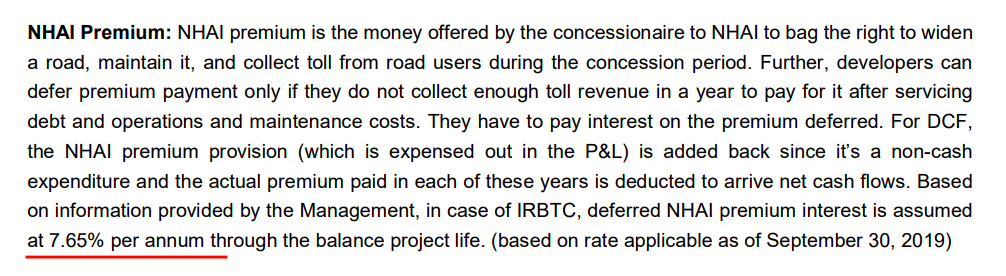

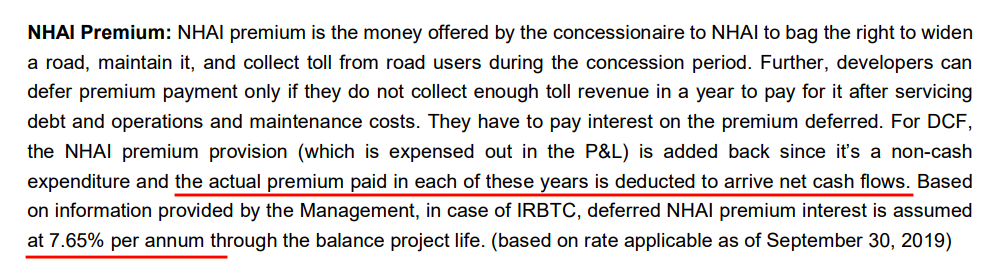

Just to give some background on this ‘premium deferment’ issue. Some of the BOT (Toll) projects (Not just IRB, but across developers) were under stress due to lower toll collections. Payment of premium was affecting servicing of debt. The loans, provided by banks, would have become NPAs had the developers continued to pay the premium. To prioritize servicing of debt and operating expenditure, NHAI allowed the SPVs to defer payment of premium until toll collections improve. This was in the year 2014. Here were the deferment terms:

- NHAI will allow the developer to pay 25% of what they actually owe (i.e. 25% of the annual premium) NHAI during the first 3 years; thereafter, the amount will be raised to 50%.

- The balance amount (i.e. deferred premium) will be treated as a ‘revenue shortfall loan’ and the interest will be payable to NHAI at 2% above the bank rate. The interest rate is around 10.75%

- The SPV will not be allowed to pay any dividend to the parent until it pays all its dues (deferred premiums for the previous years) to NHAI.

My source for deferment terms is this article - NHAI shelves premium payment of nine road projects.

The terms for the ‘revenue shortfall loan’ are mentioned in the concession agreement, which is present on IRB InvIT’s website - link (Read page 75).

Here is an extract from a news article:

A project, once classified as stressed as per the Rangarajan formula, will be allowed to postpone premium payments to the following year under Article 28 of the Model Concession Agreement. The rescheduled amount will be treated as a revenue shortfall loan. Once toll collections pick up and the revenue shortfall is eliminated, the developer will have to pay the premium along with the deferred amounts and interest thereon. The discounting rate in order to ensure that the net present value of the premia doesn’t change is determined at 10.75%.

Source: IRB is first to sign up for road premium recast, takes 2 projects to NHAI

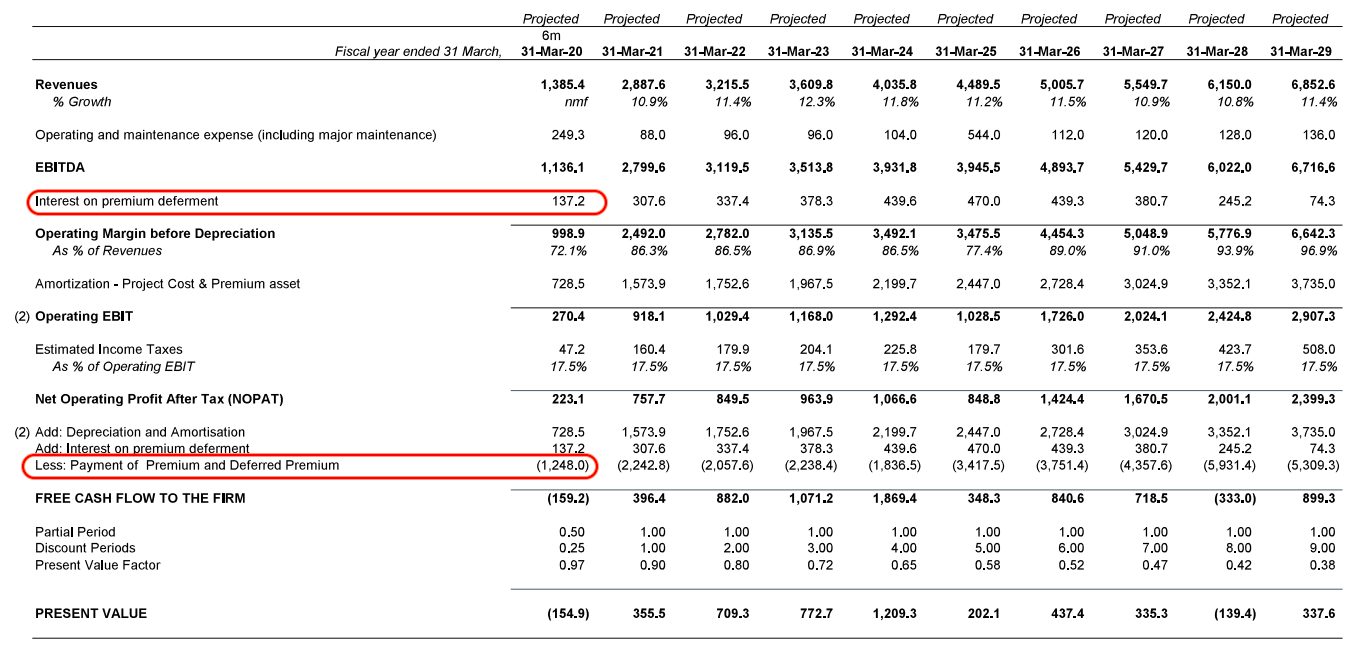

How much is the premium?

Starts with Rs 140.4 crores and increases by 5% every year. Source: Concession agreement from IRB InvIT’s website, link above.

The above news article also mentions that:

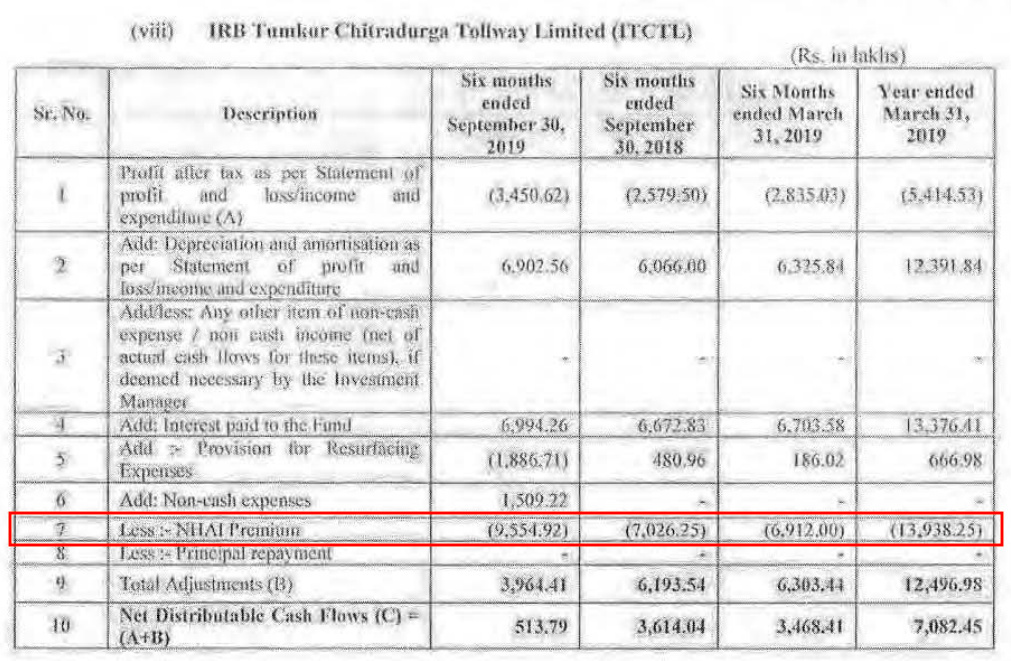

In the case of the Tumkur-Chitradurga project, the premium sought to be postponed is Rs 90 crore.

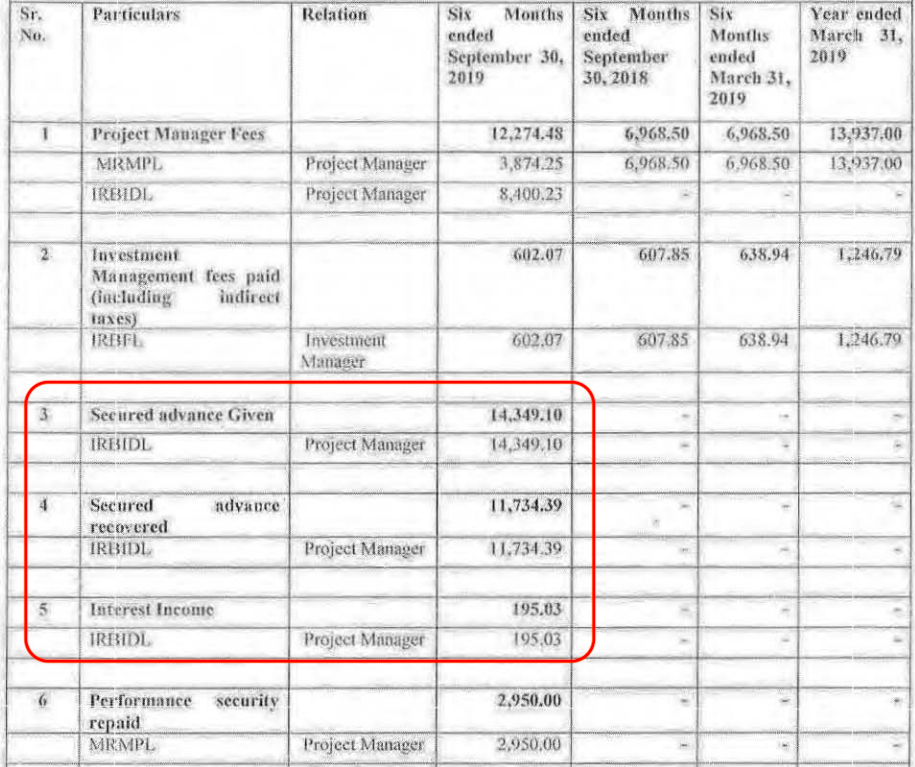

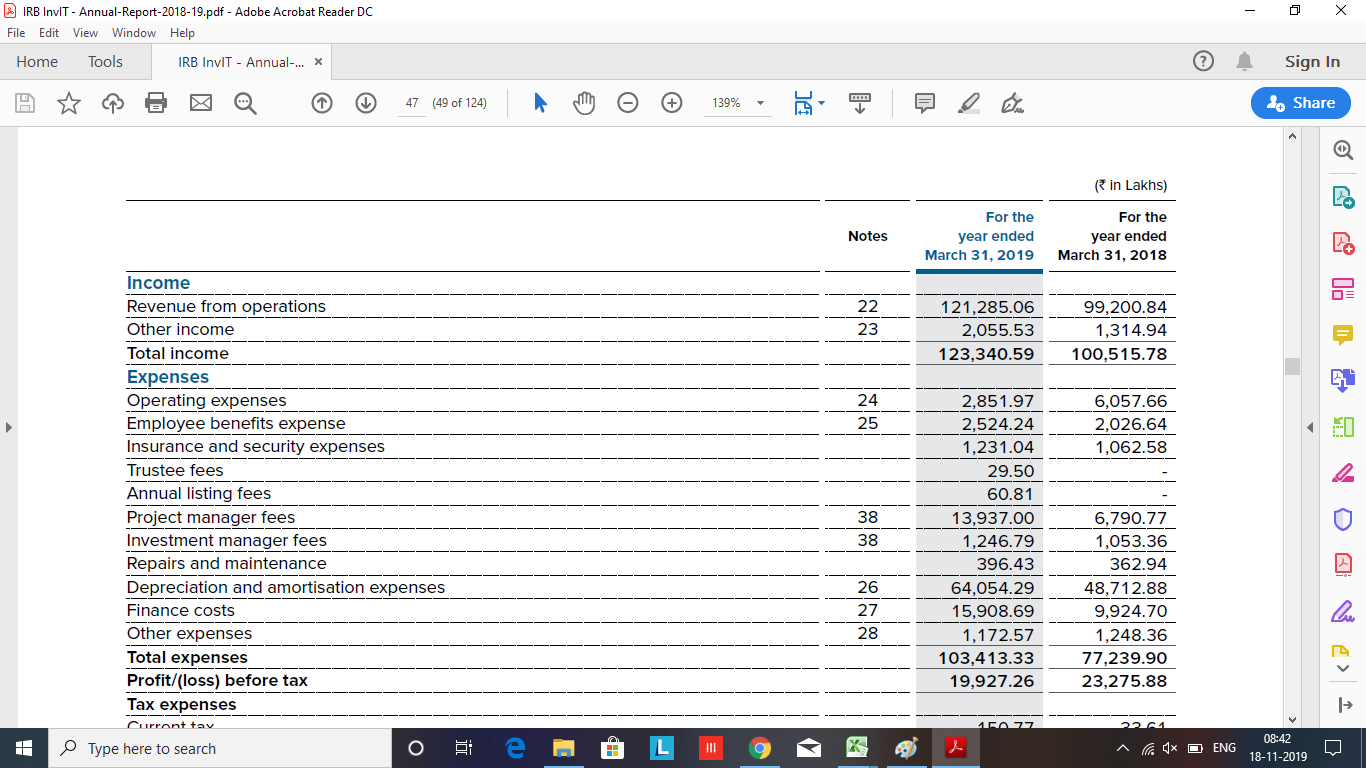

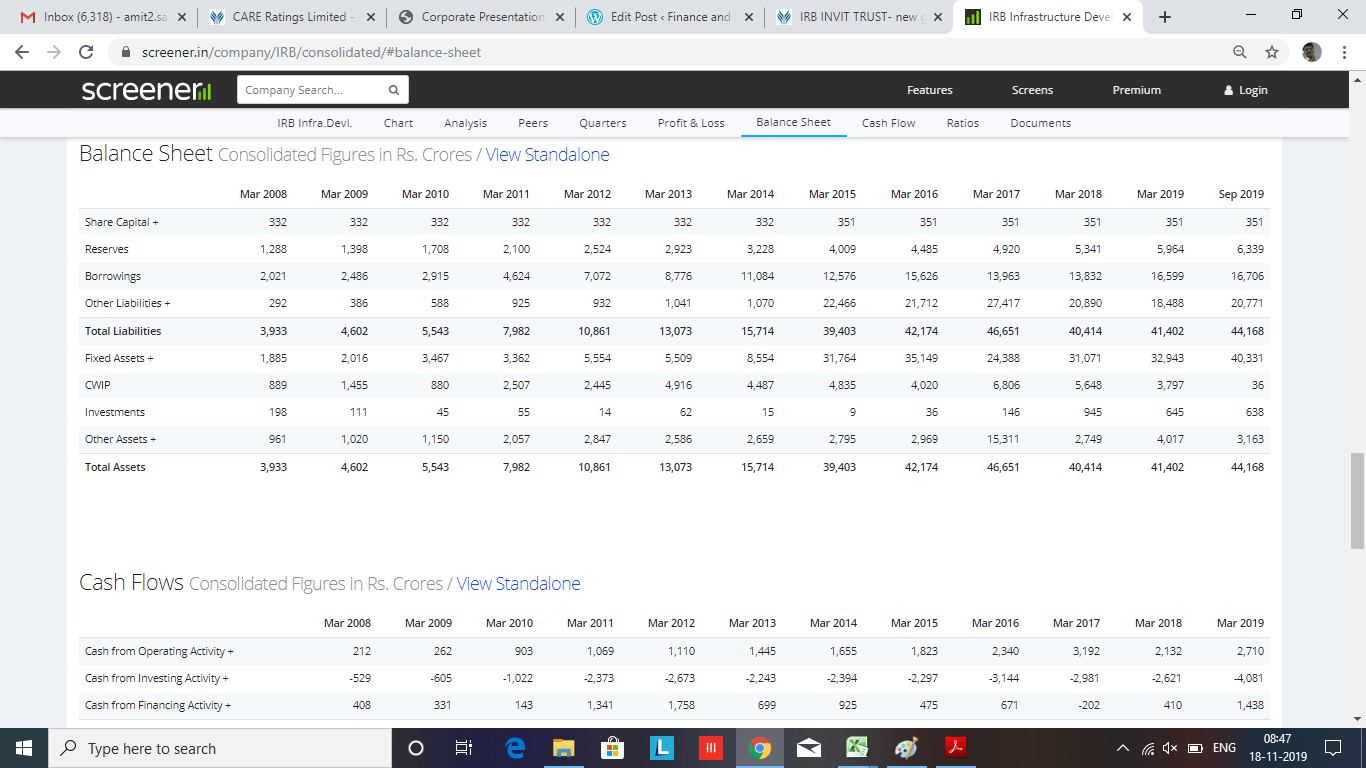

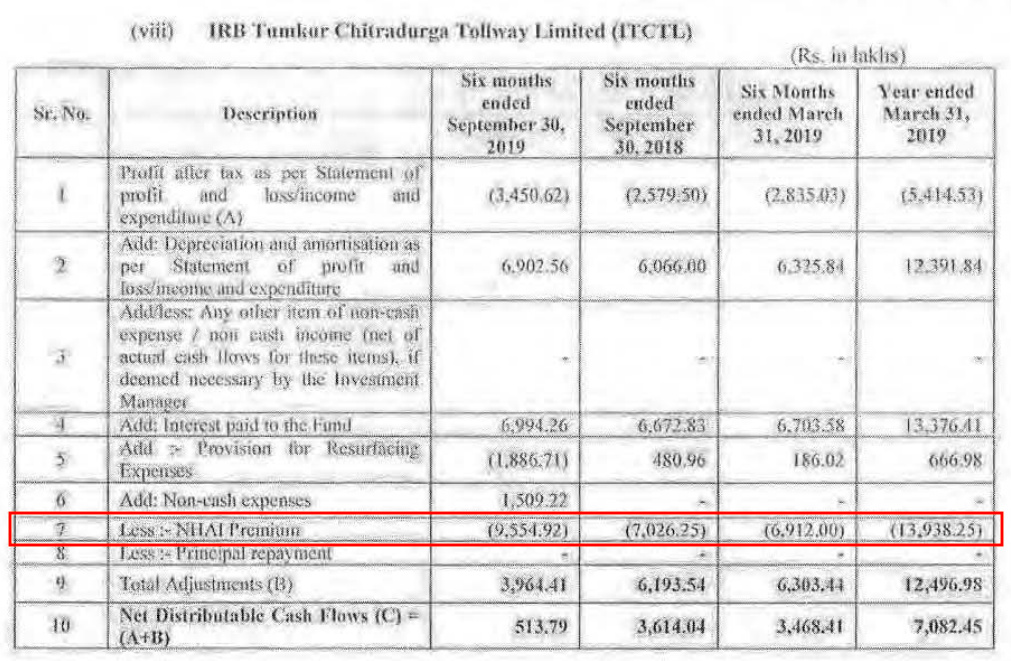

So IRB has not deferred the entire premium payment. And by now IRB must be paying almost 100% of the annual premium. The cashflows statement of IRB Tumkur Chitradurga Tollway Limited (source: Half year report September 2019. Link) confirm this:

The report says it paid a premium of Rs 139 crores in FY19.

@Amit2saxena Please correct me if I am wrong somewhere.