Although you have asked the right person and his insights would be- and always are -worth reading, I could not resist to poke in to stress that do make sure to read the book named as The Most Important Thing by Howard Marks in order to quench you aspiration to know and understand behavioural finance.Even if I tell the definition, it may not be of much help.But Marks masterpiece explains the meaning beautifully in the context of equity investing.

1 Like

Applying rationale decision making in a financial process would be short cut for good behavioural finance. Let me try to put a small gist of my understanding:

We all humans have a brain which consists of compartment (right, left with a core brain).The side of brains unfortunately have different capabilities, for example left side of brain has limited capability where as right side has almost infinite capacity (99.99% people use left side of brain only!). Each compartment consists of attributes with which we are born, some we develop. These attributes are bad and good both. Say one attributes are the biases we born with, say like over confidence, arrogance, temperament etc. Challenge is while applying these attributes to different aspects in life can be total contradictory. For example what attributes you use during employment are completely upside down when it comes to investing or entrepreneurship. For example buying a cheap product on sale is good only for us, but when it comes a cheap share may become nightmare by falling another 80%.

These biases can be overcome through studies and habit which is ongoing process as we know. Say relegious books provide you nuggets as to how to overcome fear and greed. Or say more samples increases accuracy of analysis (not necessarily true for all cases).These habits and act of practices are also called wiring between core and right/left brain. Wiring to right brain is much more complex as its not an objective compartment.

Take this way:

Core Brain WIRING to Left Side: Analysis, practices, higher sample, in depth studies etc

Core Brain WIRING to Right Side: intuition, gut, unusual habits (like act of doing less, beyond the rules etc).

(different terminologies used for these neural finance like Second system thinking/brain, NLP, R-Mode thinking etc).

These wiring will help you to take a proper decision while buying, adding, holding or selling shares.

Risk tolerance is how much risk you can take against each financial decision. I just wrote a piece on Risk of Ruin under this, classic example of risk tolerance.

Lets continue to debate and discuss on these subjects.

3 Likes

A higher tax provision than required can either be a. impending trouble or b, management conservatism.

Higher tax rates are provided when either expenses charged to PL by management are expected to be disallowed by income tax like penalty, provision against contingent which management feels can be challenged. If this is the case I would have expected to disclose them in foot notes.

Higher tax provision can come when management feels revenue deferred can be challenged by income tax. This is a regular problem of media companies. Management goes conservative and provide higher taxes to be in safe side.

Saying that 60% plus is a big number, must be one time adjustment which is expected to be disallowed. Please search notes to accounts and directors report if commentaries provided.

Your second question:

This is the minority interest, with IFRS it is called non controlling interest. Basically this is the ownership of a subsidiary not attributable to parent company who has a controlling interest (meaning more than 50% but less than 100%).

IFRS change the disclosure to separate section now. Previously net income attributable to non controlling interest was recorded as an expense while calculating net income. Now both net income for controlling interest and non controlling interest presented separately.

The minority interest calculation has got guidelines, you can go through them.

Thanks

3 Likes

No you will not unless you work for an institution. In case you are working you are abide by non trade clause.

1 Like

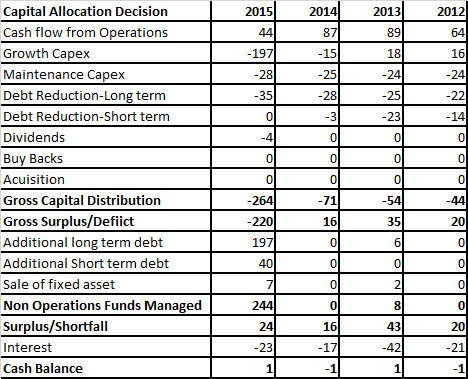

Great question, I use five year cash flow to form an opinion. Let me paste you an example:

First decision making point:

Capital Allocation Decision, Company name: Nitin Spinners

Company has not been successful in managing its operational expenses, growth is only supported from additional borrowings.

Below is the table showing cash generated and distributed:

During 2012 and 2013 company couldn’t generate enough cash even to spend capex on growth. The debt and interest liabilities were enough to eat up the entire cash flow. Also we can see there was no money to maintain the asset, company have avoided proper maintenance.

During 2014 situation marginally improved when Nitin managed to spend 18% money on growth capex out of free cash flow. We didn’t see any short-term debt repayment.

During 2015 Nitin has taken up expansion plans with a 200 Cr expansion. This is completely funded by long-term debt. To support the ongoing maintenance of asset short-term debt has been raised.

Please let me know questions if any.

You can not predict expected annual growth. Even management does not know fully, you can management guidance if available.

I use PE ratio is crowd expectation on growth, higher the PE higher growth expectation by investors. But again crowd can change their opinions too often.

In short I won’t rely on these type of ratios with variables which are highly unpredictable. Better use a method based on both balance sheet and EPS like Bruce Greenwald- franchise model.

Hi Thanks a lot for your reply. So what I understood is that initially for 2012 and 2013 cash from operations is eaten away in paying interest for debts. And in 2014 just that debt has reduced so interest was less and hence that went into capex (as cash from Investing) increased. And then in 2015 all the capex growth came from getting more debt. (Please note I used screener.in only and not annual reports). Since I am still understanding could you confirm the figures you got must be from annual report as such detailed figures like maintenance capex is not available otherwise. So here there are few more things I like to question.

- How come price increased 3 times (from 2014 to 2017) without any meaningful business improvement?

- How can we know the capex expansion is rightfully for business and not something unrelated or useless? little subjective question but where we can get such information?

- So the quickest way to know profit of business going back to business is :- (a) cash from operations increasing and (b) cash from investing increasing (ie going more negative). Am I correct? or there is any other way. like asset turnover, return on asset, capital changing etc

- Also if lets say company is not increasing capex but producing more output from buying more raw materials or spending on processes improvement etc. how can we know this meaningful spending of money by the company? what could be quick way to know this?

regards,Saurabh

Company does not have statutory obligation to disclose maintenance or growth capex. We have to estimate by ourselves. There are different methods of estimating maintenance capex. For simplicity I have used depreciation as maintenance capex. Fixed asset purchase minus maintenance capex becomes growth capex.

Please do not use over the counter numbers such as online site for capital allocation analysis. In my take apart from screening of stocks the numbers are subjective and not reliable due to algorthim build in. I have written about it one of post. I prefer to take number from line item from AR and load to excel for my own analysis.

Question 1

The price increase can be a. speculative b. expectation c. value catch up. Now timing of price and fundamental catch up can drift for years. However if we look at fundamental:

Look at ten year financials, you will find substantial increase in revenue, net income and free cash flow. The effect could be seen on most of profitability ratios like ROE/ROA and cash flow indicators. So yes there has been a fundamental change in positive sense, but not on own strength. So once initial value caught initiative buyers become reluctant to pay additional price. Speculators dropped themselves as well (you can see significant decrease in volume).

So yes, sustainable self sufficiency is debatable here.

Question 2

Yes, it is subjective; still we can triangulate from different sources.

One if capex has been used for business you should be able to see increase in production numbers (consumption). Or even increase in revenue.

Two You can check rise in expenses like maintenance, fuel etc.

I would be hesitant to use below the line numbers like profit etc here as under margin sales may not increase profits despite increase in asset base.

Question No 3

I use cash flow as due to nature of information like investing, operations and finance. However this is not the only way.Now lets look at this, a free cash flow generated by company can be used for

- by paying dividend (financing activities)

- by buying back shares (financing activities)

- by acquisitions (investing activities)

- by reinvesting in business ( a new line of business or invest to existing

business as expansion- Growth capex) - by retiring debts (financing activities)

The best way I could find them is cash flow statements. Problem with any ratio would be variable inputs. Yes, asset turnover is helpful. ROA I am skeptical as return depends on many other inputs like efficiency of working capital, inventory adjustments etc.

Question No 4

Operating leverage is a significant indicator to ensure a production increase comes without capex. Meaning static fixed expenses distributed to higher units.

Lets triangulate why this situation would happen:

a. use idle production capacity. Meaning installed plant was not fully operational due to demand or other issues.

b. the production value chain is modified to squeeze more out of assets like production input/output process.

c. plant was designed for phase wise productions. This would mean you build a plant keeping an eye to five years/ten years in future. However some portion can be used after moratorium period. Even cost were spent but production was not on.

d. there can be management decision making where growth capex has been outsourced (like enhancements to existing plant) as AMC or other category expenses which are debited to PL. In this case asset won’t increase but expenses will. This would create an impression additional production without capex increase.

Not sure about short cut, all depends how we triangulate a particular case. If you have a case study (company) please put it across. We will give a shot together!

2 Likes

Hi,

Thanks a lot for the explanation. It is indeed quite helpful for me. Sorry as of now I do not have a case study of a company depicting such trend. As I come across I would sure discuss with you. I have one more question.

Suppose average Return on Equity for a company is X over past few years and lets say its earnings are growing on an average at rate of Y. Then is it possible to assign it a suitable PE.

Regards, Saurabh

1 Like

Hello Sir, From where can we get the figures for Growth Capex, Maintenance Capex.

For Saurabh

A growth on return on equity is managing profitability with optimum amount of owner’s (equity) capital. So ROE can either increased by increasing efficiency of working capital or assets (tangible and intangible both) or use other’s money as leverage to make more money (like get funding at 10% and make 20%, so additional 10% post interest payment comes straight to equity holders). As you will notice ROE uses variables from financials.

On other hand PE ratio values a company on multiple earnings meaning it assigns an expectation basis future earnings estimate to current earnings. Why one would pay for future earnings as estimate? Simply because one is expecting company to retain same set of EPS or higher EPS. Hence it boils down to identifying a question how would we identify a company that is going to increase or sustain earnings. This actually open’s the entire investment theory. I would suggest to read my thread Guru Mantra and other related threads on topic by others which covers competitive advantage, good management, leverage etc. In short these catalysts assure that management will be able to maintain current or enhanced earnings. Pick up 2/3 stock thread like Avanti Feeds, Ajanta Pharma which has been growth engines. You would find lot of dissection in this respect.

Apart from that I want to share something else with you. I have never regarded PE ratio as an strong parameter in terms of valuation. Thought other useful inferences can be drawn. From Price Entertainment (PE) to Price Expectation (PE) possibly redefines my belief on crowd foot print of a stock. In straight this is how I use PE ratio these days:

- Higher PE indicates higher expectation. This is a double edge sword, if a high PE company outperforms its expectations PE re-rating is much quicker on higher side. Similarly if it falls short of estimation then severely gets punished.

- I compare a similar company on growth trajectory to find out what was PE expansion happened with other company. Suppose company A which is ex outperformer and company B is current outperformer, I check what was the PE expanded from beginning of growth to maturity growth. This gives me a rough indication which stage of maturity cycle I am in.

- I am sceptical for a company where PE is expanding but growth is not accelerating. I am ok with a company which has a 80 PE and 10% EPS growth. But moving to 100 PE with 10% growth is dicey to me. I expect 100 PE with 15% growth. There has to be acceleration in some form I.e. 10% , 15%, 20% etc.

For Pandi

We have to calculate on our own. This is an estimation to break down the capital expenditure spent a. For replacing existing asset (I.e. maintenance) b. For buying assets which were not there earlier (I.e. growth). A growing company should spend more on growth capex. Depreciation is a rough estimate of maintenance capex. That would mean total capex minus depreciation will be growth capex. However there are different methods to calculate growth and maintenance capex. If I am valuing a company I will be reluctant to use depreciation flatly.

This book covers a important ways of determining growth and maintenance capex. Please let me know if you have doubt on the explanations on the book.

2 Likes

Thank u sir, looks like I need to get into the basics of Cash flow statements to understand few things.

Can you suggest any pointers from your knowledge base any good books or any link that would help me understand. I have been listening to you tube videos but looks like I need to deep dive more.

Also my inference from going through your answers to fellow members is that Cash flow statements is indeed one of the most important aspect of studying a company in taking a decision from a value investing point of view. Am I right in my interpretation?

Thanks,

Pandi

Hi, i am new bee just started reading books like Peter Lynch N Graham but hace some practical difficulties in understanding few things . Please help me me understand few things .

- What time amd how much in year tax paid by company in India ( As Peter Lynch mentioned Oct - Dec is right time to buy shares - though not sure shot ,but reason Hi, i am new bee just started reading books like Peter Lynch N Graham but hace some practical difficulties in understanding few things . Please help me me understand few things .

- What time amd how much in year tax paid by company in India ( As Peter Lynch mentioned Oct - Dec is right time to buy shares - though not sure shot ,but reason he sought is tax filling by company )

- What’s deferred tax n what are compulsion for company to fill tax in time frame ?

- In balance sheet if company not paid tax for 3/5 years is it normal or its some kind of concession given by govt normally ?

sought is tax filling by company ) - What’s deferred tax n what are compulsion for company to fill tax in time frame ?

- In balance sheet if company not paid tax for 3/5 years is it normal or its some kind of concession given by govt normally ?

1 Like

The below 2 books should be useful:

Corporate have to pay advance tax four times in a year i.e. June 15, Sep 15, Dec 15 and March 15. How much, not easy to know, as tax statements and payments are different forms and not managed by companies act but Income tax act. If you can get a quarterly cash flow statement you can see tax paid. The tax provision should tell you how much management provide as taxes. There can be difference between two.

Deferred tax: please see above, link:

Tax not paid for 3/5 years: not normal at all. Yes there can be concession, can be tax planning (but they should get caught in MAT-Minimum Alternate tax).

Buying of shares at advance tax payment dates- I am not sure I have ever followed that. Rather I would buy when there is a gap between business valuation and market price. And my gap is respected by crowd foot print or you can say public ( at least some) is also believing there is a gap. I don’t want to be alone.

2 Likes

Thank you sir

Sir while you started Working how much time did you dedicate to reading about Stock Markets ( Books specifically )… How many Books on an average did you used to read… Did you only read about Books relating to Stock Markets in your initial days… What impact did reading Books have on your initial investing days and the days thereafter… What kind of Books on Stocks did you start reading in your early days…

Hi Friend

Thanks for asking this question. I started working around early 2000 (Year) till Jan 2016. I was not an enthusiast reader then. Though I had a habit of reading newspaper etc before that or till 2002 it was never focused. It was attraction of money that drove me to market. Most of initial investment were made basis annual report and business magazine, although I loved documenting investment then and now also.

Between 2002-2004, my guru played an influential role in shaping reading and research. I was given books like Intelligent Investor, Security Analysis, Phil FIsher etc. Honestly the books may be great, unfortunately I couldn’t apply any of them or at least not to my knowledge.

2004-2007 was a pivotal period where I could capitalise on my investment made earlier (perhaps luck is a significant factor). I continued with mostly stock investing books hapazardly with addition to business strategy books.

2008 was the most of significant year where I survived by a whisker as I withdraw money before end of bull market to buy something else. By chance or luck market crashed, that helped me retain a great deal of bull market profit. That also made me realise how much vulnerable without plan and focused research.

2009 onward I kept increasing my appetite for reading month after month, year after year. It came to a point perhaps which liberated me from certain beliefs including quitting a job for something I always liked to do. The studies are around three subjects only 1. Investing (including both technical and fundamental) 2. Business strategy (including industry insights) 3. Self help (I will include psychology and behavioral finance here).

Before quitting job I was reading average 4/5 hours on working day. Holidays can go up to 8/10 hours easily. Basically if not family/friends, if not office/colleagues then it’s all about books or articles. This may not be good actually, missed those wonderful movies, sports etc. But somehow I am convinced about two things for survival i.e. imbalanced work life, unconventional approach or wisdom.

After job, from morning till evening I spend time on investing books and post evening on self help. Though subject remain same I have started writing extensively here and there, interact more frequently with people and group (but focused group, more closed groups without noise).

Specific answer to your questions

- I haven’t spent much time reading books in initial days. I was more lucky to somehow survived with a favorable market and god gifted guru.

- These days I must be reading at least reading all I can. On an average I purchased around 150 plus books this year (kindle and hard copy). You can take 6 hours minimum, can extend to 12/14 even. No other job to do!

- My life of reading focus on three areas as descried above.

Something bonus from my side:

- It’s better to read one book ten times than ten books once. So among 150 plus purchases this year I would have junked 120 books. I do not regret, they do not align to my requirement. Many times you can not make out from contents or review.

- Book has no value unless you can add one TO DO list. Keep your investment method or task management side by side, every thing that you feel is a treasure add to your list.

- The books with lesser pages are more intense (at least some of them), big volume books are repetitive.

- Getting a good book is like getting a good stock. What is good for you may not be good for others.

- I split requirement to categories first would be essential (investing practice books) and behavioural finance second would be advisory like self help and third will be basics of business strategy and economics.

14 Likes

Please do list the names, which you value very highly. Regards.

To prepare investment documentation: 25% of effort

1.The Investment Checklist by Michael Shearn- without even looking at other books one can pull out key topics wise checklist and start answering. This include bit of screening process too.

2. Five Rules by Pat Dorsey- much has been written about it, not an great advanced book but answers and help first book to put up some working paper.

3. Buffett and Graham beyond by Bruce Greenwald- because I use his franchise valuation for business valuation. Plus a practical approach for competitive advantage working.

4. How to Make Money in stocks by William O Neil- very important layer to understand information beyond financials like acceleration, market direction etc.

For investment execution and maintenance: 50% of effort

- Trade like a Stock Market Wizard by Mark Minervini- all about crowd foot print, growth investing and money/risk management. This has improved my performance substantially.

- Market Wizard by Jack Schwager- not sure how many points I would have added to metrics checklist from this series.

Psychology and behavioral finance

- Beyond fear and greed by Hersch Scheffrin- struggled too much initially but a rare book which touches behavioural finance practice to investing.

- Trading Psychology by Brett Steenbarger- drives you to right mode, NLP etc. A strong reminder always to start the loop from beginning. In short it tells us adversity and need to maintain the tempo when it comes to effort.

Note- this is what my current investment philosophy supports because I prepare a investment document as per fundamental investing but add catalyst and technical (more crowd foot print) for buying and maintaining.

10 Likes