Ludhiana plant, Horizon, Securipak etc relate to their diversification to Corrugation. These plants use Kraft paper and not white / writing paper. On their core office / writing / coated, speciality and packaging board, following are their plants;

Company is doing a 650 crore capex for a BCTMP pulp mill. The company has done some acquisitions in the corrugated box segment. A huge expansion in virgin fiber board was completed only in Jan 22. The company has just came out of major expansion for packaging board and Sirpur mills( 2019-22). On top of that they have been acquiring corrugated board manufacturers. They always had very high capacity utilisation for their paper business except for Sirpur. It is the realisation that makes the difference.

I think company is diversifying into related business that require smaller capex.

I read somewhere that a few MNCs are planning to establish large facilities in India. Among them are Sinar Mas Pulp & Paper, which plans to invest 10,000 crores, and Asia Pulp & Paper, which plans to build a 1.2 million-tonne factory. What’s the impact of this on existing players?

Asia pulp and paper seems to be a subsidiary of Sinar Mas. To set up an ecosystem that JK paper will definitely take some time. They have an excellent distribution and they have set up a good raw material procurement as well which will not be very easy for a new company to do. Such a large capex would take some time to be operational.

I am sorry if this is an oft repeated, and answered question, and I have missed those, why are the paper companies so cheap? Shouldn’t that make them attractive?

Looking at margins does not look like cyclical. Even in the worst period for the industry (Covid) they made profits. Also, they are continuously growing, either by acquiring or by expanding and setting new capacity.

Just to clarify, if you follow the TV Interviews, the pulp prices are not falling, however, the paper prices are falling owing to higher imports.

JKP is a solid old school stock with smooth balance sheet and backed by JK brand. KJP is also showing good ambition for a mature company. I like their recent foray into corrugated packaging. They are already the largest organized corrugator.

Current PE is actually below long term hist average of about 10. All integrated paper companies are just coming off a spectacular 2023. Wood pulp prices are at rock bottom, Indian wood prices are elevated, hurting realizations. Due to china and asean slowdown, paper of coated kind is getting dumped in India. Classic double whammy of a text- book bulk commodity producer! Near term is all clouds and rain.

IMHO my own long term thesis is that JKP will maintain 10 to 15% sales growth with about 15 to 20% margin. Near term high base may result in flat to degrow th near term.

DISCLOSURE - lay retail investor, not very bright… holding a small position around 390. Will accumulate slowly

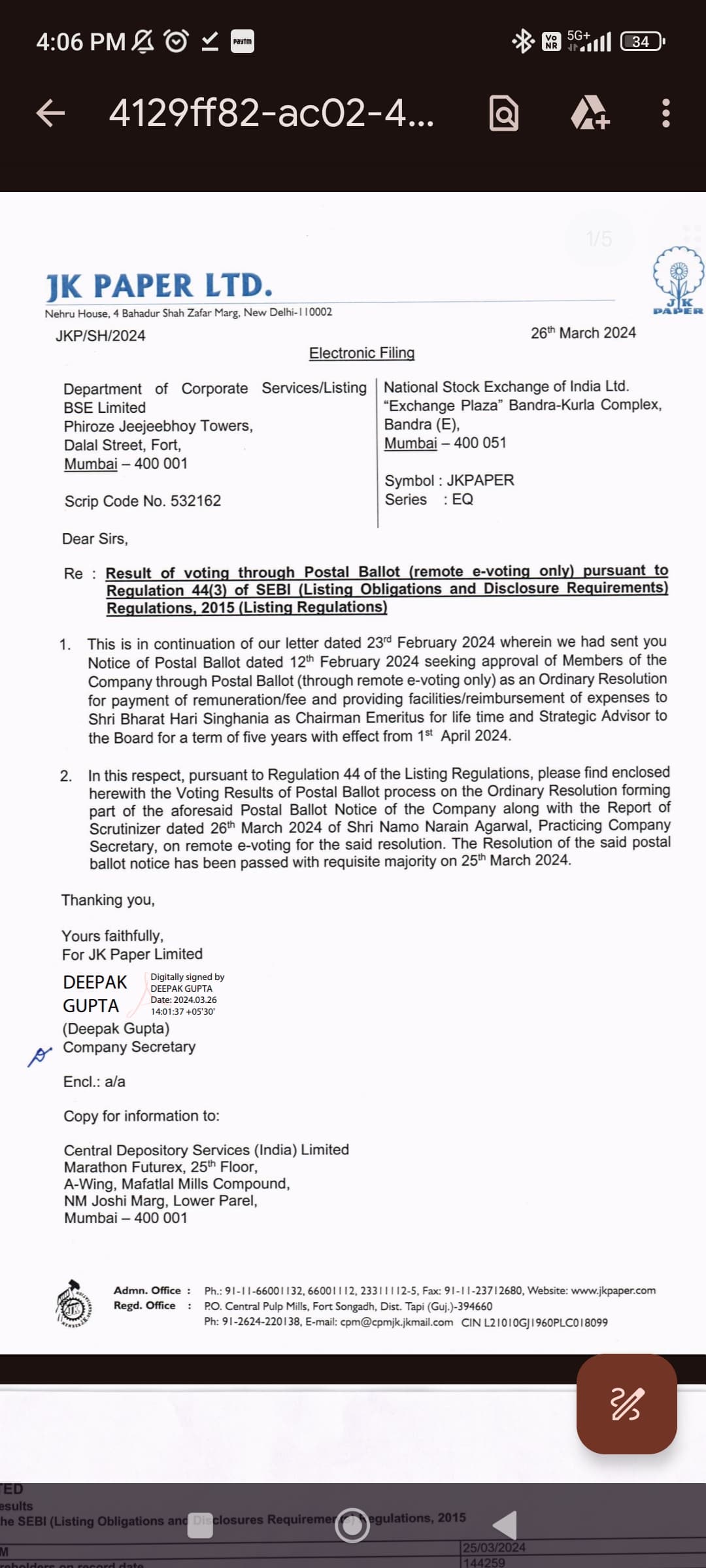

Yesterday, JK paper submitted this, I am in doubt regarding the outcome of this for a long duration investment, he(Bharat Hari singhania) received 281.20 lacs approx in FY ended march23 out of which 275 lacs was commission and rest was sitting fees. So if he will receive X amount for lifetime without actively working for the company, isn’t it a bad proposition for the company ?

In FY23 he was the key managerial personnel so the amount is justified. When he resigned he did mention that he will still remain available for JK paper for consultation and the above letter simply states that there will be an official position with the title “Strategic advisor to the board” and it will be fair to get compensation for it.

All in all, it will depend on the amount they are offering him.

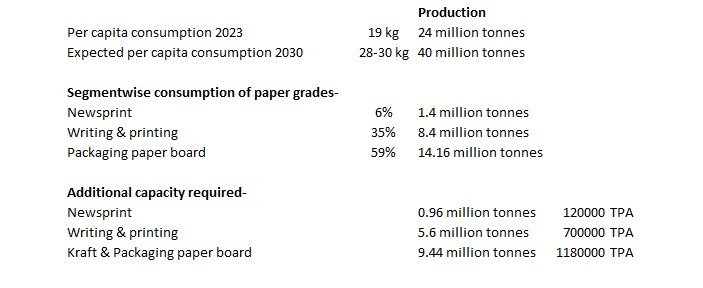

Industry is expected to grow at ~6% so a back of the envelope calculation suggests that industry needs to add 2 million tons every year to catch up with the expected demand.

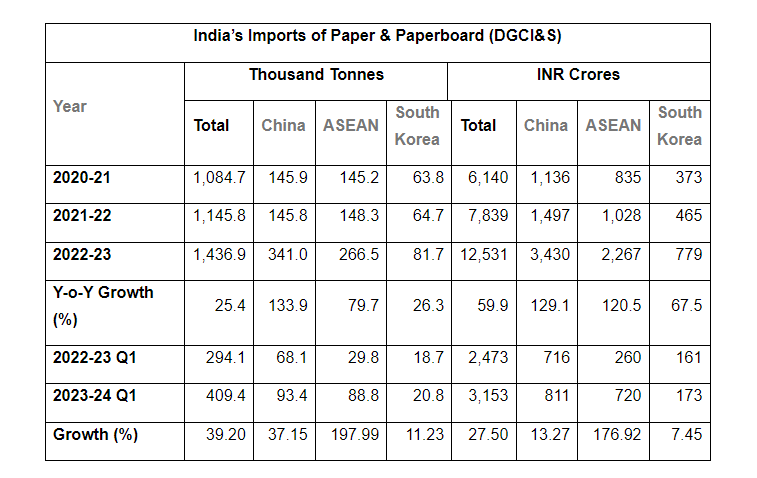

So the demand supply gap exists but its being addressed through imports which are on the rise since the removal of ADD. Indian imports of paper & paperboard have jumped 47% in FY23, the highest jump being in imports of uncoated writing & printing paper at 102%, followed by coated paper & paperboard at 51%. In the previous year, overall jump in paper & paperboard was ~25%.

In November 2021, the Directorate General of Trade Remedies (DGTR), recommended the continuation of then existing anti-dumping duty on imports of uncoated copier paper for a further period of 2 years. But the Ministry of Finance decided not to impose the anti-dumping duty and there is a logical reason for that. Paper is the most recycled commodity. When we import 1 ton of finished paper, it provides 5-7 times fibre for recycling, which in turn saves the foreign exchange on imports of waste paper. However, in the case of exports, every ton of export of finished paper, indirectly exports 5-7 tons of fibre also. The country has to thus make a higher foreign exchange payout for importing 5-7 tons of waste paper in lieu of every ton of exports of finished paper.

There has been a rising trend in imports and a declining trend in exports, thanks to the slowdown in China and massive paper capacity additions by Brazil, Uruguay & GCC. We don’t know when the demand for export will revive.

Other than that, one of the largest paper-making giants, Asia Pulp and Paper (APP), is going to set up the largest capacity in India (1.2 million TPA).

So to conclude, although Indian exports have outstripped imports in last few years, going forward, it appears that exports are contracting due to excess global supply while imports are increasing due to higher demand in domestic market (provided govt doesn’t intervene). JK Paper undoubtedly remains the best bet in the entire sector but there has to be a trigger (say ADD on imports). What’s the trigger here? In my view, any moderate increase in demand due to NEP or single use plastic ban will be met by increase in imports if not interrupted.

Views are welcome, especially opposing views. I am sure I am missing a lot of things here. Happy to be educated.

The company has stopped concalls this FY (qtrly PPTs and concalls were a regular feature till FY23). I heard the last (Q4FY23) concall I could not pickup any stated / implicit intention of the mgmt in this regard. This is pretty extreme / drastic action - does anyone have an inkling about it?