Hi,

JAI deals with leaf springs segment and is a market leader in the parabolic leaf spring segment.

So are its product going to be impacted when Internal combustion Vehicles are replaced with Electric vehicles?

Thanks,

Deb

Hi,

JAI deals with leaf springs segment and is a market leader in the parabolic leaf spring segment.

So are its product going to be impacted when Internal combustion Vehicles are replaced with Electric vehicles?

Thanks,

Deb

Leaf springs are rarely used in passenger 4 wheels hence won’t make any difference. They cannot be replaced on goods carrier till technology changes

Great move, in my opinion. But I’m surprised even CVs are facing a slowdown equal to that of PVs. I was wondering perhaps BS6 implementation will be tough of CV component makers. But to see that even this Auto slowdown has impacted a market leader this much is interesting to hear.

In my eyes, the company has some issues with management remuneration. But as I have expressed elsewhere, I’m okay with a high-salaried management as long as the underlying business is economically good. The stock is somewhat undervalued in my eyes. Let’s see what kind of discount this news brings.

No Sir, Can not be.

In any case either it is ICE or EV or HFCell technology, you are going to need parts like Wheel Assembly (Tyre & Wheel Rim), Suspension etc.

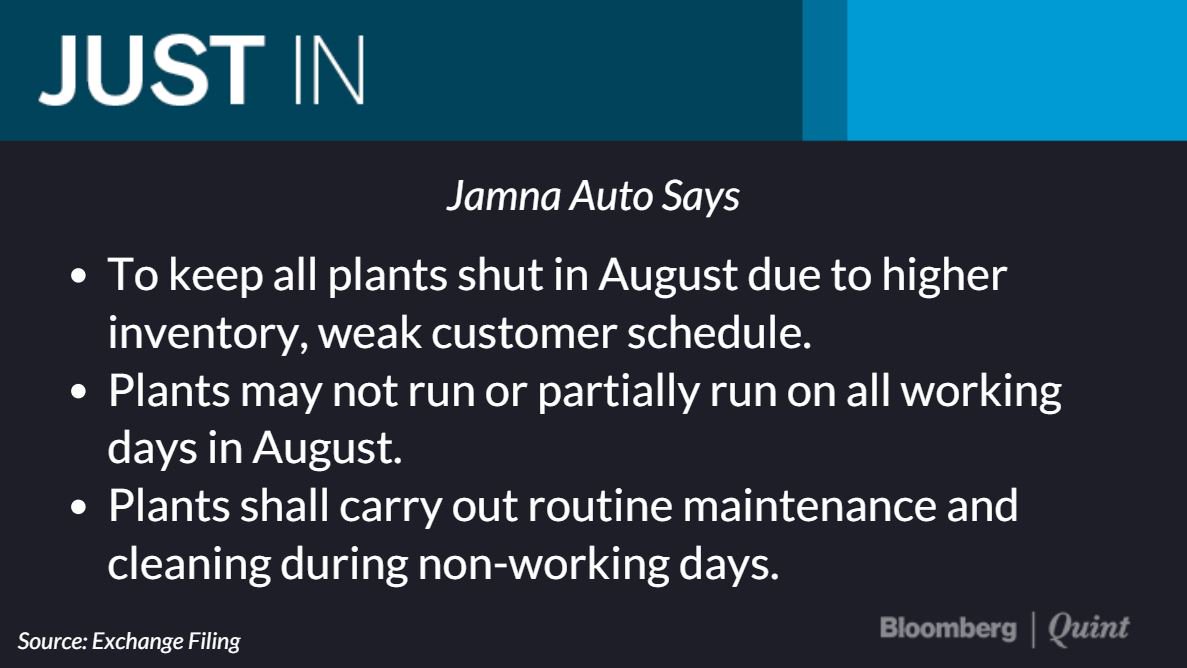

Clarification from Jamna :

“Some media news have interpreted that the Company has planned plants shut down for whole

month ofAugust, 2019. We would like to clarify that plants will run in accordance with production

schedule in August, 2019. However, due to cut in production, on some working days plants may

not require to be run or may run partially”

https://www.investing-notes.com/jamna-auto-industries-ltd-nse-jamnaauto-bse-520051/

An analyst’s write up on Jamna.

In line with the famous quote that goes ‘History doesn’t repeat itself but it often rhymes’ (apparently by Mark Twain) and given the cyclical nature of industry JAI operates in, I looked at previous years and tried to arrive at some sort of conclusion on what could be the right price (if at all). Please pardon me for my naivety.

From screener.in March-2013 EPS saw de-growth of 0.65 times March-2012 EPS (which was peak) and it was trading at PE multiples of around 11. Year after that i.e. in March-2014 EPS was even lesser than 2013, however price was hovering around the same level as that of previous year (meaning expansion in PE).

If we consider March-2019 EPS as the peak of this cycle then this year EPS could be somewhere around 2.27 (0.65 times 3.45 EPS of March-19) and assuming the PE multiple of 11 gives price of Rs. 25.

Discl. I have a insignificant position at higher price but looking forward to average down.

yes but the OEM Business coming online the cyclicality of the earnings will not be as intense as previous cycles and the margins in the OEM are also much higher

Find this to be a unique approach to see how much was contraction from peak earning (2012) and extrapolate the same with current EPS to arrive at projected EPS and further to a fair Price range.

Let me try to put another perspective. IMHO, this type of industry has a double squeeze situation - on one hand the inputs (steel) has high commodity type cyclicity, on the other hand the end user industry (automobile and MHV) itself also goes through its own peak and valleys (on a slightly longer time scale though).

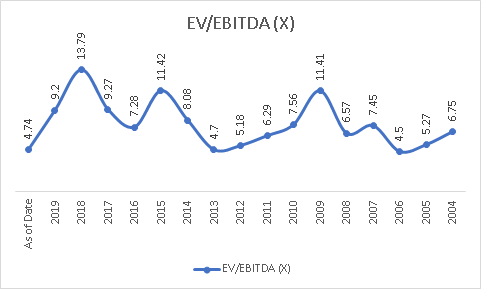

Instead of going into derived numbers (call it…compounded assumptions) why not to use a more direct and appropriate approach for this situation. Below is a 15 years EV/EBIDTA chart for Jamna. What is evident is that current EV is possibly lowest over 15 years horizon (covering couple of cycles).

Please note, time axis is in reverse order - starting from 2019 going into past.

Disc: No Investment while going to press. This may change ![]()

Thanks,

Tarun

@T11 I was looking at the same data from screener a while back, however you are missing that 4.74 would increase as and when next quarter results come. If you look from 2009, the fall was gradual which may imply that the correction in EBIDTA due to demand contraction got built in while calculating EV/EBIDTA.

Regards

Kanv

Hi @kanvgarg123,

Not sure if I am understanding it correctly.

To be clear on my intent all I am saying is:

a) Based on Friday closer the EV multiples are ~4.75.

b) This is almost lowest point if I look at broad 15 year horizon (off course this is on the date of book closure, this is how data is at my disposal).

In that sense, are you saying that EV will improve next quarter or EBIDTA will deteriorate further to optically improve the multiples.

As long as one part of the equation (EV) is tied to market forces… I dont know

Sorry but I am not getting the message.

So in March 14, the company had an EBIDTA of 44 cr which was the trough of profits that the company earned. The earnings cycle reversed from the next quarter. EV/EBITDA of 4.7 means equity value of 208 cr (If we add the debt component, market value of equity would go down further). In the current cycle, we only had one quarter of bad earnings factored in (Q1FY20). Now if we factor in the EBIDTA of say H1FY20 (46cr + 46cr) and assume that the company would be able to earn similar EBIDTA as H2FY19 in H2FY20, the total EBIDTA would come out to be (46 +46 + 64 +69) 225 cr. The current market cap of the company is 1445 cr which means EV/EBIDTA would be 6.4. Hence it looks optically that we have touched historically low EV/EBIDTA but that is not the case.

In previous years, fall in EBIDTA was gradual and hence the numbers had true reflection of business valuations whereas this time, the fall is drastic and hence the numbers are misleading.

Thanks @kanvgarg123 for the explanation - this makes absolute sense. Agree that the deteriorating EBIDTA will have impact further on the multiples in the coming month.

Thanks again.

Tarun

Which is why I wanted to buy it around 20 odd levels but it never went there. Maybe the difference this time is that company’s B/S is lean and strong.

Please correct me if I am wrong. JAI is primarily focussed on manufacturing of Leaf Spring suspensions. From what I have read, this kind of supension is used in heavy vehicles. How much of an impact does it have in the auto slowdown? Does CV and PV sales go hand in hand?

Co. has done a cumulative CAPEX of ~400cr and yet there is no increase in gross block during this period. If we take from 2008(consolidated) figures then Co. has incurred CAPEX if 719cr while Gross Block has only increased from 178cr(FY08) to 491cr(FY19) an increase of ~300cr. Does this mean that JAI’s Fixed Assets have short working life and need to be constantly replaced?

No, it doesn’t mean that. Tax laws allows depreciation in a certain way for certain assets. It makes all sense for the company to show maximum depreciation to save tax. In nutshell, the company maybe having all the assets but their current value on B/S is 0.

Gross Block as on 31-March-2017 is Rs.601 crore as per financial statements for the year ended 2016-17. The same is shown at around Rs.321 crore in the statements for the year 2017-18. This is on account of change in the method of accounting during the year 2017-18, which has been explained in the Annual Report for that year (Ind. AS 101 Exemption “carrying value of Property, plant and equipment has been carried forwarded at the amount as determined under the previous GAAP”).

Basically, accumulated depreciation upto that point has been reduced from the Gross Block and the resultant value is the new Gross Block starting from the year 1st April 2017. This is explained in the Fixed Assets schedule and Notes to Accounts for the year 2017-18.

In the Co.'s Annual Report, There is only mention of JAI Suspension LLP which caters to the aftermarket. Examining the RPT of the standalone entity, if we subtract the the standalone entity’s sales to the LLP we can arrive at the Revenue the standalone entity generates from external customers. To get Total Sales of the LLP we can subtract the standalone entity’s external sales revenue from the consolidated sales the JAI group. Is there any other subsidiary through which Sales happen? The subsidiary financials of Jai Suspension Ltd. (as on the Co.'s website) reveal that the subsidiary is not revenue generating. The Co. has not disclosed the financial of the LLP in the AR. Can someone please explain why?