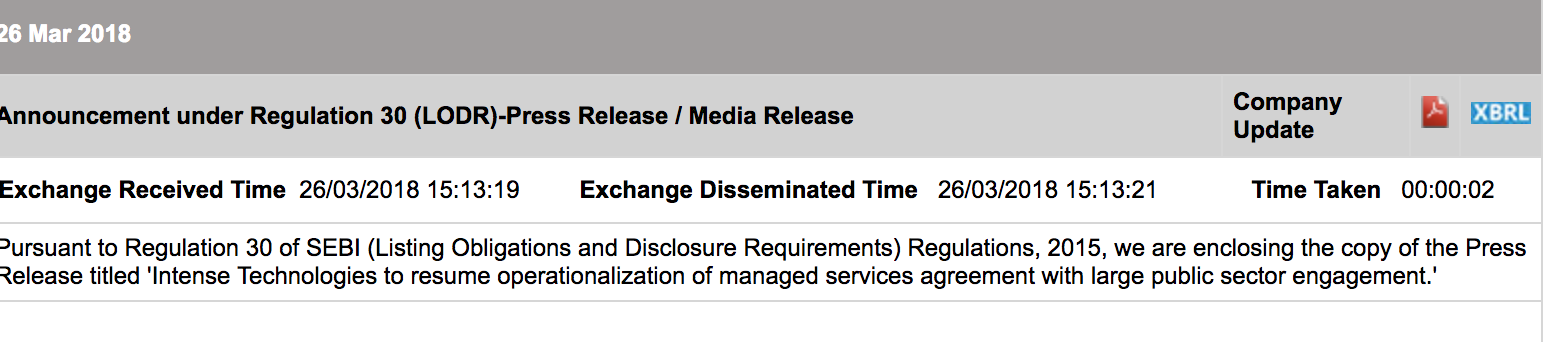

Finally the BSNL impasse seems to be at an end. The company announced this on BSE last week.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=351c9679-49d7-4632-ae50-026b754a8a2b

Finally the BSNL impasse seems to be at an end. The company announced this on BSE last week.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=351c9679-49d7-4632-ae50-026b754a8a2b

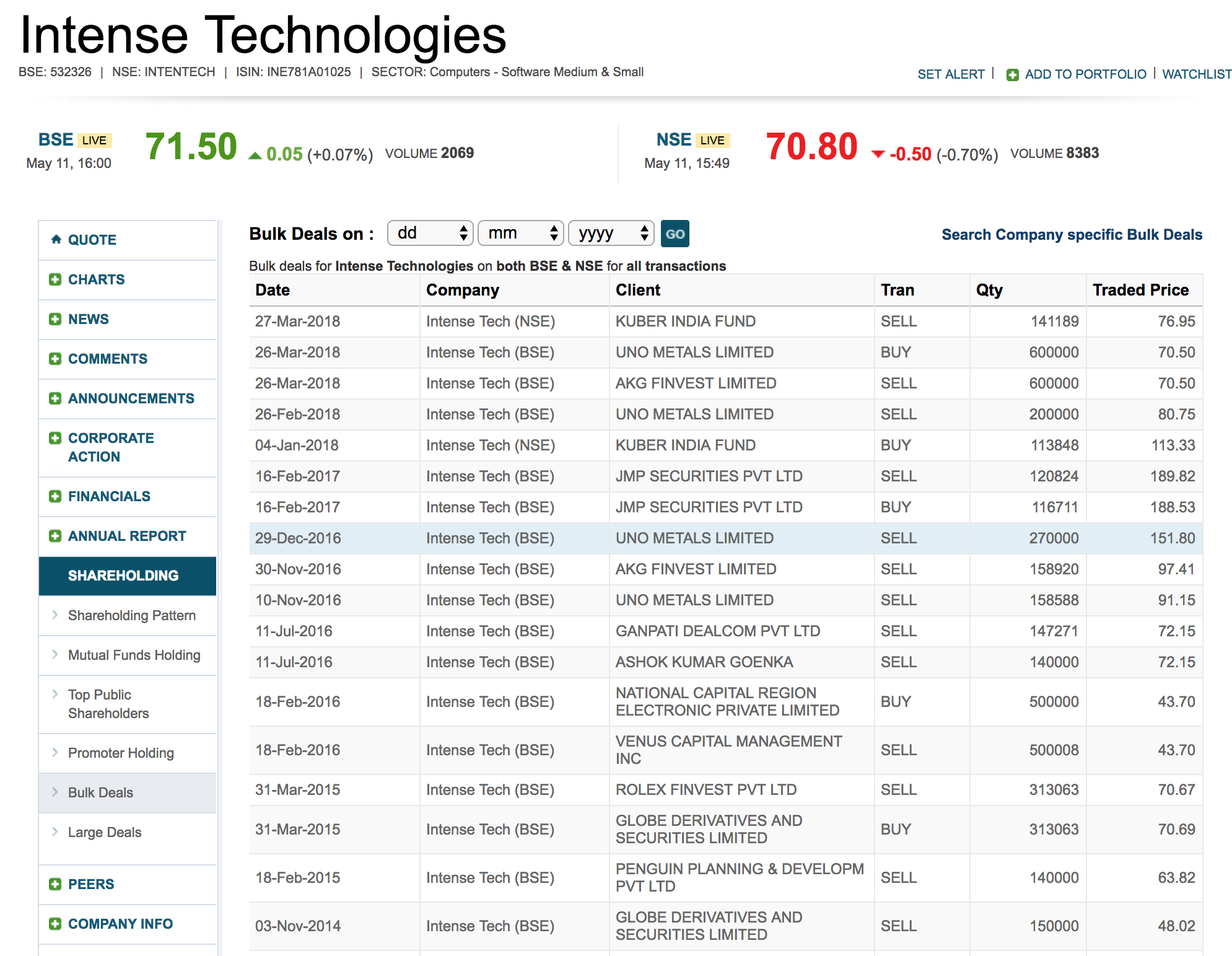

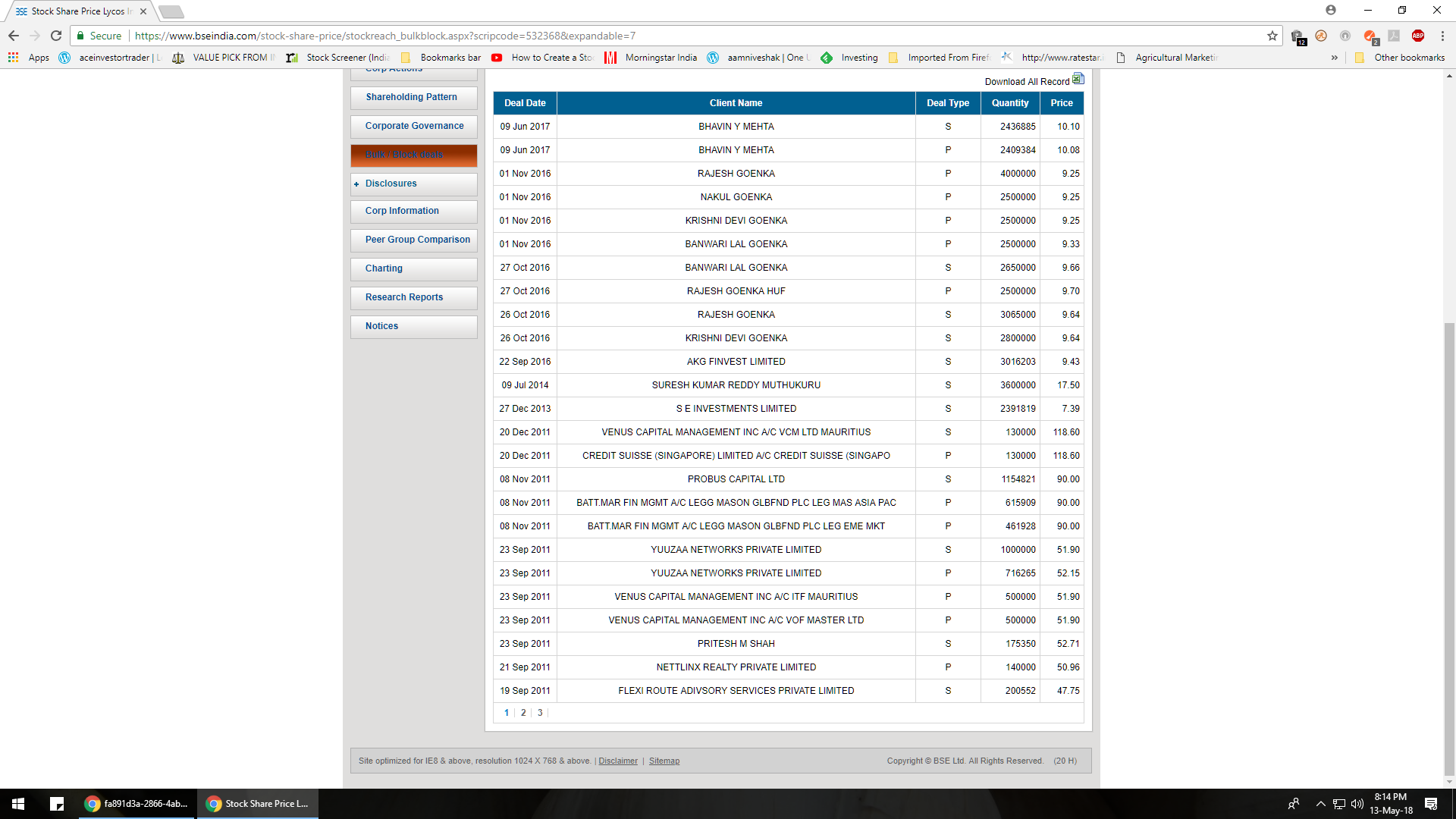

Here are some observations on bulk deals in Intense Technologies:

On March 26th, there was a bulk deal where AKG FINVEST LIMITED sold 6 lakh shares and UNO METALS LIMITED bought 6 lakh shares. See screenshot below

There is more than what meets the eye in this bulk transaction.

a) Firstly the volumes are way higher (atleast 7-8 times higher) than daily volumes. But here is where it gets interesting.

b) This transaction occurred on the same day as when the company announced that BSNL deal is resuming. The BSNL announcement hit the Bombay Stock Exchange website at around 3:13 pm. But the bulk deal occurred b/w 12pm-1pm as shown in the screenshots below taken from my trading platform. The bulk transaction occurred around 3 hours before a material announcement was made, material because BSNL can increase revenues by 50%.

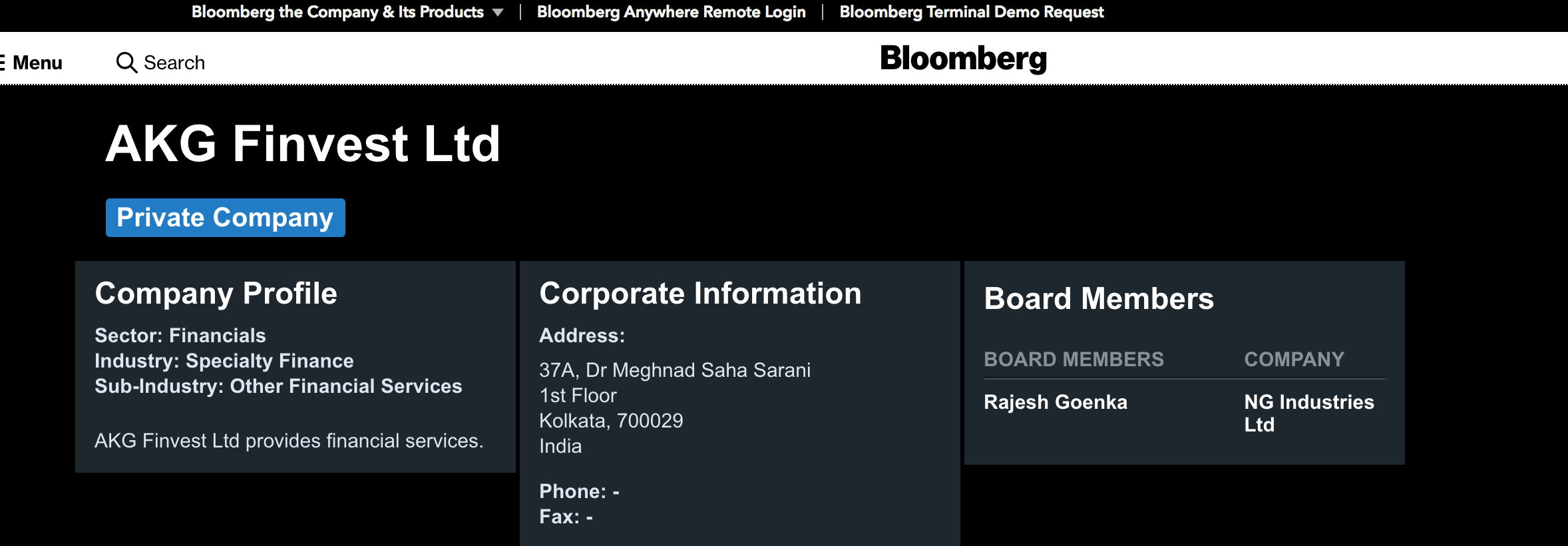

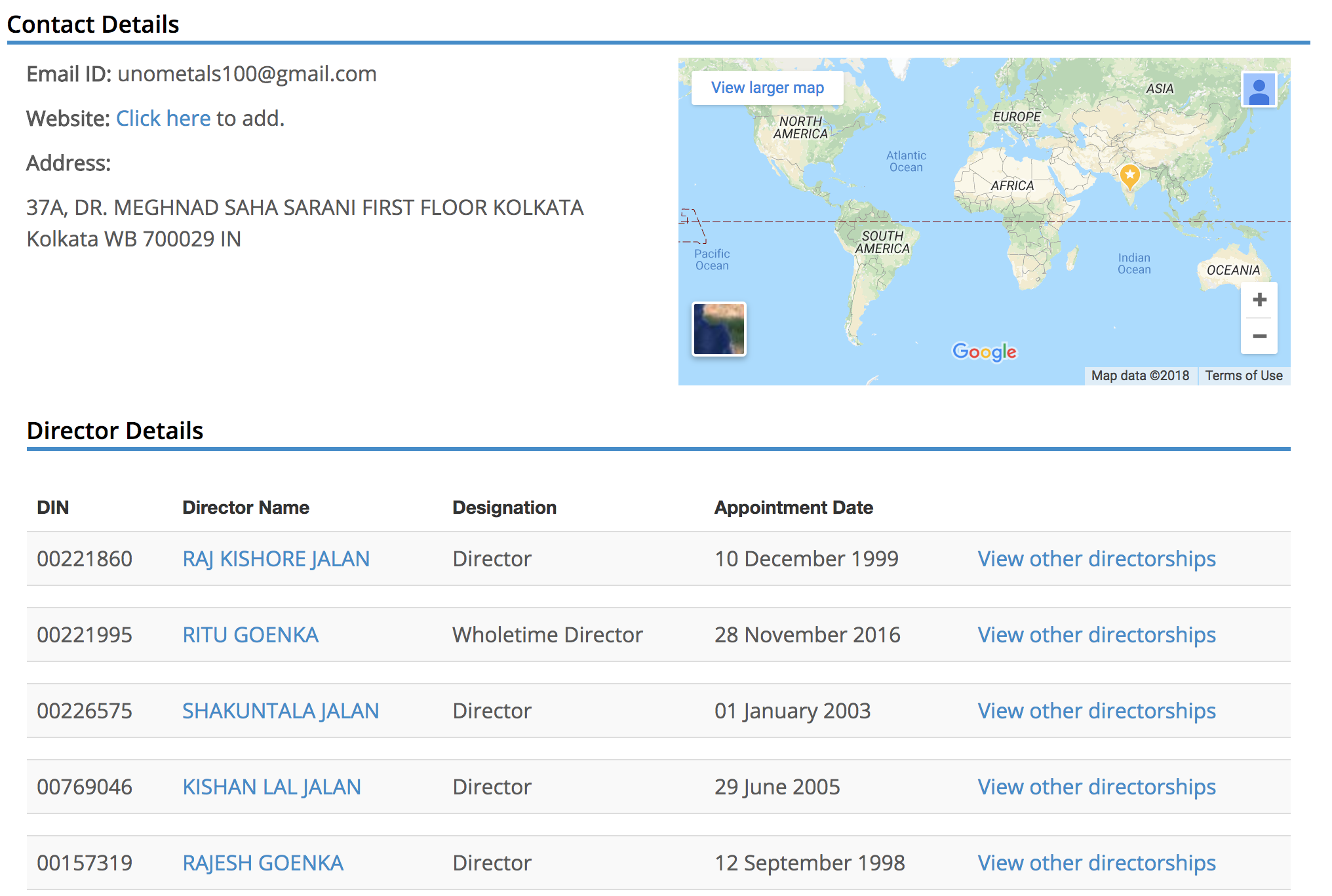

c)I was curious to understand who these entities are. On searching the web, I found out that they have the same mailing address:

37A, DR. MEGHNAD SAHA SARANI FIRST FLOOR KOLKATA Kolkata WB 700029 IN

Not just that, they have a common set of board members: On

https://www.bloomberg.com/profiles/companies/1246900D:IN-akg-finvest-ltd

On

I wonder what economic value this bulk transaction generated.

This UNO and AKG finvest works in hand to hand to pump the stock then play their game. Same type of misdeed is done in Lycos Internet.

I am afraid and cant decide what to do with this stock which has become a burden to our portfolio.

Discl: Holding

@ravish: Do not be afraid. Sub-par investment decisions do happen and investing is a life-long learning experience. These bitter experiences make one humble and should be taken as an opportunity to learn as much as possible from them, and one should work harder to get the portfolio back on track.

My opinion is that I think this stock is bottomed out, even assuming that BSNL deal does not go through.

Even if BSNL standoff continues, a) the company is close to breakeven (I expect a max of 4-5 crores consolidated loss without BSNL contract for FY 2018) and b) The Market cap is approximately 3 times sales, which is not too high either.

I think the downside is limited and hence have decided not to sell for now.

(The above assumptions made on calculations are taken from the conference call notes)

Welcome back INTENSE TECH super Standalone result

Attended the con all of management . In a nutshell . The management is supremely confident having seen through the time , results of Q4 FY2018 are harbinger of the results of next years , having sorted out the crisis, the management will now concentrate securing orders from abroad which will be more profitable . I could see that the company is on a growth path.

Just see the chart. No one spoke about the downside, only the Income Tax, Jio, BSNL orders when it was “only buyers on BSE” for weeks on end. Clearly a pump up to price of 220. It is now trading at 30% of the price. Read this thread to see instances of price manipulation. Hyderabadi promoters (although you had mentioned it as a risk in your OP - this is not aimed at you).

Questions on accounting standards.

If its not a dump, then god knows what is.

I agree this is a story which didn’t play out as envisaged. No one has lost more in this counter than me, hence the accusation by Ashwini specially pointing to me is clearly not in good taste.

All posts are created with a view to enable healthy discussion about a stock. In all the threads initiated by me, I hold enough shares to be above the disclosure threshold. I exited one, and updated that particular thread.

You are free to label me as a bad stock picker. But nothing else.

This stock has been pumped and dumped. There is no debate here. It is not often that a stock loses 80% of its value from the peak. (250 to 50).

A stock is said to have been pumped and dumped when:

The dumping in this case has occurred for an extended period because the company did not disclose important information on time. (like BSNL standoff, non-existent BSNL revenues/non-existent pipeline of new revenues etc.) The delay in disclosures ranged from 3 months to more than a year, which led to retailers to buy the stock on a continuous basis. This makes the company/promoters untrustworthy.

While we are facing the brunt of this pump and dump process, we (including myself) should hold ourselves responsible for this sub-standard investment. If we are not accountable for our money, then who should be?

My opinion here is that the stock price may go up and we might get a significantly better price to sell the shares, as the revenues booked excluding BSNL do exist, and I still think it is difficult to fake the existence of a software product.

Here are some really interesting observations and analysis on Intense Technologies shareholding patterns. Even if you have not followed this company, I will provide enough details. This analysis will raise some key questions and there is a lot to be learnt here as shareholders in general.

I also realize that it may be difficult to understand my previous posts, so again, a lot many details below, where things will be clear:

There are 6 Parts to this analysis. Do read each of them carefully.

PART 1

First, let’s understand the sequence of events as they unfolded:

• The company generated 42 crores in revenues in FY 2016 through sales and maintenance of software

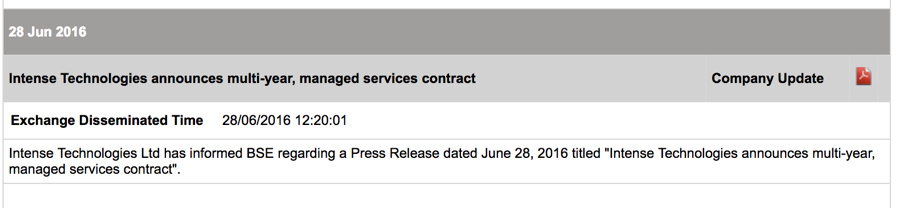

• On June 28th, 2016, the company announced a contract with BSNL worth 25 crores every year. Some estimates say this could be 40 crores. Screenshot from BSE

• Due to BSNL, revenues are expected to increase 65%-100%. From negative EPS, company is expected to generate EPS of 8-10

• In July-September 2016 quarter, company records 25% of its revenues from BSNL and posts best-ever EPS. Results announced on 10th November. Company does not reveal anything about BSNL contribution

• In Oct-Dec 2016 quarter, company records 50% of its revenues from BSNL and posts best ever sales. Company does not reveal anything about BSNL contribution

• Share price starts going up and hits a peak of 248 on Feb 9th, 2017

• However, on Feb 7th, 2017, Supreme Court says that a mobile number needs to be linked with the corresponding Aadhar number. Here is the link:

• On June 1st, 2017, there was a conference call with investors where

o The promoter says that because of the above Supreme court ruling, BSNL contract has come to a standstill. No BSE notice, no early warning, just a few statements that the 150-crore contract could be on hold.

o Promoter does not say that a substantial 21% of FY 2017 revenues needs to be written off.

o Share price is already down 60% to ~ 100 BUT WAIT:

• On March 9th, 2017, there was a conference call with investors where

o The promoter insists that BSNL contract is on track (note: Supreme court ruling came out a month earlier) and

o No disclosure about BSNL revenues contributing to a massive 50% of Q3 FY 17 revenues

o Share price is already down 40% to 150 on March 9th

If you have read and agree with what has occurred, only then continue ahead. If not please go back and read this once more and ask any questions, so that you can understand what is written below

PART 2

Do read Part 1 before reading ahead

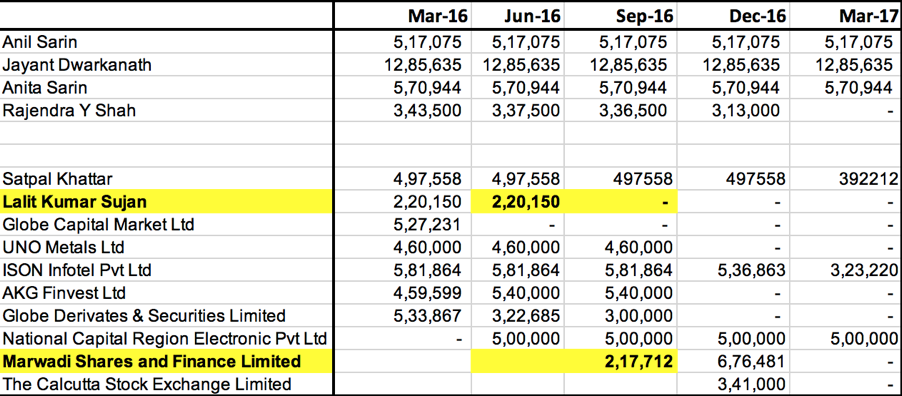

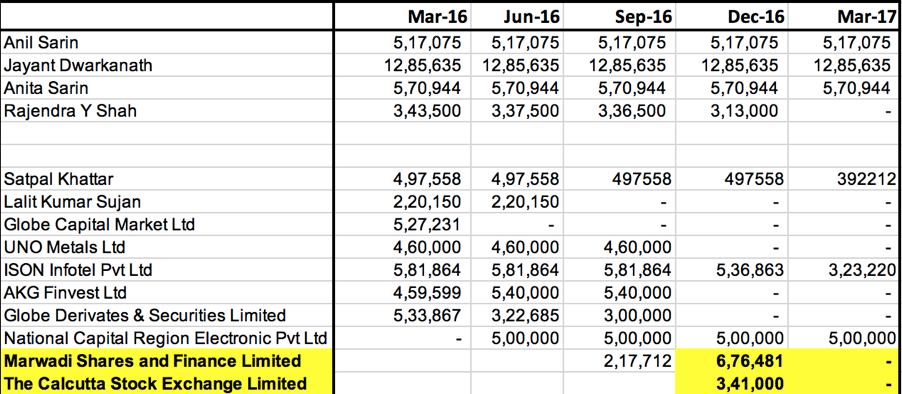

Let’s look at shareholding patterns:

Look at shareholding from June 2016 to March 2017, to see who has entered and exited. This is where it gets interesting:

While he exits, Marwadi Shares and Finance enters with approximately the same number of shares. These are the changes between June and Sep 2016.

The company has said revenues will be up ~65% (and therefore profits will increase exponentially), and yet the exit by the insider. The BSNL contract came to a standstill only on Feb 7th, 2017 as per the court ruling according to the company; Company is recording BSNL revenues starting July; Is it not strange that the promoter’s relative exits between July 2016-Sep 2016 immediately after the 150 crore BSNL contract is announced?

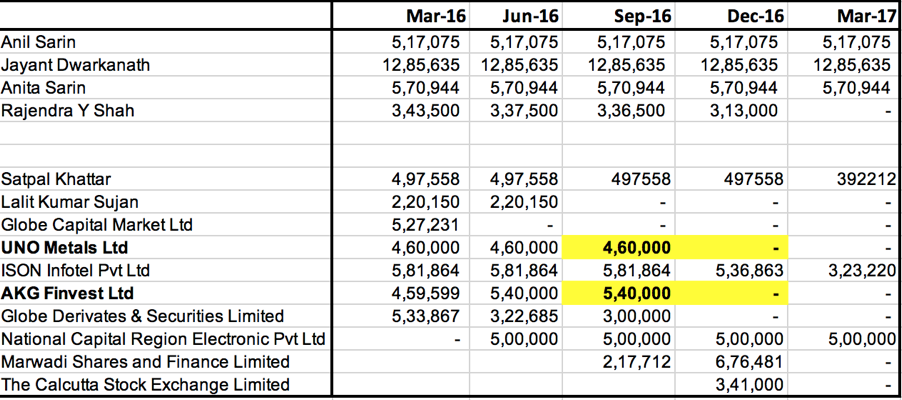

Ashok Goenka is a Director in AKG Finvest and Ganpati Dealcom. I have already mentioned earlier that AKG Finvest and UNO Metals have a common set of directors, same mailing address in Kolkata and more importantly are insiders (they know insider information about the company before announcements are made to retailers/exchange).

Is it not strange that insiders are exiting the stock as soon as the BSNL contract announcement is made?

Again, the same question: Why are insiders so keen to dump shares when BSNL has contributed to 50% revenues between Oct 2016-Dec 2016? The BSNL contract is progressing extremely well, as per the company; there are no signs of standoff, yet insiders are heading towards the exit?

Further, the 21 country Vodafone contract was announced and yet insiders are leaving en-masse?

I am going by what BSE discloses as a policy: that is, only shareholding above 1% and bulk deals above 0.5%. The Goenkas have 4 entities registered under their name and the same mailing address, but there could be many more as there are 300 plus corporate bodies who hold Intense shares. They have engaged in circular trading to prop up trading and delivery volume as explained before in my post on May 10.

PART 3

Let’s summarize Part 1 & 2: Insiders have sold a massive 15.1 lakh shares between July 2016- Dec 2016, despite the company announcing the 150 crore 6-year BSNL contract, that is game changing and where according to the company a) There is absolutely NO BSNL STANDOFF and b) Revenues are being recorded in “good-faith” because the company believes it will get paid.

Why do you think this is the case?

Continuing: Who are insiders selling their shares too? Some analysis below:

Good chunk of shares is sold to retailers

As per bulk deals, on Dec 29th, 2016, Uno Metals Limited sells 2.7 lakh shares to Marwadi Shares and Finance at Rs. 150 (one operator to another)

Some shares are bought by Calcutta Stock Exchange (CSE). Firstly, CSE is not a PE fund or a Venture Capital/Mutual Fund that invests in companies. It mostly comprises of shell companies and many times they organize “synchronized transactions” (or circular trading to control price movements) as per the article by Mint:

So, a corporate body/broker has purchased shares under CSE’s name. It is a coincidence that The Goenkas, AKG Finvest, UNO Metals, Ganpati Dealcom are all based in Kolkata (see my earlier post on May 10th) and these entities trade amongst each other.

The government is trying to close CSE but the matter is stuck in court. Again, CSE does not own shares as an entity, it is only a conduit to control share price movement, as per available online sources.

Now look at Dec 2016 share holding pattern: Marwadi Shares and Finance and CSE own 6.8 lakh and 3.4 lakh shares.

Now, let’s look at share price between Jan 1, 2017 and March 31, 2017. It went up from ~ 150 to ~250 and then back to ~150 by when both the entities above completely dump 10.2 lakh shares together on retailers. This is at a time when the company is insisting BSNL contract is on track.

PART 4

Do read Parts 1,2,3 before continuing ahead.

To summarize: In total, more than 20 lakh shares have been dumped on retailers by March 31st, 2017 (there are only small retailers and a few HNI’s in this stock as no mutual fund has taken a stake here).

When the company is recording revenues from BSNL and is insisting that the contract is on track and there is no standoff, why have 20 lakh shares been dumped by insiders and corporate bodies on retailers?

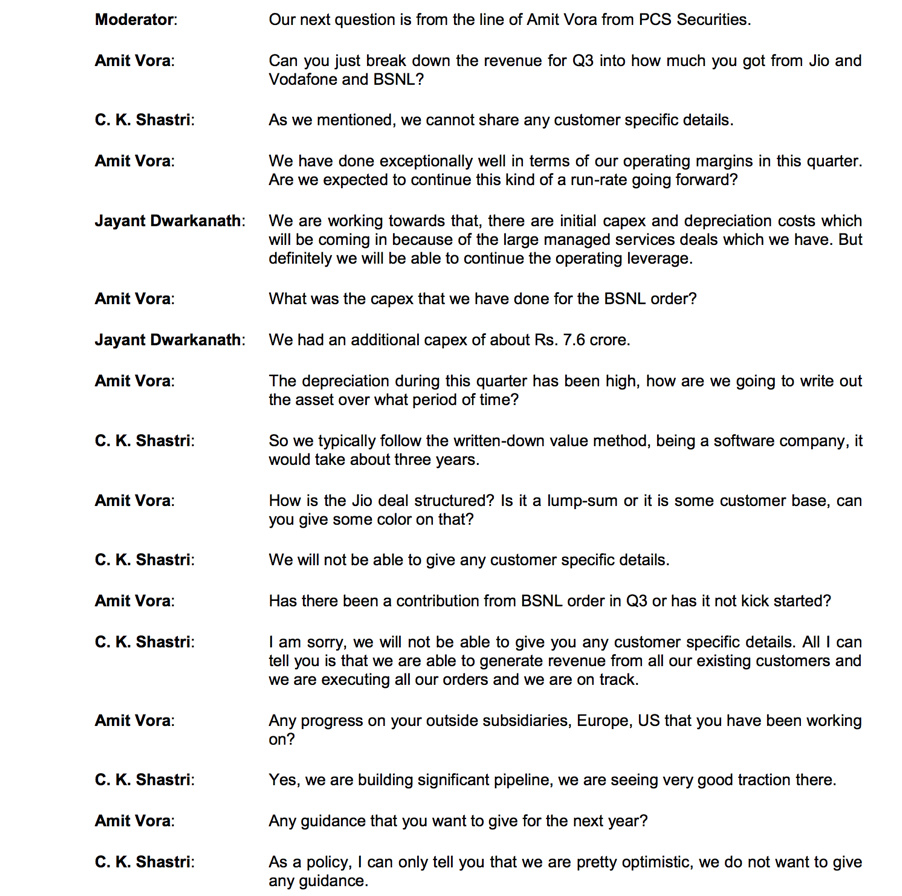

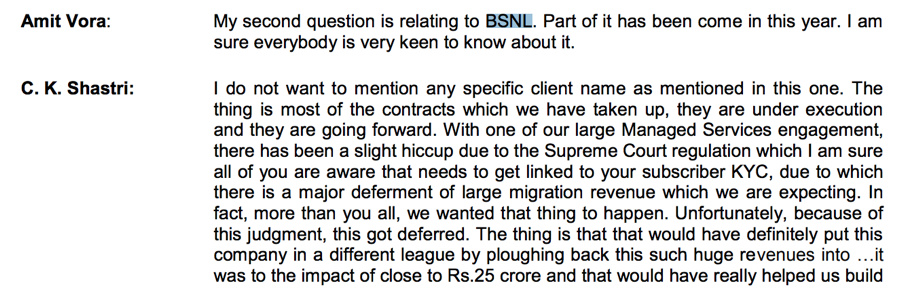

Now let’s understand what the promoters of this company told shareholders/exchange during this time:

On March 9th, 2017 there was a conference call with shareholders. The promoter insists that BSNL contract is on track. He does not reveal that

Here is the conference call excerpt:

Now your argument could be that the promoter genuinely does not know about the three points above and absolutely believes that BSNL contract is on track; for which, the counter-arguments are, How could he not know when:

Since the promoter does not reveal facts related to BSNL and further insists that the pipeline of revenues is strong on March 9th, 2017, retailers continue to buy the shares all the way from 250 down to 100 on June 1st, when he finally discloses that BSNL contract is on hold, before which, Calcutta Stock Exchange (a corporate entity essentially) and Marwadi Shares and Finance completely offload 10.5 lakh shares by March 31st.

Now, let’s assume that the promoter discloses BSNL related facts as-is on March 9th during the conference call. What would have happened? The share price would have plummeted to 60 over the next few days. Would anyone buy shares starting March 2017, if they knew that the entire BSNL contract is at risk and most revenues from Q2 and Q3 needs to be written off?

Let’s give the benefit of doubt to the promoter and that he absolutely believed that BSNL contract was on track on March 9th.

But the company does not even send a notice to BSE stating that the 150 crore BSNL contract is on hold. They can send a notice to BSE stating that they received an order from BSNL that can increase revenues by 65%, but do not even inform shareholders till June 1st, when the promoter makes only passing remarks that the entire contract is at risk. See conf-call excerpt below:

On June 1st, 2017 the promoter still does not disclose that 21% of FY 17 revenues are from BSNL and is at risk to be written off. This is disclosed quietly only in Feb 2018, more than 18 months after revenues have been recorded, that they need to be written off.

PART 5

Based on analyses Parts 1-4 described at-length above, I have come to the following two conclusions:

The stock has been pumped due to

a. Recording “non-existent revenues” and announcing “non-existent contracts” (non-existent for 2 years at least, may exist in the future) and

b. Dumped by insiders on retailers (no fund is invested here)

c. And the 80% drop in price from the peak is not an accident.

The promoters are not trust-worthy

Apart from the two conclusions above, there is a third conclusion that I have come to which is

I know the three conclusions are contradictory but that is what the data and my analysis is telling me. The stock having lost 80% of its value from the peak is something that has occurred over the last 2 years. Again, it is not an accident. There are strong signs of it being orchestrated. This does not necessarily mean it will go down further, though. The stock is at reasonable valuations considering price and revenues that are largely not at risk of being written off. The revenues are earned from AMC’s mostly, pay for the companies’ expenses to much an extent, and are earned from large corporations over many years that have demonstrated a history of paying up. The stock might have bottomed out, but one never knows.

With disappointed shareholders in tow, and a poorly executed pump and dump to boot with, the stock will turn around, is my bet.

Nice work done Srihari. I am one of the affected parties here as well.

I remember once anirudh sethi recomending this stock. He is a number one manipulator. I feel its safe to not to touch a stock if he has put his hands on

Solid analysis. A painful read for me as an investor and all I could let out was a whimper. Good work @Shrihari

But I have a question. Don’t large dealings happen in a stock when “real” good news is announced? Is the promoter’s family member selling “early on” (not at peak) the biggest reveal. Basically I also want to understand if such a pattern can be consistently spotted early.

@Vij: If we were to go back in time and do things differently, in my opinion, we should look at the following:

o How much “skin-in-the-game” do promoters have? In other words, do they own a large chunk of shares?

o Who has the company struck a large contract with? A PSU should raise concerns as situations

like these could arise.

o Do reputed funds own shares? Funds do good amount of due diligence which even HNI’s cannot.

o When large deals are announced, promoter’s relatives exiting should raise questions. In this case, there is an exit. While price is not at the peak, we do not know anything else (who has sold to whom etc., we are left at making guesses here, or we should be looking at other data points to understand promoter-quality)

o When large bulk transactions occur, question why and when have they occurred.

o Look at bulk deals. AKG Finvest and UNO Metals have a not-so-good history in Lycos as per other forum members’ learnings. Lycos is another Hyderabad based software company with a chequered reputation either

o Look at shareholding patterns. Can an exchange own shares? What history and reputation does the exchange have? From my analysis, NSE is most trustworthy. Who has entered and exited according to shareholding patterns?

o If one understands technicals, one would have exited between 150-240 as the stock is nosediving. If one is a strong technical chartist, one can make a logical guess that the shares are being pumped and dumped, without even reading about the fundamentals, is what I think

PART 6

Please read Parts 1-5 to understand what is written below. It might be difficult to follow otherwise.

This stock has gone through a second pump and dump at a smaller scale within the larger one. This occurred as early as a few months back.

Here is analysis to explain the point of contention:

Like mentioned above, the stock hit a peak price of 248 on Feb 9th, 2017. This was due to recording non-existent revenues from BSNL in Q2 and Q3 of FY 2017, as explained earlier.

After a large number of shares were dumped and recording “made-up” revenues from BSNL came to a halt, the share price started making daily lows and touched 80 in September.

The company posted dismal revenues and EPS in the Apr-Jun quarter (lowest revenues and EPS in a very long time) and announced it on September 11th. Retailers panicked and started selling shares that were dumped on them at a much higher price.

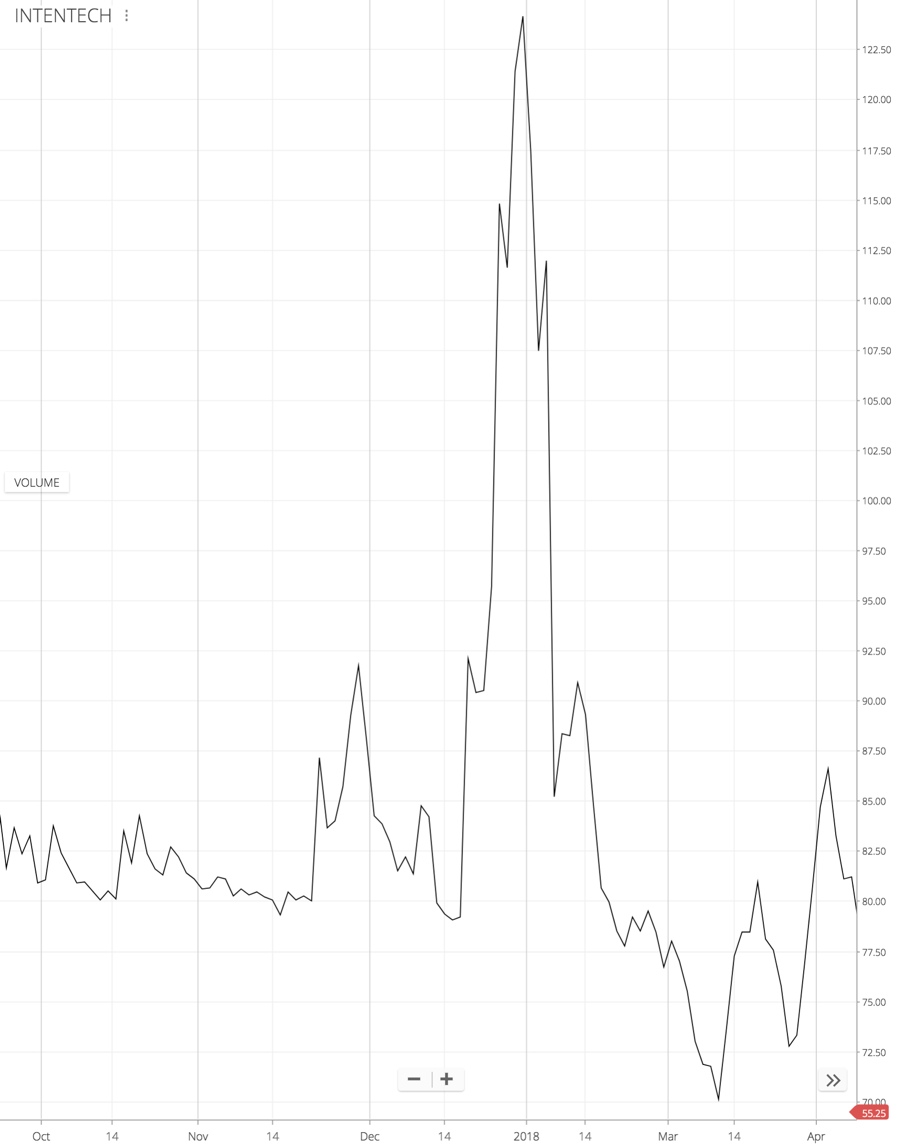

Now look at share price between Oct 2017 to Mar 2018. Here are the key observations

Stock price is in a tight range between 80 to 85 for most, if not all of October and November (most of the time, it is between 80 and 82.5).

What this means is that the shares are being accumulated. Retailers are offloading shares and some entities are buying

The share price shoots up to 125 from 80 in a matter of days and comes down equally fast to 70 by the end of March, for no fundamental reasons whatsoever.

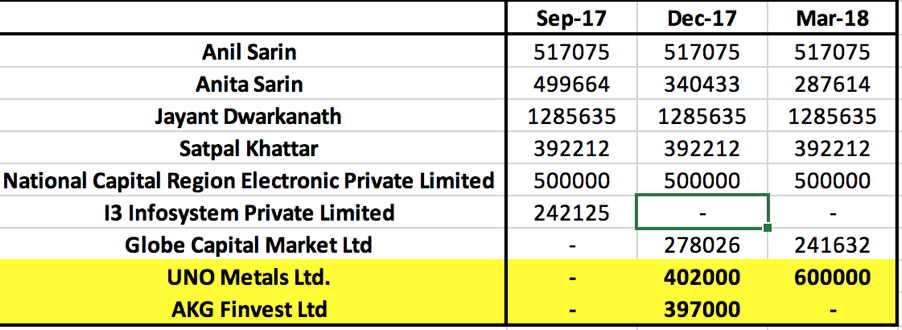

This is the second recurrence. To understand this better, let’s look at shareholding patterns between Sep 2017, Dec 2017 and Mar 2018:

As mentioned earlier, the insiders, AKG Finvest and UNO Metals (corporate entities with the same mailing address and same board of directors as explained earlier) dumped their shares completely between Oct-Dec 2016 on retailers, as the frenzied buying progressed due to the BSNL contract announcement. They have no shareholding as of Sep 2017.

But they start accumulating shares at 80-85 between Oct 2017-Dec 2017, as retailers keep selling their shares, as most of them start suspecting that something is amiss. They accumulate around 800000 shares

They again dump shares at a ~ 50% increased price. This time they are able to dump only ~2 lakh shares as retailers are perhaps not interested anymore. The share price nose-dives back to ~70 zones in no time.

Uno Metals holds 6 lakh shares in Intense as per the latest shareholding patterns. If you are an Intense Tech. shareholder, do observe these corporate bodies’ shareholding patterns.

PART 7 : Complete Explanation Using a Simple Analogy

Not all Valuepickr community members own Intense Technologies shares. My analysis has six parts and may be tedious to read and understand, especially if you do not follow this company.

Here is a complete explanation using a simple analogy:

Imagine a scenario where you own shares of a manufacturing company.

• The manufacturing company posts 42 crores in revenues in FY 2016

• On June 28th, 2016, the company sends a notice to BSE that a large new factory has been constructed that can increase revenues by 65% (some estimates say 100%) and therefore profits are expected to increase exponentially

• Between July-Sep 2016, company records 25% of revenues from the new factory and posts largest-ever EPS; Does not disclose this fact until much later

• Between Oct – Dec 2016, company records 50% of revenues from the new factory and posts largest-ever sales; Does not disclose this fact until much later

• Between July-Dec 2016, there is frenzied purchases of shares by retailers while insiders keep dumping shares on them.

• On Feb 7th, 2017, there was a fire in the new factory and production came to a halt; company does not say anything

• On Feb 9th, 2017, stock price hits a record high of 248

• Insiders continue dumping shares and retailers keep buying

• On March 9th, 2017, there is a conference call.

• Share price goes to 185 in the next week (by March 15th, 2017) as retailers still do not know that there was a fire in the new factory

• Share price starts hitting weekly lows and touches 100 by the end of May 2017

• There is a conference call on June 1st, 2017.

• Company posts the lowest ever sales and earnings between Apr – Jun 2017 in a very long time and reveals it on Sep 11, 2017. Share price drops from 100 on Sept 10th to 80 on Sep11th and recovers

• There is a conference call on Sep 22nd, 2017

• A few weeks later, promoter pledges shares on Nov 30th, 2017

• Share price is stuck at 80 for 2 months and for no reason goes up to 125 on Dec 29th, 2017 and back to 70 a few weeks later (Insiders dump and retailers buy)

• On 14th Feb 2018, company announces earnings and sends a notice to BSE saying “We had a fire on Feb 7th, 2017, in the new factory, as you already know. We, however, recorded revenues in Q2 and Q3 2016 from the new factory and it totals to 25% and 50% of these quarters’ revenues, and this needs to be written off, unfortunately”.

• Based on data, there is a strong case that there was no fire in the factory on Feb 7th, 2017, because there was no factory in the first place

• In March 2018, company sends a notice to BSE stating that the new factory is now up and running

• It is July 2018 now (share price has touched an annual low price of 50), and we shareholders are waiting patiently for genuine revenues to be recorded from the new factory

Replace the

and you get what has occurred here.