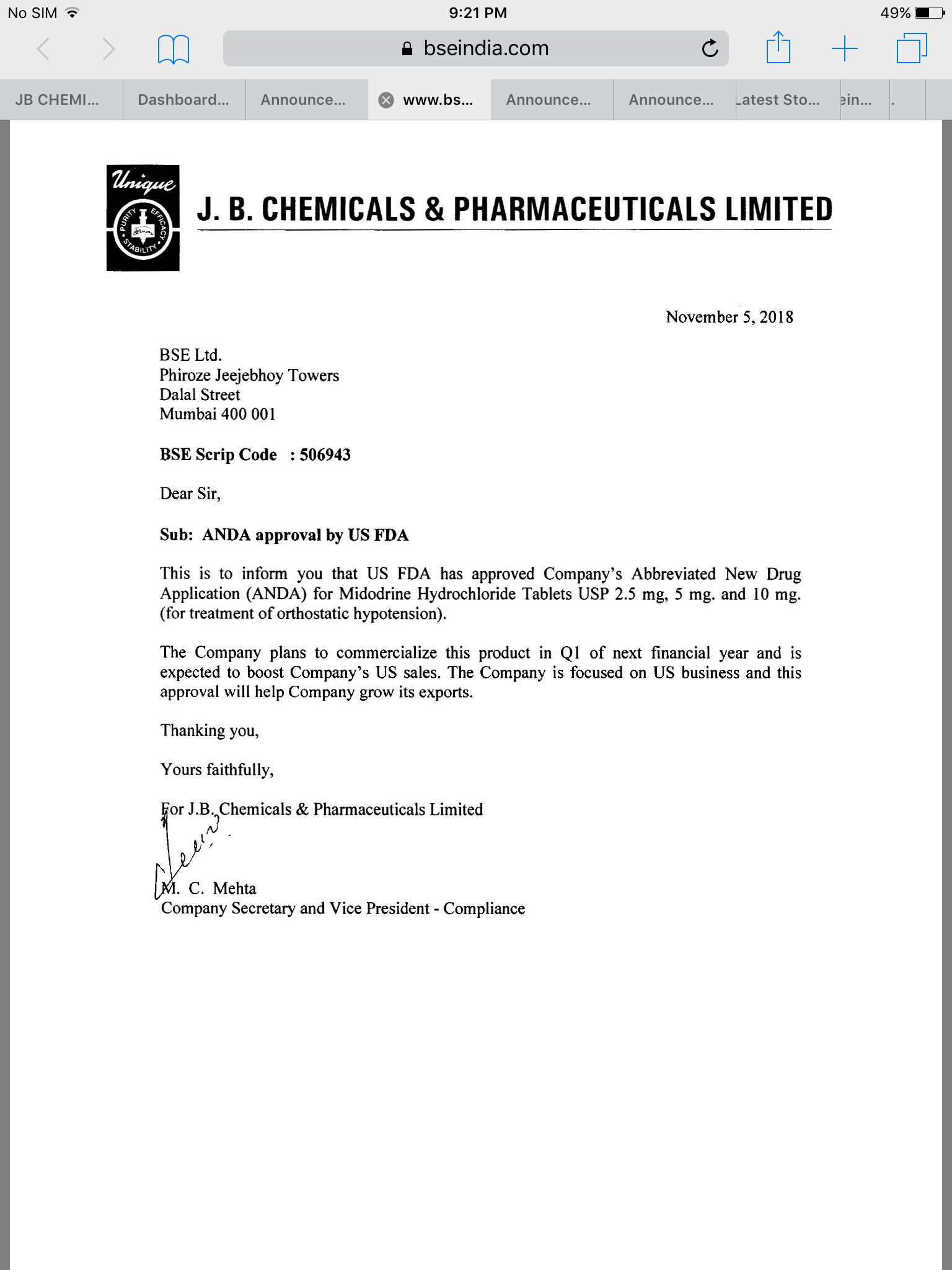

ANDA approval by US FDA

Company’s reply on the above news:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/463700B9_5E11_4FC8_94D2_95ACA86D578A_171839.pdf

Notes from JB AGM to shareholders queries. I may have missed/misinterpreted few points. Request others to add /correct:

Overall business having decent trajectory. looks to maintain 15% growth and same margins of last FY.

Domestic market:

Present medical representatives no is 2065( including 450 managers). Added 100 in beginning of year…no more additions until year end. …looking to consolidate as we added more than 1000 MRs in last 2 yrs. MR efficiency and bandwidth getting better. Attrition rate of MRs at 15%.

Four divisions focused on domestic formulations. No more divisions we are going to add. Engagement with doctors and focus on brands and extension of brands. Initially we use to lose focus on our old brands when we introduce new drugs which we have corrected by adding MRs and divisions. Our strategy is working well.

Main brands(4): Rantac, Cilacar , Metrozyl and Nicardia shown good growth and brand extension possible. We are doing a lot of innovations/combinations with existing brands. Easy and more effective in getting 5% growth on existing brands than making 100% growth on new launches. Our 4 major brands have good opportunities which we were missing and corrected in last two years.

Existing four brands still have a lot of value even though they are common drugs with many competitors. We are looking at expanding the uses of same.

Introduced new variant of Rantac which can be taken once a day. Looking to get more volumes of Rantac, as other class of drugs(PPIs) which are prescribed as acid reducing agents have some side effects but this shift is going to take time. Even small % gets converted to Rantac it will be huge for JB . (cost of Rantac Rs.23 per strip…JB sells 45 lac strips(30 tabs) per month.)

Cilacar : target to increase the use with other combination of other anti-hypertensive’s . Just to compare ,market size of amlodipine(another antihypertensive) combination is more than amlodipine alone. Trying to do the same with cilacar combination. Looking for more subdivision for cilacar among cardiac and renal care.

Margins with Rantac and Metrozyl is very less( Metrozyl 100 ml at Rs.13 of govt price cheaper than water). Cilacar and Nicardia still have decent value and margins.

We don’t do business with govt. Participation with govt tenders are very less.

New products focus on cardiac and renal segments. Introduced 6 new brands last year. 2 to 5Cr revenue per brand during first year of launch…it will take few years to make meaningful contribution from new brands. Each year we will introducing new brands as we have enough bandwidth of MRs now.

Backward integration: Cilacar and nicardia backward integrated. Rantac and metrozyl api we buy from outside. Don’t issue much issue with raw materials.

Generics, price control and Govt policy : 13% of our products under DPCO presently. Govt may announce policy on generics in 2020. It’s going to affect pharma industry for sure. Govt takes avg selling price, costs to decide on retail selling price and they may regulate retail pharmacist margin also . Overall the impact will be less on JB as most of our products are not highly priced. There will be an option for price revision yearly based on inflation, cost. JB is not getting into generics presently.

EXPORTS: 35-40 countries …largest exports to USA, Australia, Russia & South Africa.

USA: competitive market. Introduced last year approvals with partner. 5 ANDA approvals are pending and 1or 2 ANDA filing this year. JB doesn’t have own front end team. Last year growth was exceptional aided by Glipizide sales. We are looking to manage same revenue from US for present FY.

South Africa: JB was supplying to one customer in SA and partner was looking for partner and our subsidiary started in 2007. SA is a difficult market to enter due to regulations and scale up business. We have basket of around 60-70 products. We have good product pipeline for SA with good potential. SA we have private:public business in the ratio(60:40) few years back it was mainly through govt tenders(60%) with less margins. Slowly we are changing to pvt market business.

Russia/CIS: Last year growth mainly contributed by CIS countries. This year we may not have similar growth. 2new products for Russia during the present year. ?4 pending approvals.

CRAMS: stable margin business with fixed cost. Contributes to 10% of business. We are building business with some marquee customers. Scaling up of CRAMS business depend on customers and takes time to through validation. This year our customer JJ is having some issues at Russia.

API business(Diclofenac salt): Once new registration process is over our revenue will go back to earlier no of 120 cr. It will not happen during the present year.

Q1 export formulation was low: due to low US sales and sales to JJ was flat.

Capex: routine maintenance capex of 40Cr for fy20.

Capacity : Tablet facility at Panoli plant has high capacity…lozenges plant we expanded capacity looking for contract manufacturing.

R&D expenses : 2-3% of sales.

Buyback: Not possible till Nov 2019. Dividend policy: around 30%.

Fire accident : value last 7.6 Cr…insurance claim under process…?6 Crs have been received…plant is operational.

Stake sale: No( there was a lot of rumours about JB getting acquired by Lupin/Piramal which does not seems to true…management denied it and told that they have already notified to exchanges when news came out)

Acquisition : when there is a good opportunity and matches with our business plan but everyone ask valuation in the multiples of revenue not based on profit.

AGM was chaired by Pranab Mody in the absence of JB Mody. Pranav ,Jay Mehta and Nirav Mody interacted with investors on the sidelines of AGM. I think they are very decent in conducting AGM, interacting with shareholders and discussing about company operations without any over ambitious targets.

Disclosure: invested around 5% of PF.

19 Likes

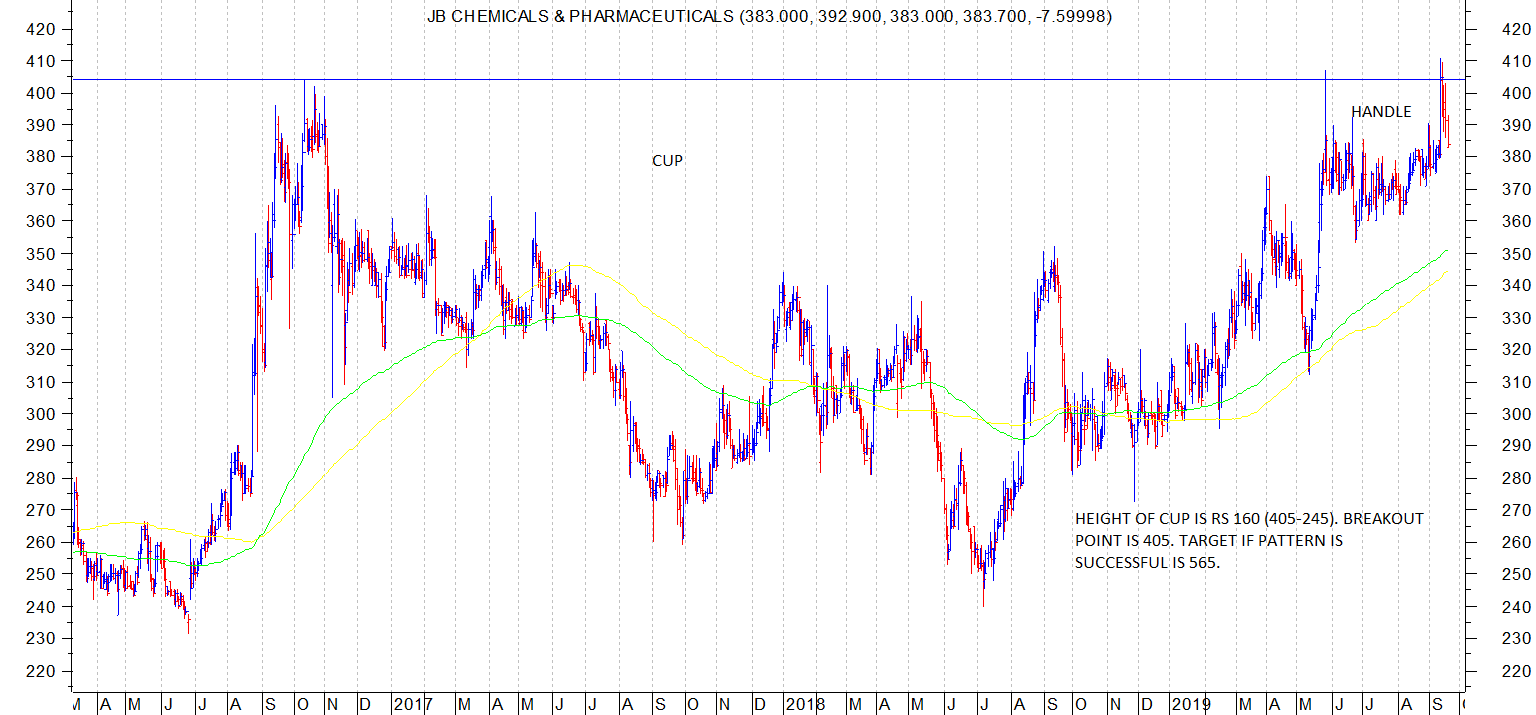

J B Chemicals has formed an interesting chart pattern resembling a cup and handle pattern. Till now, it has been showing good relative strength as compared to overall general market which is weak.

Attached chart with comments.

disc: invested around current levels.

7 Likes

First of all I am invested in jb chem, so take my views with a pinch of salt.

The issue is of potential carcinogenic impurity in ranitidine which is NDMA. Now different manufacturers of the finished dosage form of ranitidine source their API ( raw material) from different sources.

It is as of now not clear which API manufacturers produce ranitidine without this impurity. According to some sources, jb chem gets it from sms pharma. I would await announcement by jb chem. Some cos have voluntarily withdrawn batches (not totally, only some batches) while the authorities have ordered a probe.

Coming to jb, it contributes 159 crores as per fy 19 AR. Which is 10% of revenues. Profitability of the product might be much lower as the product is under dpco and costs around 80 paise per unit.

On the flip side, jb chem pays 35% tax and will benefit out of govt cut in corporate tax.

Technically, 200 dema is at 351 which needs to be watched for support.

6 Likes

Ranitidine:

As per report of a US ab which tested ranitidine samples across companies, all products had NDMA impurity which was far above acceptable level. It is understood from experts that the issue is with the molecule itself rather manufacturing process of a particular company. This is the reason that global companies have gone for a voluntary withdrawl even though FDA has not asked for a recall, as the companies know the reality.

JB Chem has annualized sales of 190 Cr from Ranitidine (from company presentation).

Ranitidine is their top product in domestic market.

Companies affected by Ranitidine accident: JB Chem, Strides, Solara & SMS Pharma in listed space

I read an update on ranitidine problems from nomura.

Some salient points

NDMA is considered a PROBABLE carcinogen.

USFDA has issued notice to all suppliers to check the quantum of NDMA. As the current evaluation process is underway a lot of companies including Sandoz, Dr Reddys, have announced withdrawal of sales from US market.

Glaxo has announced withdrawal of Zinetac from Indian market.

It may take about a month to determine the quantum of impurity in the molecule. If the level if found to be high, then suspension of sales is likely to be applicable to all players. However if levels are found to be acceptable then resumption of sales is likely and if Glaxo then relaunches its product it is likely to regain its market share.

As of last week (before the news came out) Cadila had 36% market share, Glaxo had 30% and JB Chem had 24% share in domestic market.

In US markets, market share of various companies is Strides 33%, Glenmark 31%, Amneal 27%, Dr Reddys 5%.

IF ranitidine goes off India market, players with omeprazole, pantoprazole and rabeprazole are likely to benefit.

Leading players in domestic mkt

Pantoprazole – Alkem, Sun

Esomeprazole, Torrent, Sun

Rabeprazole - Dr Reddys, Lupin.

Domestic companies have the option to continue sales till the report of levels of impurity comes through and inquiring with chemists, I find that JB Chem product remains available.

12 Likes

It is worth noting that there is an issue with the molecule of Ranitidine itself rather than Ranitidine from a particular company. Ranitidine as a chemical entity produces NDMA due to unstable nature of compound. (see attached file)

So, all companies are bound to be affected.

The lab in US which shared this hypothesis substantiated the above point by testing Ranitidine samples from 10 companies and all tested positive for NDMA in very very high concentration vs permissible limits. This precisely proves the point that its not an issue of a particular company but that of a molecule. So any company which is saying that our product is fine, needs to prove it with data.

GSK, Sandoz, Dr. Reddy’s have recalled their products because they know the truth and given the body of evidence, it was prudent to recall it immediately.

Solara - one of the largest API manufacturers of Ranitidine has decided to halt production all together.

Global Updates:

South Korea & UAE have banned Ranitidine for import & sale

All major manufactures in US have decided to stop sales

Given the scientific evidence against Ranitidine molecule for presence of NDMA, a doctor would question that I why should treat patients with Ranitidine. There are multiple other salts available in market to treat heart burn/acidity which have been tested for NDMA and no traces were found.

JB Chem

JB Chem doesn’t make its own Ranitidine API and sources it from Saraca & SMS.

Saraca is the same company whose API certification has been cancelled by European authorities and it was supplying to GSK (product recalled).

As a responsible company, it would be better to show data if the product is free of NDMA else halt the sale of product in interest of public health (given the evidence against Ranitidine molecule).

Valisure-Ranitidine-FDA-Citizen-Petition-v4.12.pdf (840.4 KB)

5 Likes

Here is the clarification from JB Chem related to ranitidine impurity.

jb chem rantac announcement.pdf (241.5 KB)

3 Likes

I think its clear after the clarification. As JB caters to Indian market , if other suppliers call back their products , it will benefit JB as they continue to sell ranitidine.

2 Likes

BUY BACK 3.68% Of total paid up equity @ 440/- per share through tender offer route spending 130/- Cr…not sure promoters participating or not…8.38% acceptance ratio if promoter do not participate…https://www.bseindia.com/xml-data/corpfiling/AttachLive/9975b466-9016-4a53-b4ba-2d7889c3b7af.pdf

JB Chem results.

Aided by margin improvement and as expected, tax benefits, q2 profits have shown big growth. jb chem q2 fy 20.pdf (981.7 KB)

H1 FY 20 EPS 19 plus.

7 Likes

JB Q2FY20 results has been good with gross margin expansion and PBT growth of 36%.

Domestic formulation business of JB grew by 15% in Q2FY20 (204 cr vs 177 cr in q2fy19).

I was more interested in domestic formulation business due to Ranitidine issue. Rantac is strong brand of Ranitidine by JB chem which contributed around 10% of the company’s overall revenue ( 189 cr as per company presentation)

Total size of Ranitidine formulation in india is around 700Cr.

Major players:

Cadila pharma 245 cr

GSK 209 cr

JB 153 cr

Strides 126 cr

(aiocd data)

I think the impact of reduced Ranitidine sales will start reflecting from Q3. Even though the US FDA statement on NDMA in Ranitidine samples came during 2nd week of September, news gathered steam only towards the end of September and first week of October. As more companies recalled Ranitidine and more articles came on media/whatsapp, people started questioning professionals prescribing Ranitidine resulting in prescription of alternative anta-acids. Significant sale of Ranitidine use to happen as OTC product influenced by chemists which is also affected. As per my interaction with few pharmacist /chemists the sale of Ranitidine is down by ?40-50% (much more damage in cities). Even though US FDA has come out with clarity on NDMA in Ranitidine(unfortunately which don’t get much publicity) the sales/prescription of Ranitidine has not improved. Even though overall market size is reduced JB may gain market share as GSK has withdrawn its Ranitidine brand.

Disclosure: reduced my holding of JB Chem

5 Likes

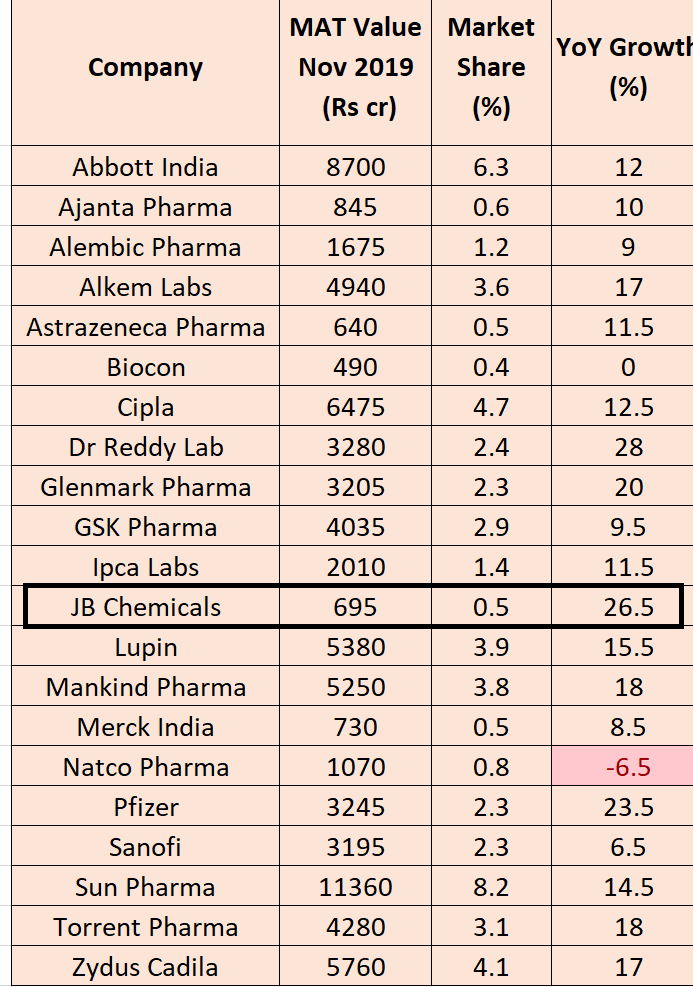

JB chem saw strong growth of 26.5% for the month of November along with some other pharma companies (Dr Reddy,Pfizer,Glenmark…etc)

Source: Toshniwal equity@ToshniwalEquity

NPPA has revised the prices of certain essential drugs up by 50% in which Metronidazole also included.

Metrozyl(metronidazole) is one among the top four brands of JB contributing to total domestic formulation sales of 623 Cr for FY 19( source company presentation). Exact contribution of Metrozyl to the revenue is not known.

JB chem has issued a notification about implementing price increase from next manufacturing batch and impact will be 5% of domestic formulation sales for entire FY.

BSE dt. 16.12.2019.pdf (267.2 KB) .

Discl: Recently increased allocation of JB

5 Likes

Thanks @spartan for the updates on JB Chem.

With the company taking a hit due to ranitidine imbroglio, these november numbers are very encouraging. My guess is the cardiac division is performing very well.

The govt allowing the company to raise prices of drugs falling under NPPA (read metronidazole group) also is good news for the company.

Currently there is a buyback going on by the company at Rs 440 per share.

Something unusual happened in JB Chem when it went past the record date for buyback. Usually the share price after the record date tends to fall but in case of JB, the price fell a day before buyback record date and post that there has been a very resilient price action. Currently trading at around 425, it shows trading in a very narrow range of around 5 Rs range.

The stock price is quoting very close to its all time high and has been able to maintain above its previous resistance zone of 400-410. The action post completion of buyback on 30 dec 2019 would be interesting to watch.

7 Likes

Really interesting remark Hitesh bhai on the price movement around the end record date. I thought about it and bought some more. The explanation that seems to fit is that operators were buying in anticipation of spike due to buyback and they then rushed to sell off just before the date was reached. Serious investors on the other hand stayed clear till this game was on and only afterwards came back into play, really strongly. Really adds to the conviction about this stock! Thanks!

JB chem management meet with analysts/institutions post q3 fy 20 results.

Seems a welcome move for investors to better know about the developments at the company, provided details are shared with everyone be it on company website or researchbyte etc.jb chem earnings call jan feb 2020.pdf (19.8 KB)

4 Likes

JB Chemicals came out with a steady set of numbers.

On consolidated basis, topline increased from 373 crores in q3 fy 19 to 420 crores in q3 fy 20, a growth of 14%. EBIDTA grew 15% while aided by tax benefits, net profit grew by 33%. 9M eps at 27.66 per share.

In another interesting development company has announced that it has bought some logos from Unique pharma to which it used to pay restricted royalty for a one time consideration of 8 crore. So from FY 21, this royalty payment that was made till now will no longer have to be made and will be EPS accretive.

4 Likes