Royalty amount was 10 Cr per year and amount which they’ve paid is 8 cr. Can’t understand this.

1 Like

From annual report:

Royalty paid was 11.2Cr for FY19 and same during Fy18. On the face of it paying 8Cr for acquiring entire trade mark looks good but couldn’t find any details about unique pharma brands licensed by JB chem . Today con-call may through some light.

Q3FY20 presentation presentation Q3.pdf (952.9 KB) (good to see their domestic formualation growth of 14% in spite of ranitidine issue.

2 Likes

Notes from JB CHEM Q3 CON-CALL:

Consolidate revenue growth of 12.7% EBITDA growth of 15%…EBITDA margin at 21%.

Domestic business: 45% of revenue,remaining is from exports.

Domestic formulation growth of 14%…branded generic export grew 17%.

Chronic segment growing at 20%, growth from acute therapy segment is low.

Net cash: 580 Cr

Top brands:

Cilacar 200 cr

Rantac : 200 cr

Metrozyl : 150 cr

Ranitidine issue: impacted growth for the quarter and sales to remain flat for the year

growth affected due to negative news related to NDMA which spreads easily through social media and competition from players marketing proton pump inhibitors.

Actually the probability of cancer due to impurity is very low.

Creating awareness and bringing back growth will take time.

Last 1-2 months have seen some improvement.

Metrozyl: 4 SKU… With one SKU price increase has happened.other SKUs will be by March.

Domestic Business:

4 divisions: taking care of different brands which increases focus on brand and relationship with doctor.

MR no:1600.

Enough room for the each division to grow.

Confident of growing domestic formulation business faster than market.

We will keep adding new products to the existing divisions. Some of the new products added are ARB( telmisartan) , beta blocker( Bisoprolol),product in wound and pain management… Etc.

New products in last 2 yrs: contribute to 10% of revenue.

In next 2-3 yrs domestic business will contribute 50% of revenue.

Margins to remian flat( conservative guidence) due to certain expansions. Improvement may happen due Metrozyl price increase and royalty amount settlement.

Dependence on china for API: overall material imported is around 120 cr…75% of it is from china.

present strategy is to increase inventory. Currently we have not seen any impact due to China.

Exports: guided for growth of 10 to 12% in branded generic exports.

USA: 40 cr is revenue from USA… No of ANDA approvals:16.

Pending approvals:3. Plan to file 2 ANDA per yr.

We are cautious on US market due to pricing issue.

US FDA Issue with API supplier for one major product is solved… We will restart supply inQ4.

Have approval for ranitidine but holding due to NDMA issue. Domestic API supplier has to adress FDA issue.

Russia /CIS : market not growing at faster rate due to sanctions…we have limited products( 7 to 10) approvals. 5 new products approvals expected this yr.

South Africa: cagr of 15% to continue. Tender business and pvt market doing well.

Contract manufacturing business: certain issue with our client in Russia and that should change in next year. Adding new clients which will improve growth.

No major capex… Regular maintenance capex of 40 cr.

9 Likes

Thanks @spartan for the concall notes.

I think for FY 21, few margin levers I can think of are

Higher contribution of domestic business which has a lot of operating leverage built in for the company.

Hike in price of Metrogyl group of products which is in DPCO.

No further royalty payment to Unique pharma which should add directly to bottomline.

Key monitorable remains to see how company fares in the newly launched molecules especially in the domestic space. Company needs to land up with another one or two blockbuster molecule/group of drugs like it did in Cilacar to keep the growth engine chugging.

3 Likes

Where can we get the Data for the month of January?

Disclosure

Invested in J B chemicals

I have been tracking jb chem for some time now but never prepared any concrete notes where I can come and get grasp of company within few minutes(except few posts on vp forum I m guilty of not preparing structured notes for most of the stocks I follow). Inspired by @Donald bhai I went through some of existing stock stories on forum. Even though they have written some years back anybody can get grasp about the company business and key points by going through them. I have committed to write such stock storey for JB CHEM and keep it updated regularly. Will be looking for guidance by @hitesh2710 bhai, @rupeshtatiya and any other vp member can contribute for the same.

7 Likes

They are implying that many ranitidine formulations might get impure with temperature.

Seems worrisome this time.

3 Likes

Despite USFDA Ban, JB Chemicals & Pharma Continues To Market Ranitidine In India

What will be the impact of this on Revenue is the question to ponder upon in the US Market? @spartan @hitesh2710 any views here?

2 Likes

JB chem continue to market Rantac in India.

As per US FDA press release if the Ranitidine is stored above room temperature over time NDMA impurity level increases.

There is possibility of Indian drug regulator extropolating the US FDA data for Indian market( may not happen also as I have not seen any knee jerk reactions from Indian drug regulators) . If it happens then JB chem will have tough time as Rantac is their major domestic revenue contributor( 200 Cr) . To some extent already the Ranitidine market size has been replaced by proton pump inhibitors. Other issue is they had ANDA approval for Ranitidine and wanted to launch it in US market which is unlikely to happen now.

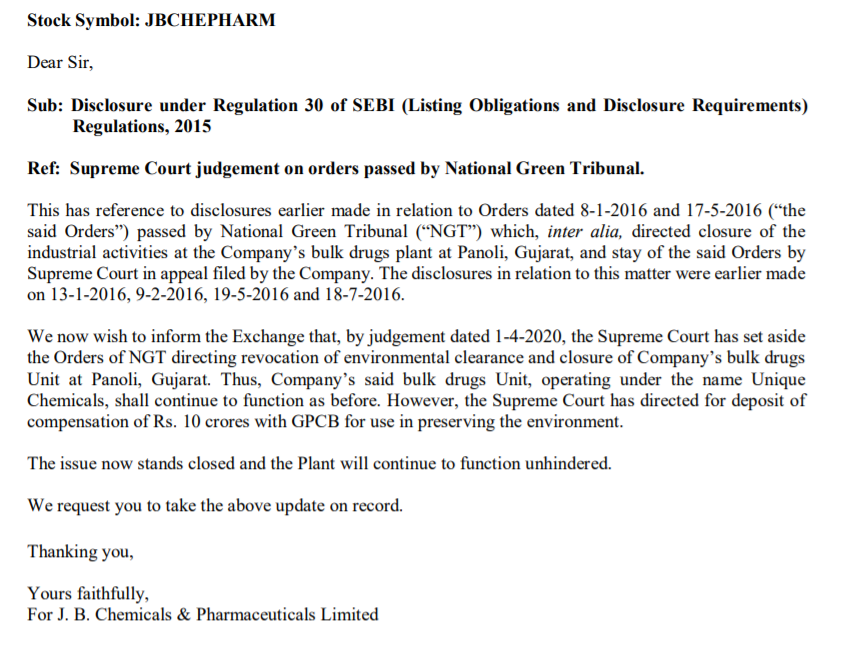

JB chem notifications to exchanges:daf9a656-ea23-423d-93b6-bcc8252772d3.pdf (88.9 KB)

Discl: holding 3% of present PF… Have done transactions in last 30 days.

3 Likes

JB has received approval for ANDA for Carbamazepine Extended Release Tablets USP 100 mg, 200 mg and 400 mg. (for treatment of Epilepsy and Trigeminal Neuralgia). The product is a generic version of Tegretol XR tablet in the same strength of Novartis Pharmaceuticals Corp. According to IQVIA, US sales were approximately USD 128 million.

3 Likes

saw this 2012 annual statement. the rent has increased by 20% and now in 2019 the rent has reached to 261 Lakhs around 12% CAGR. Is this normal or should we consider as poor management attitude towards minority share holders.

This is a related party transaction as well.

1 Like

On the con call they say that Unique Pharma is selling the brand so no royalty payment. if that is a sale then it will be higher transfer of money ?

Also Buy back has mostly promoter shares ? can they actually decide whose shares to buy back.

Disc - Invested

2 Likes

There was a news regarding the promoters selling out. Is thr any other update on the same given by the company?

JB chem Q4 and FY20 results.

Investor presentation:

Revenue growth of + 6% to 443 cr in Q4

Ebitda margins further improved to 20.6%(91cr) from 15.6%(65cr) in Q4fy20

PBT 67 cr vs 68 cr.

EPS Rs 6.3 in Q4 and Rs. 34 for FY20.

Bottom line is impacted by 10 cr of exceptional payment due to court order.

Domestic formulation growth has been good(in spite of Rantac impact!)

Company experienced a slow down in acute segment sales due to covid-19 impact.

Good cash flows.

Next year bottom line should be better (considering one time exceptional payment,royalty payment adding to bottom line)

No mention of stake sale by promoters.

1 Like

KKR to buy controlling stake in JB Chemicals & Pharma in $500 million deal

54% stake at Rs 745 per share

1 Like

KKR has done share purchase agreement with promoters to acquire 54% of stake in company.

Open offer to public shareholders to acquire upto 26% of stake at Rs.745/share.

If I have understood correctly, depending on the subscription for open offer by public shareholders, KKR and promoters are in agreement so that KKR shareholding will not be more than 64.90% of company.

Generally entry of PE firm brings in more professionalism, better growth, efficiency.

Only during last 2 years JB chem strengthening field force and had decent growth in domestic market.

KKR may accelerate it by introducing new products in India or entering new geographies.

@hitesh2710 bhai , as retail investors how do we approach such scenario. Does market perception about JB chem change and give better market cap? ( its PE has already expanded in last one year).

I think the entry of KKR is a good event for retail investors and future story of jb chem. Because of high proportion of domestic revenues, there could be some sales pressure especially in q1 fy 21, but post that things should normalise.

The stock price in the short term has run up in anticipation of stake sale. So I guess once the stake sale goes through, the stock price might remain sideways for some time post which it will trace the results trajectory.

5 Likes