The company has accounted for a Government Grant (refund of VAT from Jharkhand Government) of Rs.19.02 crore of which Rs.2.42 crore is taken as Other Income and the balance is taken to the Balance Sheet as Deferred, to be taken as income in future years (See Note no.45 on page 138 of AR FY 2016-17). Against this, I can see an Asset of Rs.13.82 crore created as “Government Grant Receivable”. What happens to the balance Rs.5.19 crore – can someone explain the accounting to me?

Time to relook maybe

Hi fellow investors/experts,

I have been reading about Jamna auto. The numbers looked good and it looked to be a great business. However after reading the AR’s from 2009, I have some serious doubts which tell me to stay away from it. However I want to make sure that I am understanding it right, before making a decision.

- 2013 AR – Auditor observations:

a. Delay in payment of statutory deposits, repayments of loans – 92Cr delayed upto 35 days. ICRA downgraded debt rating for the same. Reason stated by the company is temporary liquidity problems.

Reported Trade payables for year 2013 was 218Cr, which almost covers the Inventory+Receivables part. Capex for the year was only around 30Cr. PAT for the year was around 28Cr. If you look at the CF, net CFO after interest paid is 60Cr and capex is 30Cr. From the reported figures, I do not understand why the company could have liquidity problems, so big that it led to downgrading. This happened in 2012 as well – 46Cr of loan payment delayed

b. Reported fraud by job worker, company claims it is dealt with.

c. Around 35Cr of short term debt is used for long term investments. - Same year, that is in 2013, when there were observations, the auditor was changed because of their unwillingness to continue. Please note that the auditor was changed in 2009, due to the then auditor’s unwillingness to continue. All auditors changed in 2011 again due to their unwillingness to continue. The internal auditors changed in 2015. Isnt this unusual?

- 2014 AR – this year was a low point in recent past – OPM declined to the lowest – 5%. The reason stated was increase in raw material cost, due to inventory revaluation and inventory rationalization due to obsolete inventory. No more details given. Isnt normally the other way around – due to raw material cost hike, inventory must be charged down or impaired?

Strangely, the same year the auditors observed that there were discrepancies in physical verification of the inventory. Co claimed that they initiated verification of unfit inventory and disposed of such materials. No further details given. I feel this is fishy and weird. - 2014 AR – Auditors observed that the remuneration to the whole time directors are in excess to the permissible amount. Co then requested special permission and if not approved, the excess money will be refunded. Moreover, the managerial remuneration in general is on the very high side – many years it is around 15% of PAT and has even gone to 20%.

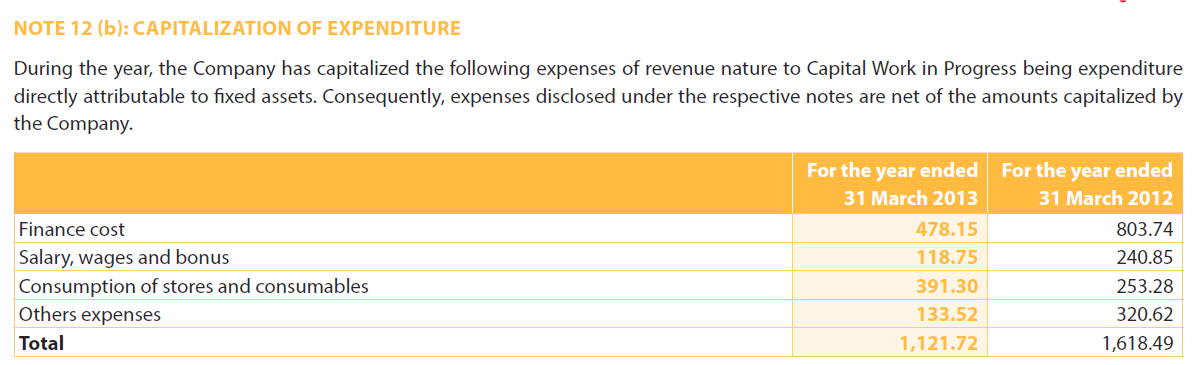

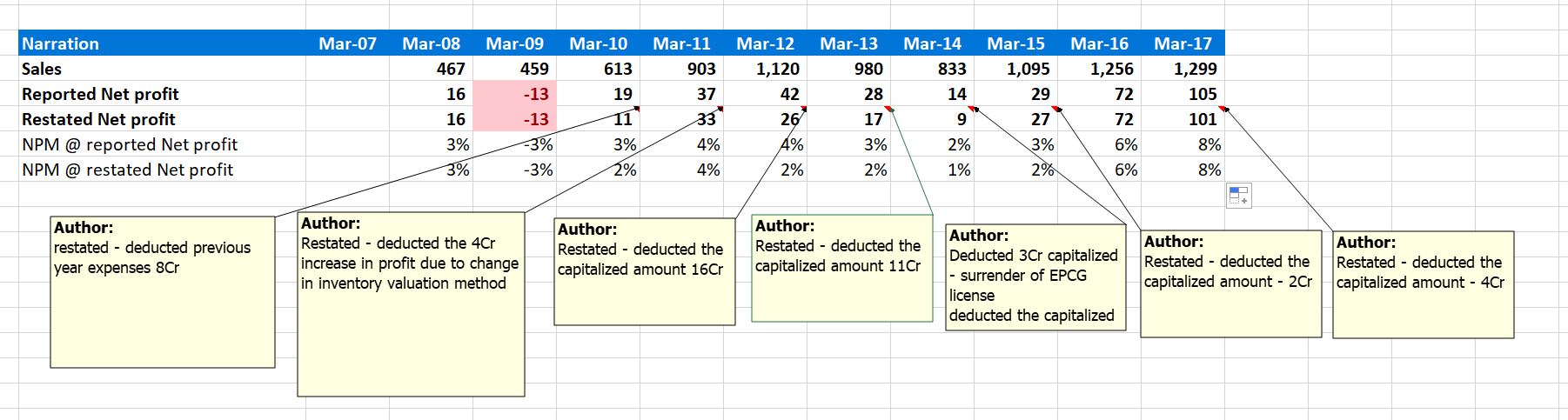

- In many years, company disclosed that some expenses of revenue in nature, is capitalized (snapshot attached). Why is such a capitalization if it is of revenue in nature? Shouldn’t it appear in P&L? R&D expenditures are usually capitalized, however during these years the company’s R&D expenditure was negligible.

- Strange capitalization continues – 2014 AR disclose that expenses due to surrender of EPCG licenses are capitalized. Isnt this wrong?

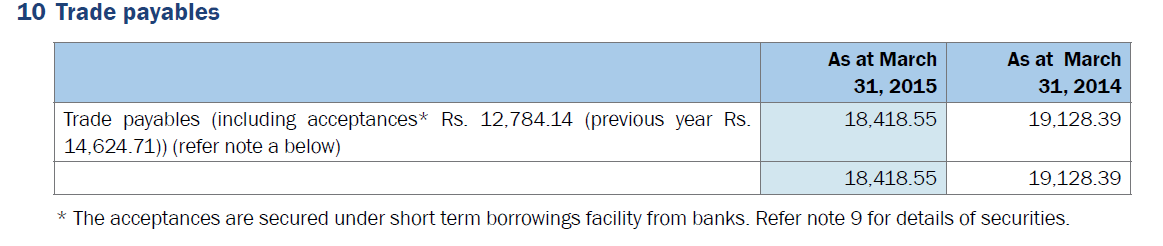

- 2015 AR - The reported trade payables is 184Cr, disclosure says this includes acceptances of 146Cr which is secured under short term borrowings. Doesn’t it mean that the 146Cr is a short term borrowing and not a trade payable. What I understand about trade payable is that it is for inventory purchases. This is there in reports from 2014 through 2016, disclosure first appeared in 2015. There is no acceptances part in 2017.

Why cant the company include these in short term debt?

Other related observations:

a. 2014 AR – 900Cr of personal guarantee by the promoters. However the total reported debt is less than 100 Cr.

There is a 370Cr guarantee for private subisidiary loans. Moreover a good % of promoter shares are pledged – 9% in 2012, 4% even until 2017.

b. The reported total debt was 14Cr in 2016 (not considering the acceptances part). However 4% promoter shares are still pledged. Why?

c. Also, in 2016, for a debt of 14Cr, the total interest in P&L was 15Cr. CFO shows interest paid as 6Cr.

d. The interest amount is at many times not proportional to the total reported debt.

- 2012 AR - Revenue recognition changed from dispatch from factory gate to delivery to customers. It is disclosed but the effect is not clearly shown and compared against the same for previous year.

- 2011 AR – Inventory cost method changed from weighted average for entire year to weighted average on rolling cost basis. This resulted in the increase of 4Cr in PAT. However, other earlier and later AR’s disclosures just specify only about weighted cost. Why change only for one year? 2012 is the year where the last recession phase started (2012 to 2014 were bad years)

- 2012 AR shows that other assets contains ancillary costs for arranging borrowings – 3.7Cr (2Cr for 2011) is capitalized. Is it ok to capitalize bank costs for debts?

- 2007 AR – debentures converted at 62 Rs in June 2007. The share price back then was aprox 40 Rs., split adjusted. I do not have full AR, hence not clear who was these issued to – is it to Clearwater? Is it ok to do this way? If it is to Clearwater, I suppose it is good for the company and shareholders, as the shares were valued more than the then market price.

However in Aug 2010, shares allotted to Clearwater at 95 per share, when the market price was around 150Rs.

I welcome your insight on this, and would like to correct myself if I interpreted any data wrong.

Thank you

Wish you all a Happy and Fruitful New Year!

35 Likes

Thank you @Prasad_India.

I look forward to opinions from you all so that I can be better informed and learn further.

To add to my earlier comments/questions. When we look at any fiddling of numbers up by the management , it is not complete without considering what are the incentives and what have they gained out of it. Following is what I can think of, assuming that what I read and infer from the AR is correct:

-

Obvious enhancement in profitability as follows:

-

This in turn will augment the ROE and ROCE. Especially when ROCE is one of the ‘Lakshyas’ of the company. (ROCE 33% is one of their financial goals) and they flaunts ROCE for sure.

-

With the use of short term debt for long term investments, and masking of short term debt as payables, ROCE is further augmented (though this specific part is small, when combined with the profit booster it does make a difference) and BS look tidier.

Notwithstanding the boosters, the numbers and BS look ok until 2015 (on a second thought, this is also questionable for a top OEM supplier with around 60% of the market and the top player in India and the third in the world) and company seems to take off from 2016, apparently due to new products. However I would not want to analyze the company further if the management has a continuous tendency to make up numbers, even if at a small scale.

I welcome further opinions on this.

15 Likes

Interesting announcement that goes almost unnoticed – the company is getting into Composites.

The global trend in leaf springs is to replace Steel with Composites, such as CFRP (Carbon Fibre Reinforced Plastic) or GFRP (i.e. glass based). Composites are 50 to 65 % lighter than steel but provide the same or higher level of strength to weight ratio. They are also cheaper, more convenient and long lasting. ARC Industries, Ichalkaranji , Maharashtra claims to be the only composite leaf spring suspension maker in India presently, with clients such as Mahindra, Ford, Toyota, Chevrolet etc. Though market for composites is currently small, it is growing faster than steel springs.

4 Likes

Jamna Result announced today :

BIG jump in receivables.

Both in receivables and inventory,'Is it a cause of concern or a one-off?

@johnsgeorge.cet wonderful work. I was about to start researching given the ‘positive’ news flow about the company. This gives me a very good picture of what to watch out for

As an after thought, seems like most of the issues were in the pre 2016 era, wonder if it had anything to do with increased institutional interest, and as a result Jamna also being more prudent with their practices. This is also borne out in your restated profit being almost the same as reported profit for the last 2 years

1 Like

please note that recent quarter result shows high receivables and short term borrowing increased around 10 times.(may be some red flags).

1 Like

Also, the D/E ratio is now 0.5 instead of 0.1 as earlier. It’s a huge issue for a company of this scale. The increase in receivables and inventory signals to a possible rejection of a big order (may be due to quality issue or something like that).

I would suggest to stay away till the next quarter or if the management clarifies on these issues.

1 Like

Thank you @arhagar  .

.

I think practices and processes can be bettered, however I doubt if the character of the management can be or will be changed for the better.

The results may be getting better, however I did not look into it after my last one, as there are better options. However once I update myself with the latest, I will add further.

2 Likes

Was taking a look at this counter. The high receivables to 191 cr is a red flag. Any update from the management on this? I don’t see an Annual report for the current financial year. One interesting thing I noted was the rise in payables as well although not as much as the receivables.

even though the recievables hav increased, the major clients of the company are tata motors ashok leyland and the likes. I dont expect them to default or d receivable going bad. However this will increase the working capital requiremnt.

1 Like

Hi,

I was just going through some past annual reports, one thing I noticed is since 17-18 (i.e.post application of IndAS) the company has stopped reporting PRODUCT WISE revenue. I have two questions.

-

Why it has been stopped? (Was there any rule binding the companies to do so and now that rule has been removed OR is there any rule now, that is stopping the companies to do so.?) (Also, I have seen the same thing in PI Industries)

-

In absence of annual report, where I can find that? (I have checked investor presentation but couldn’t find the same.)

When the Company is saying that it wants to stop relying on just one product, the product wise reporting becomes more important to check the validity of companies’ claims. And surprisingly that is stopped now. Why?

At a very high level, below is revenue split between key segments:

Leaf Spring = ~66%

Parabolic Spring - 23%

Lift Axle+ Air Suspension = 10%

Another way to track performance would be to look at the volume growth (please keep in mind, Parabolic spring has approx 22%-25% higher realization):

As an aside, this is another counter where info in public domain is very limited. I am still trying to figure out the 'WHY" part of it, however few things really stands out. Cash conversion cycle (specifically the inventory and DSO) looks to be very good for a company catering to cyclic business and have commodity products (short of):

|

Disc:

Currently no position, Have positive bias. Please do your own due diligence.

Thanks,

Tarun

2 Likes

Hi Tarun,

Thanks for an insightful reply. Just curious to know from where did you find the information on product wise volume growth i.e. the first snippet attached.

And the “Commodity Products” word caught my attention. Just curious to know two things on the basis on that.

- Why you think the products are commodity? Do you think the company is/ was earning economic profit, if yes, can you opine why it can do so while having commodity products?

- I noticed that you are positively biased on this. What thing makes you positive on this, valuation or business or both?