Income Tax Exemption is at Trust Level but SPVs have to pay Income Tax.

The way to reduce tax at SPV level is to invest as Debt from Trust to suck out the cash flows. Hence, effective tax is lower than corporate tax rates.

Yes, as of now there is no tax at SPV level as well but in future due to debt repayment to trust, they r likely to make reported profits and hence will be taxed. However, there is also a view that trust may increase interest rates being charged to SPVs in future to avoid any large tax outgo

yes, but that wont help a lot in reducing the tax effect in medium to long run. Tax Authorities allow inter group loans to be charged 200 to 300 bps higher than interest rate but beyond that they don’t.

The better method would be to raise fresh equity as primary capital and pump into subsidiary as Debt to reduce tax liability.

And what SPVs will do with that money raised at an implied cost of 14-15%? Its probably not the best way to look at it

I agree that they wont be able to raise interest rates beyond a point, so essentially they will balance it out and pay some tax. But it will take at least 3-4 years before any SPV starts showing material book profits

In any case, tax at SPV level wont affect much the post tax IRR of unitholders. This is because interest payment to unitholders will be getting partly replaced by dividends. So today on interest, unitholders r paying ~35%+ tax. Once dividends r paid, SPVs will pay 25% on profits and unitholders will pay 10% on dividends. All in all tax liability of SPV + unitholder put together will remain in similar range

I think if i remember correctly there is no DDT on SPV of an INVIT, but i am not sure and need to recheck

its an incorrect assumptions that income tax would have no effect on returns. SPV level income tax would reduce dividend yields by 2%-3%.

I would check and get back about DDT at SPV level, but main criteria for improving yield is to ensure Income Tax at SPV level is nil or negligible.

FasTAG implementation going through its bumps. The deadline has been pushed to 15th Jan now.

Users have reported issues like double debits, incorrect RFID readers etc.

Disclosure: Invested in IRB InvIT. Less than 5% of my portfolio.

I did some digging through the September valuation report to figure out the DPU split by asset.

There are only 3 ways an asset can transfer cashflows to the trust:

- Return of capital

- Interest

- Dividend

No asset is giving out a dividend right now. I looked at the cashflows from each asset and compiled them in the following 2 tables.

How to read the table?

- The table on top gives the actual cashflows (in Rs lakhs) for FY 19 and H1 Sep19. The cashflow is further broken down into interest and return of capital (ROC).

- The table on the bottom gives the contribution to the total cashflow from each asset.

- For example, for IDAA the H1 Sep19 figures say interest 7%, RoC 55% and total 20%. This means IDAA contributes 7% of the total interest paid to the trust, 55% of the total capital returned and 20% of the total cashflow.

As we can see Bharuch-Surat (IDAA) & Surat Dahisar projects contributed to 38% of the H1 Sep19 cashflows, down from 45% in FY19.

Disclosure: Invested in IRB InvIT. Less than 5% of my portfolio.

I drove last week from Mangalore and Goa, the road highways were built by IRB INFRA which are pretty good and covers till Mumbai and thereon to rest other cities presumably.

The highways are still under construction and the tolls are full constructed, there was none to collect tolls (my guess they would start from this year on wards to collect tolls) and also in Ankola they will be building an airport for the domestic which also would cater to the Navy…

Yes the tolls are implemented with Fast tag across and 1-2 counters to deal for cash payment collection…

Am not sure whether IRB would get the large slice of hot cake for the road mala projects with the plans of 102 lakh crore infra.

IRB Infra has received NOC from NHAI for transfer of nine of its BOT assets to IRB Infrastructure Trust (Private InvIT) and subsequent investment by GIC affiliates for 49% stake in the this Trust. IRB Infra retains 51% of controlling stake. 98% of lenders have approved their NOCs supporting the deal. The Portfolio spans across 1,200 kms in Haryana, Uttar Pradesh, Rajasthan, Gujarat, Maharashtra and Karnataka.

adf68190-5856-4f9f-a470-b64ac7d92521.pdf (374.3 KB)

The Investment proceeds from the deal will be used for deleveraging of the Portfolio and Equity funding for under construction projects of the portfolio

1 Like

IRB InvIT has declared a distribution of Rs 2.7 for Q3. Board meeting outcome is attached.

- The distribution has disappointed for 2 quarters in a row. Rs 2.5 in Q2 and Rs 2.7 in Q1.

- There was unprecedented rainfall in Q2, so we can cut them slack for that. Why the distribution is lower in Q3, is not clear right now. They have not shared any plans to have a Q3 concall.

- In the last call, the management was very confident in traffic uptick. They had also said that they are confident of adding 2 new assets by the end of FY20. No signs of that happening.

My notes for Q3FY20 Conference call:

- The slow down in economy growth has adverely affected traffic movement of CV (MAV). While other vehicle traffic growth pick up, negative growth in CV affected performance.

- Currently, FasTag account for near 60-65% of collection. The company can reduce manpower once FasTag collection increase to 90-95%. Currently, it spend around 3-5% on manpower. On achiement of 90% collection, it could reduce manpower by 40%, providing around 1.5-2% gain to unitholder. Secondly, it estimate leakge of around 1% (which cashhandling) being improved. So expected around 3-3.5% overall improvement in toll collection from FasTag.

- Since two of major assets (Dahisar Surat and Bharuch Surat accounting for around 50-60% of cashflow would not be available after two years, the management has decided to cap the distribution at around 90% of Net distributable cashflow (as required by SEBI regulation)

- The management also explore of acquiring third party assets in distress. They would look at assets being acquired by debt (since the InvIT has option to increase debt). The cost of debt is around 9-95% while thye would look at asset IRR of 14% resulting in improvment of yield. I intend ask management what is point to acquire new assets 14% when the units are trading at 20% current yield (distribution of Rs 11 on price of around 55)? I dialled the number but for some reason could not get access to management.

- There was question about why management did not excerise first right of refusal when assets being sold to GIC? The management replied that duration of assets was around 20 years+ and may have contributed negative cashflow to trust in initial years. (Although over the life IRR would be good, but initially there was negative carry). Since the mandate is to acquire only assets which are acretive to cashflow, they ignored these assets when approcahed by IRB.

- Tunkur Chitradurga, traffic movement was lower. During Q3FY19, there was consruction of highway in adjacent are which resulted in higher CV movement. Since highway construction work is over, the traffic was affected.

On Pathankot road, while the mining ban was lifted, Q3FY20 affected by removal of 370 clause which reduce commerical traffic in J&K region. In Q4FY20, it is now moving to normalcy and company expect better performance.

On Jaipur Deoli, the Supreme court allowed mining by small units. However, that is not material for traffic. The decision on large mining approval is still pending at Supreme court. - Over next 5-6 years, one can expect 90% of distributable fund being distributed to investor. At the things stand, managment expects around 11-12/ unit distribution in next 5-7 years. In FY20, we may expect around Rs 11 as minimum distribution. Depend on how Q4 traffic and cashflow, distribution may be higher than 11, subject to 90% of distributable amount.

- In order to provide stability in distribution, the balance 10% accumulated in next two years, would be utilised as cushion for shortfall after two years when Surat Dahisar and Bharuch Surat are not available.

I still I can not understand how it make sense of for investor, when 20% yielding assets is keeping money in 12-13% yielding assets? Get cash quickly would be better for investor as keeping Rs 10 in trust, unless supported by new assets (and hence potential for future cashflow and higher yield) does not make any sense. Market is intelligent enough to appreciate volatility in my opinion.

There is scope that I may have misunderstood or mis communicated the discussion. Investor shall visit company website and read/listen conference call details which shall be available in couple of days.

Link to Q3FY20 investor presentation:

Discl: I am an investor in IRB InvIT. My view may be biased due to my investment. The invetor shall do their own due diligence and/or consult SEBI registered investment advisor before making at decision.

3 Likes

When was the announcement for the concall made? I don’t seem to find it on NSE/BSE announcements page and company’s announcement page.

I listened to the concall recording uploaded on the website. I noticed 1 big red flag. The company is not uploading the presentations on BSE/NSE. They are only uploading on the company’s website. An investor pointed this out (apparently he had also mentioned this in the AGM. At that time the management had said that they will fix this). Its been more than 6 months now and still no action by the management.

I wanted to ask questions to the management on 2 anomalies that I noticed in the Sep’19 valuation report. I will post them here before sending an email to the management. Here they are:

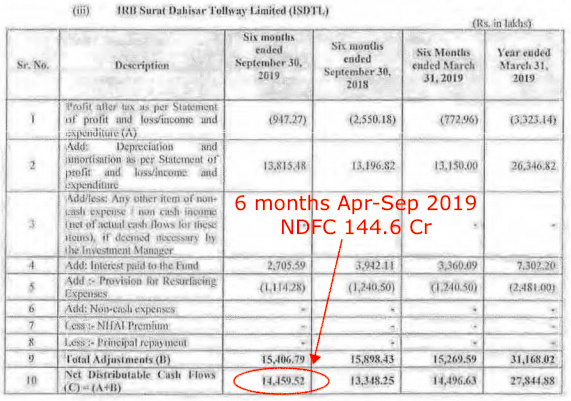

1. Surat Dahisar Cashflow Mismatch

September 2019 valuation report shows that for 6 months (Apr-Sep) the NDFC generated by the asset is Rs 144.6 Cr.

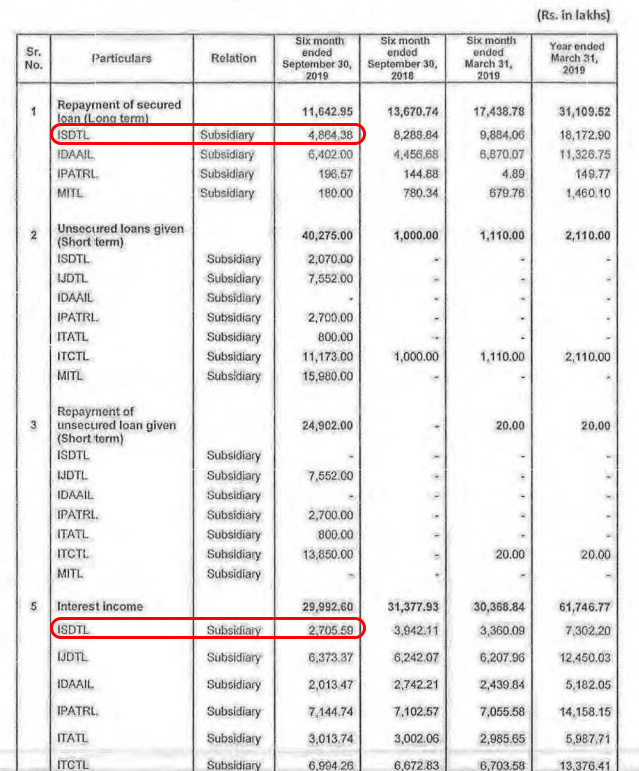

However, there is another section which shows the amount of interest paid & principal re-paid by each SPV. Surat-Dahisar project paid Rs Cr 27.05 Cr as interest and repaid Rs 48.64 Cr of principal, during the same 6 months. This adds up to Rs 75.69 crores. There is a shortfall of about Rs 69.53 crores.

I have double-checked this number and when take you take into account the cashflows from other SPVs, the entire total matches with the NDCF table of the trust. I also posted a screenshot about the same in my previous post.

So the question is - how do we account for the shortfall of Rs 69.5 crores? Is there some revenue sharing arrangement with NHAI, that I am not aware of? That is very unlikely because any such revenue share would have been shown as a negative entry in the SPV’s NDCF table.

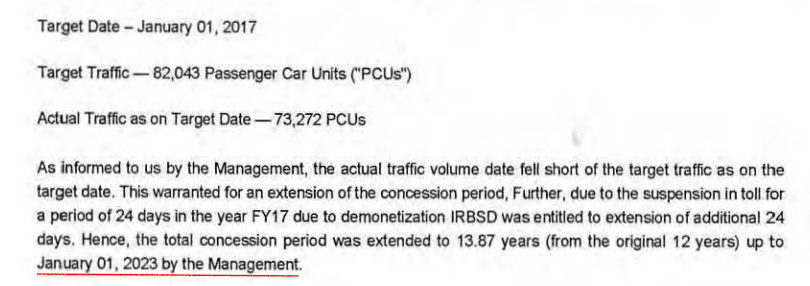

2. When does the concession period end for Surat Dahisar?

In the report it is mentioned that the “management” has extended the concession period of the asset to Jan 2023, due to shortfall in traffic. See this screenshot.

While arriving at the valuation of the SPV, they have considered cashflows till Jan 2023.

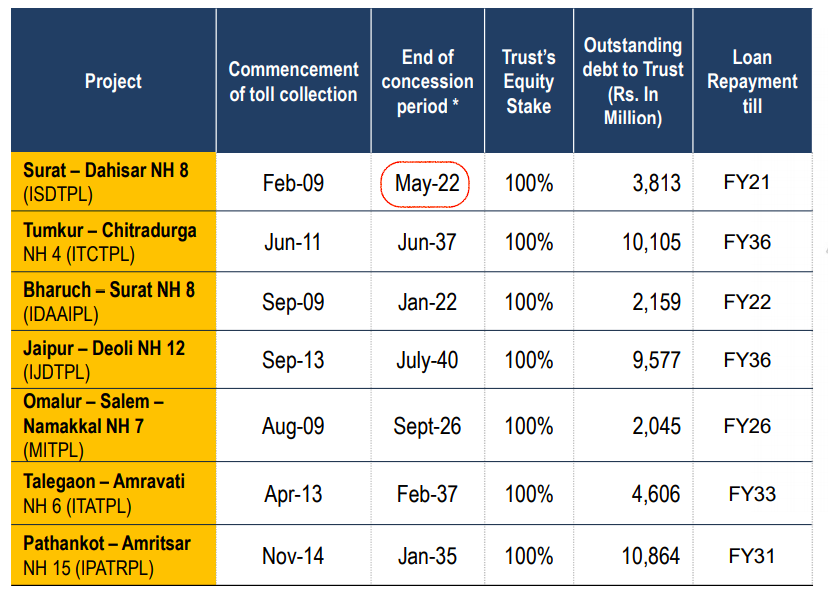

However in their presentations they mention May 2022 as the end of the concession period. This screenshot is from the Q3FY20 presentation:

4 Likes

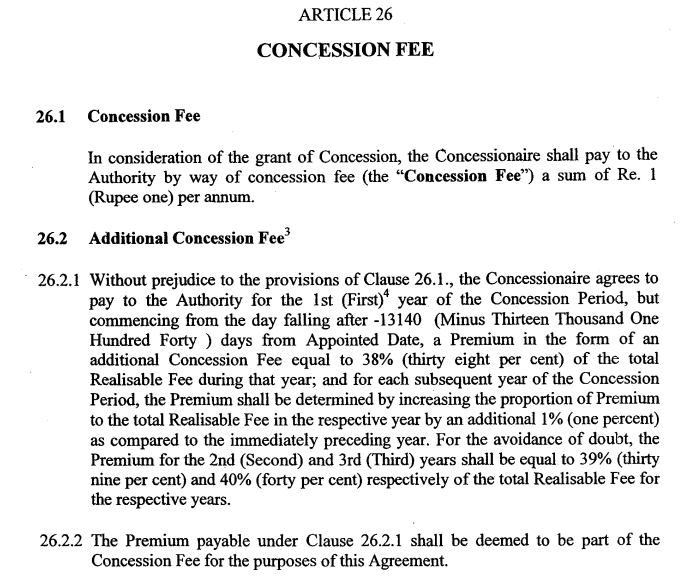

I found the answer to the first question. There is a revenue-sharing agreement for the Surat Dahisar project with NHAI. The share is paid as a concession fee. The concession agreement is available on IRB InvIT’s website. Here is the link - Surat Dahisar Concession Agreement.

Here is the relevant clause:

So the fee starts at 38% in the first year and then increases by 1% every year. So for the second year, the fee is 39%, third year 39% and so on. For FY20 the fee seems to be 48%, which tallies with the agreement given that it was signed in April 2008.

The valuation report also says this:

Revenue share is only for 2 assets: Surat-Dahisar and Omalur-Salem.

But now this raises a new question - Why is the revenue share not excluded from cashflows for the valuation of Surat Dahisar project?

3 Likes

@fabregas, Excellent work to go through report in details and come with great finding. I appreciate your efforts and diligence.

Since you have got first issue addressed, I would try give my understanding about the second issue (related to including NHAI revenue being considered in Valaution). Please note that this is based on MY UNDERSTANDING which may be WRONG.

I refered to Annual report for FY19 (since that is were latest actual data is available).

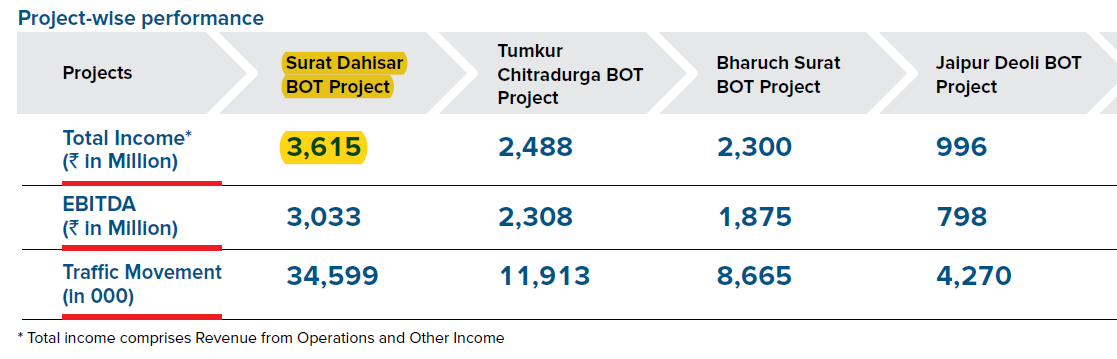

In FY19, refer to Page 18 which provide details of Project wise “Gross” toll collection:

So in FY19, Gross toll collection from Surat Dahisar is around Rs 677 Cr.

Now I refer to table given on Page 6, providing details of total Total income from key projects table.

In FY16, total income from Surat Dahisar project is Rs 361.5 Cr. If we take Gross collection of Rs 677.1 Cr, the Total income form SD project is around 53% of Gross toll collection. The balance 47% I assume to be NHAI share which is what covered broadly in concession agreement.

So, from above, I interepret that the company take only its share of Gross collection of Toll (around 53%) and same cashflow are being used for valuation. I feel that is correct way to estimate value of the assets. Do let me know in case there any weakness in my understanding.

Once again appreciate your efforts and making thread more meaningful.

Discl: I have investment in IRB InvIT and my view may be biased. Investor shall do his/her own due diligence before making any investment decision.

1 Like

for its valuation report, IRB INvit has assumed a revenue growth of around 11% for the rest of the life of assets. is it feasible given that traffic growth has been subdued recently and economy is also not growing very strongly.

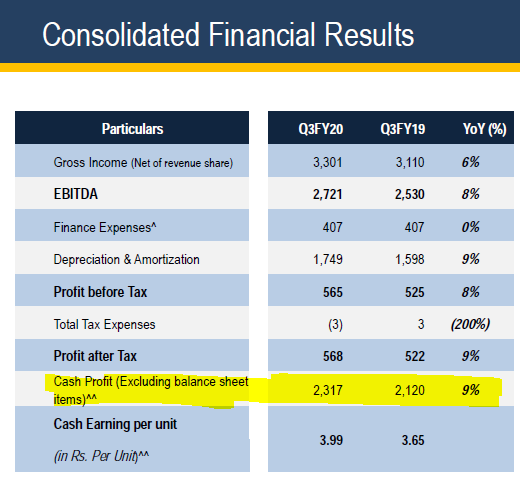

I am scratching my head , trying to understand that despite a better Q3 (Q3-FY2020 vs Q3-FY2019 - see below), why is NDCF (Net Distributable Cash Flow) for the same comparable period is low (Rs 2.7 Q3 2020 (this Quarter) vs Rs 3.1 in Q3 2019).

Management did say in Concall that they are limiting the NDCF to 90% starting Q3 2020, however, during Q3 2019, NDCF was close to 95% , not much difference.

The only reason I am able to draw, is additional NHAI Premium which was deferred in past, being paid during this year for Tumkur Project.

@dd1474 @fabregas Am I correct? Or I am missing something?

3 Likes

Excellent work Amit. However, the distribution of cashflow from InvIT is not exactly comparable with P&L Cash profit. The major contributor to difference being net debt repayment received by InvIT (Debt repayment received from various SPV-Debt repayment made by InvIT to external lenders). Also, expenditure at Trust level (valuation, investment management fees etc) and income at Trust level (interest on excess cash and bank balance) would also add up.

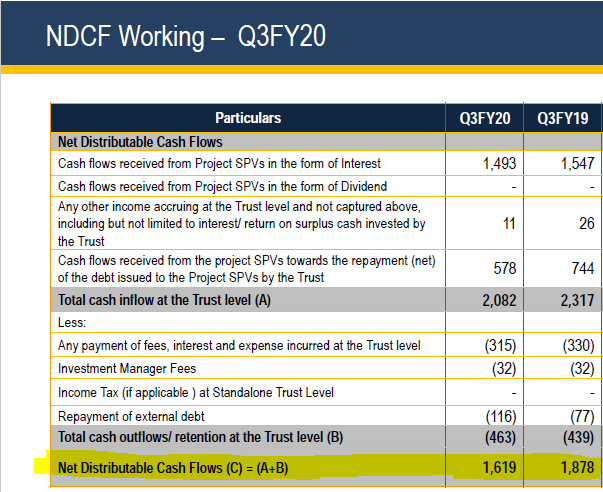

In order to get more understanding on these issues, I try to calculate qaurterly NCDF for InvIT from various presentation. Find enlcosed my working for your reference.

Cell marked in Yellow colour are Investment management fees in previous quarter, which was merged in Expense incurred at trust. (Frm Q3FY19 Investment management fees was available in presentation and hence shown seperately).

When I Compare Q3FY20 with Q3FY19 for NDCF, i find decline of Rs 26 Cr, Rs 23 Cr was due to lower inflow from SPVs (Lower interest of Rs 5.4 Cr, Lower Debt repayment from SPV to InvIT Rs 16.6 Cr and Lower investment income of Rs 1.5 Cr) and also higher cashflow outflow at InvIt level (Higher repayment by InvIt to external lenders Rs 3.9 Cr, parially compenseted by lowerTrust expense Rs 1.5 Cr).

I also tried to reconcile Six monthly InvIT NDCF and addition of individual SPV NDCF disclosed in Sep/March results.

There is difference of Rs 73 Cr (FY19) or around 37 Cr (6MFY20), that broadly InvIT expenditure at Trust level of around 37 Cr for a quarter. So every quarter there is differnece of Rs 35-40 Cr between SPV NDCF and InvIT NDCF which could be due to net debt repayment etc.

The difference in NDCF is not due to deferment of NHAI payment. I enclosed my working NDCF (complied from Sep/March results) which specifically adjust NHAI payment from NDCF for Tumkur Chitradurga Project.

Hope this clarify your doubt. Please note that I am not expert and this is my understanding of InvIt cashflow from reading results and presentation. In case any inconsistency in working, feel free to put on the board.

Discl: Holding IRB InvIt, my view may be biased due to my holding, not a SEBI registered advisor, investor shall conduct his/her own due diligence before making any investment decision.

3 Likes

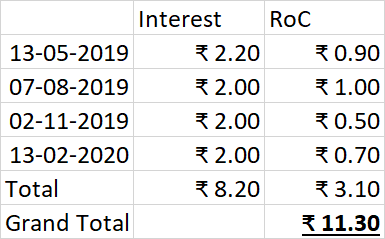

IRB Invit returns money to investors in 3 ways

- Dividend

- Interest

- Return of Capital.

In the last 1 year, they have given 4 distributions - 3 distributions of this financial year & 1 distribution of the previous financial year. I assume they give 4 distributions every year.

They did not issue any dividend in these 4 distribution. They issued only Interest & Return of Capital (RoC)

For each unit, this what what they returned

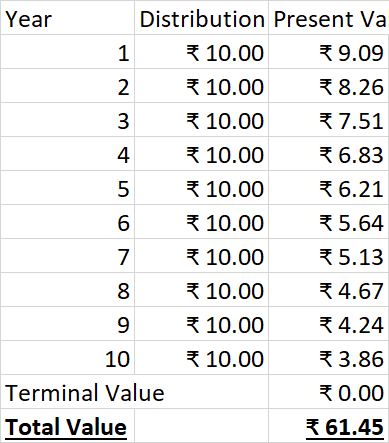

So, it’s Rs. 11.30 per year per unit. Now if we assume that they return Rs. 10 year (instead of 11.30) & they continue returning this for 10 years and then they shut down with the Invit Price going to Zero (i.e. you cannot sell it at the end of 10 years).

If we calculate Present Value based on this at a 10% discounting rate

So current price based on this should be at least Rs. 61.45. But it’s currently selling at Rs. 44.45. So why is it so undervalued? Does the market not believe that they will be able to last even 10 years? Or does the market think they won’t be able to give at least Rs. 10 per unit for 10 years?

If they give Rs. 9 per year for 10 years, even then it should be worth Rs. 55.30. At Rs 8 per year, Rs. 49.16

The current price justifies just Rs. 7.20 per year for 10 years with no residual/terminal value.

If someone buys now at the current price, it will be a great return if the Invit is able to deliver Rs. 10 for 10 years.

2 Likes