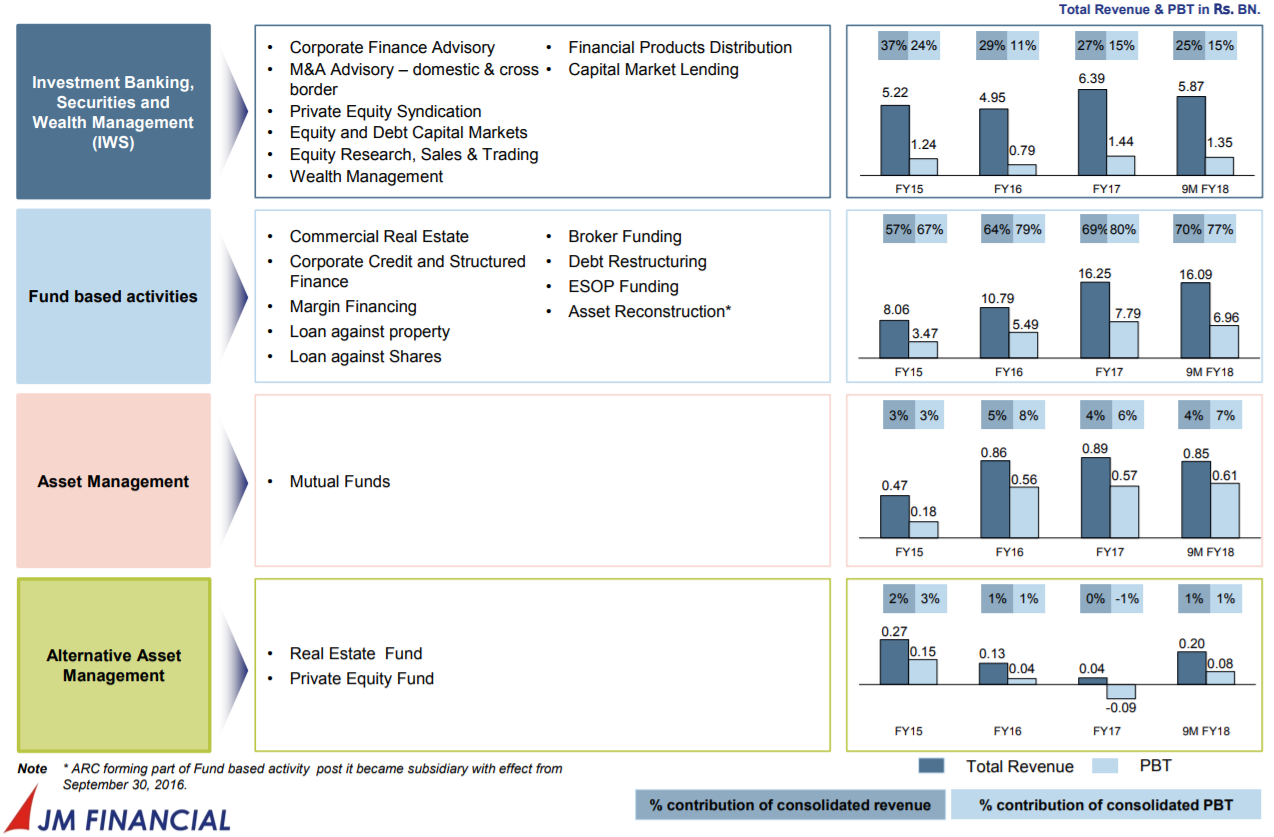

The AUM stood at Rs. 31,910 Cr (excluding custody assets) as on Dec 31, 2017 as compared to Rs. 27,289 Cr as of Sep 30, 2017 and Rs. 22,337 Cr as of Dec 31, 2016.

Fund based business

The lending book of JM Financial Products stood at Rs. 7,043 Cr as on Dec 31, 2017 as compared to Rs. 6,192 Cr as of Sep 30, 2017 and Rs. 4,123 Cr as of Dec 31, 2016…

The lending book of JM Financial Credit Solutions stood at Rs. 6,475 Cr as on Dec 31, 2017 as compared to Rs. 5,708 Cr as of Sep 30, 2017 and Rs. 4,822 Cr as of Dec 31, 2016…

Mutual Fund

The average AUM of our Mutual Fund schemes during the quarter ended Dec 31, 2017 stood at Rs. 16,633 Cr as compared to Rs. 13,952 Cr as of September 30, 2017

Securities business

During the quarter, the average daily trading volume stood at Rs. 5,688 Cr

Hi,

Recently I read a news about JM selling 32% stake in Sona BLW for a good profit. I would like to know, which companies are there in which JM Financials holds a stake? I tried to find this information in annual report and investor presentation, but couldn’t find any.

Link:

If we are to compare the financial performance of Consolidated Companies which have multiple verticals, which ratios/values does one need to take into account for the different verticals under the Consolidated parent business.

Any pointers would be quite helpful. I need to compare Edelweiss, JM financials and Aditya Birla Capital.

The 650cr QIP was done at 162 and the stock fell to 125 odd levels. It trades at a price to book of about 2.6, which I think is reasonable for a company that is growing more than 30% with great return ratios. Promoters have bought about 0.19% from open market between 5-9th March in recent fall.

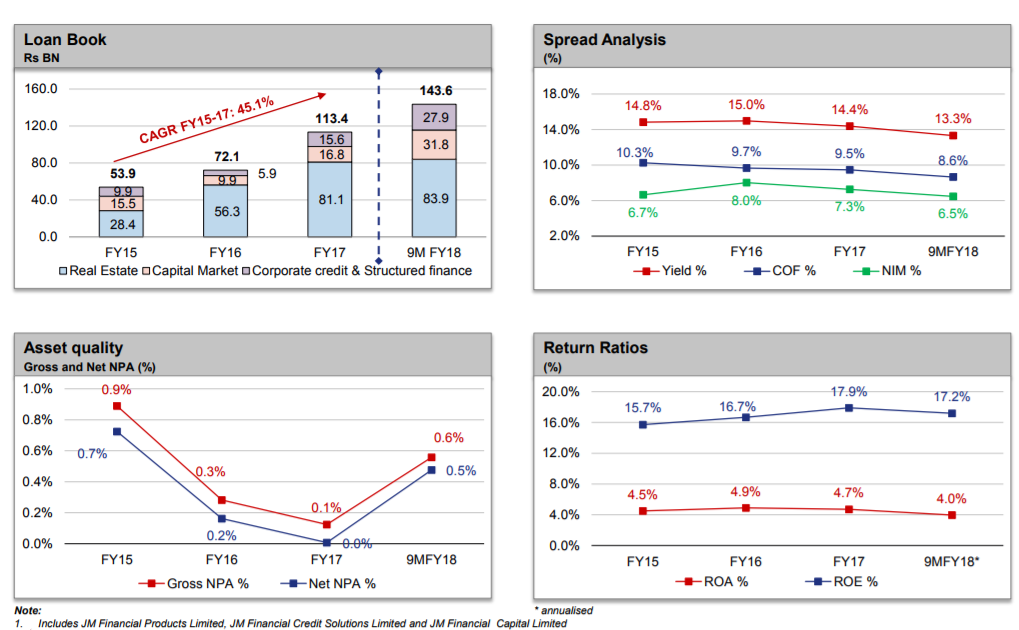

Below is a slide from the corporate presentation showing the strong track record.

8390cr is real estate lending…This will not grow more than 15-20%. There will be some pressure on the yields as the company is moving towards more conservative deals. They have been very conservative on the real estate lending front. JM just stopped lending for 2-3 months post demonetization and picked it up slowly later.

3180cr is capital market (margin finance, LAS). This will grow fast

2790 cr Corporate credit and structured finance (including LAS). They will gain market share from PSU banks.

JM’s focus area is HFC, followed by SME lending (LAP and working capital) and they plan to build a book of 2500-3000 cr in each of these over next 3 years. In next 3 years they plan to have 20-25000cr book.

Currently they are the least leveraged NBFC with debt to equity of about 2.5 odd, which has good scope to go up. They can go up to 6 when it comes to HFC and SME.There will be pressure on NIMs and ROA but that will be compensated by increased leverage to maintain RoE. Investments in SME and HFC are expected to improve RoEs in FY19 and FY20

In HFC, JM Financial will offer loans to home buyers across 6-7 affordable home projects that it has already selected. The focus areas will be the extended Mumbai suburbs including Kalyan, Thane, Vasai and Mira-Bhayander in tandem with Ahmedabad and Pune. The average ticket sizes may be within Rs.10-15 lakhs on an average (Link)

Here is a link from 2016 saying JM wants to be 40% real estate, 30% corporate and 30% SME by 2021. However, this was a while back and there would be some course correction.

Thanks rohit for the diagram with all the details.

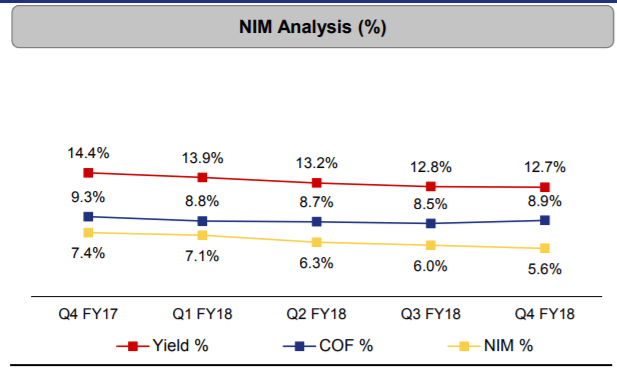

One thing that strikes out clearly from above charts is the consistent fall in NIMs from a high of 7.4% in q4 fy 17 to 5.6% in q4 fy 18. This seems to be a very significant factor and probably indicates some sort of loss of pricing power in terms of lending. The stock price also probably reflects the same thing.

There could be a ray of hope for improvement in NIMs with QIP money being deployed for lending purposes.

Overall the long term story seems quite interesting but the NIMs trajectory seems to be the key monitorable. Besides of course the asset quality.

Why NIM are trending down? I think, we should compare them with similar companies. Which companies are similar to JM Financials? Motilal Oswal. Can we compare this company with other NBFCs?

in financial cos, revenues growing more than pat is not a good sign and if it consistently shows same trend, then there could be reason to worry. reducing NIMs/yields is one reason for lower profit growth, which is clearly visible in JMF. another reason is credit losses. generally, non interest income (fees, trading, treasury etc) should compensate and ensure pat growth is higher than revenue growth.

So falling NIMs are obviously a concern. But a few things are unique about JMF in this regards

Most NBFCs and Banks provide real estate lending at 14-16%. JMF has decided to take a more conservative approach and have been looking to reduce average yields to 12-13%. This is part of their general risk management strategy.Real estate lending is approx 58% of their fund based business.

Their recent entry to the housing finance (specially affordable housing, where average yields are 12-13%) might improve the NIM going forward (but only slightly)

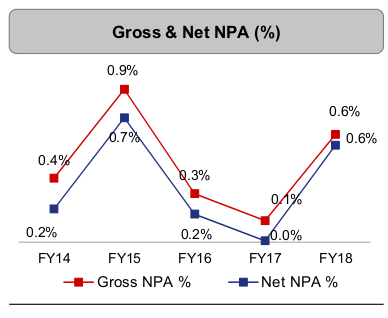

The conservative approach does explain their low NPAs

Agree with your comments. I think reducing NIMs is the major reason in this case. Management had talked about the margin compression being due to more conservative deals which happen at lower yields.

Fee based income has been subdued recently and is a cause of concern.

Rightly said.

Also at this price point, it is a great value. (PB: 2.62, OE: 18, ROA: 4.6, ROE: 20.4)

Pls check the comparison with Edelweiss, which is quite expensive (75% more expensive based on P/B). Data source: Value research online and date is of today’s.

also their debt equity is low at just 2.6x odd. they are well funded to grow fast if they want to. the fact that they are being careful about it shows management prudence.

discl. i own shares from slightly lower levels and am positive about their performance.

Asset Reconstruction Business (From JM Annual Report 2016-17)

Our asset reconstruction business is engaged in the business of acquiring and resolving distressed assets. During the year, we concluded 31 transactions with outstanding dues of 5,077 Crore acquired at a consideration of 2,252 Crore. Till March 31, 2017, we have, on a cumulative basis, acquired total outstanding dues of 28,710 Crore at a consideration of 13,279 Crore. During the year, Security Receipts worth 199 Crore were redeemed, the outstanding Security Receipts stood at ` 11,874 Crore as on March 31, 2017. The ARC business became a subsidiary of JM Financial Limited during the year. We are very selective in acquiring assets and do not acquire assets where we are unable to influence resolutions. The ARC business revenues are very lumpy in nature with high levels of profitability in the year of resolution of the assets.

The domestic banking sector continues to face substantial levels of stress in their loan portfolio partly reflecting legacy issues and deterioration of asset quality.

During the last year, several important amendments were made in the existing Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, and the Debt Recovery Tribunal (DRT) Act. The amendments are aimed at faster recovery and resolution of bad debts by Banks and Financial Institutions and making it easier for ARCs to function. The Bankruptcy Code replaces the entire gamut of extant corporate insolvency laws. It focuses on quicker decisionmaking, be it turnaround or liquidation and facilitating an early settlement of all stakeholder issues.

The ARC business of Edelweiss and JM Financial looks good after seeing the NPA crisis the banks are facing.

The Bank of America-JM combine has bought Rs 910 crore of SevenHills’ total debt of Rs 1,300 crore from the lenders led by Axis Bank. The company has a hospital each in Mumbai and Visakhapatnam.

Ten parties have shown interest in acquiring the equity of SevenHills. The bids for the equity portion of the company is expected to be opened shortly. SevenHills’ Mumbai hospital located in Andheri currently operates at only 20 per cent of its capacity. The initial plan of the company was to have 1,500 beds at the hospital.