Ain’t an overnight story…gotta give this time. Point 8 says gst resulted in order shift. Not sure how much was the impact, though.

Appreciate if any one who could attend today’s concall can share notes.

Details of INTENSE concall

- have a pipeline of new clients of around 32m $ (not including farming of existing logos)

- pipeline to order conversion is around 40%.

- New strategic investor discussions are initiated

- strategic investor needed to give uniserve the global reach it deserves

- Q2 will be much better than Q1

- New announcement of a new deal win in the US (Telecom co with operations in 23 countries) to be made soon

- products are finding application beyond traditional domains of bfsi and telecom

- system integrators actively seeking co out for its unique products

- bsnl to start latest by q4

- gst related issues resolved

7 Likes

Just incase someone is interested to hear complete call:

https://www.researchbytes.com/Intense-Technologies-Limited-I0482.htm

1 Like

Maybe some issue with Java/flash etc… Try different browsers. I tested it on firefox in win 7 and Mac

Ok. Thanks. will try again

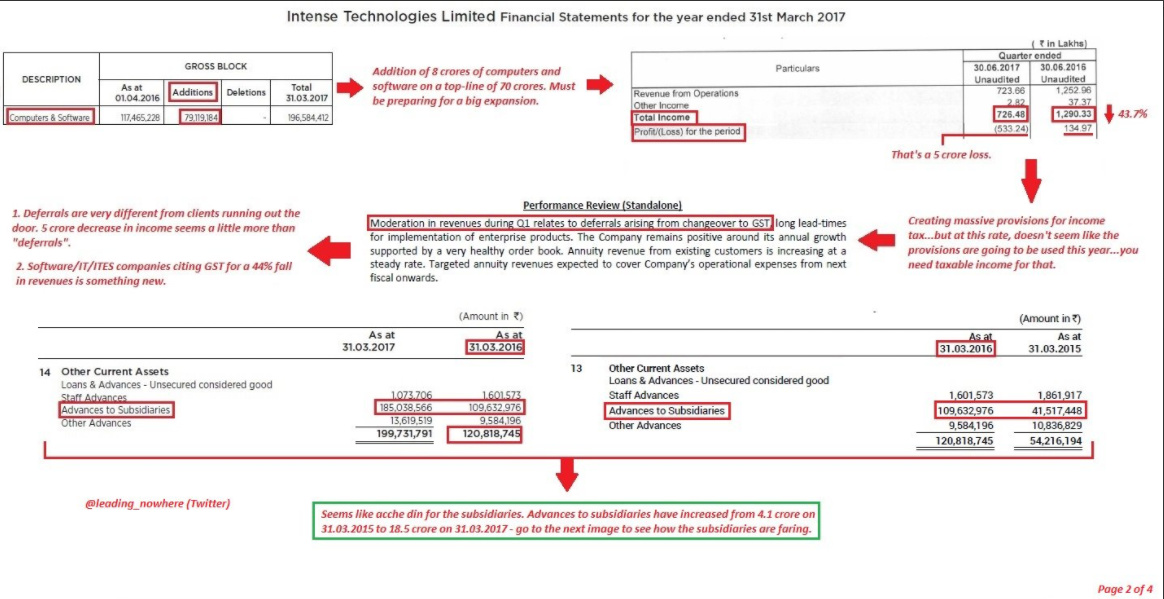

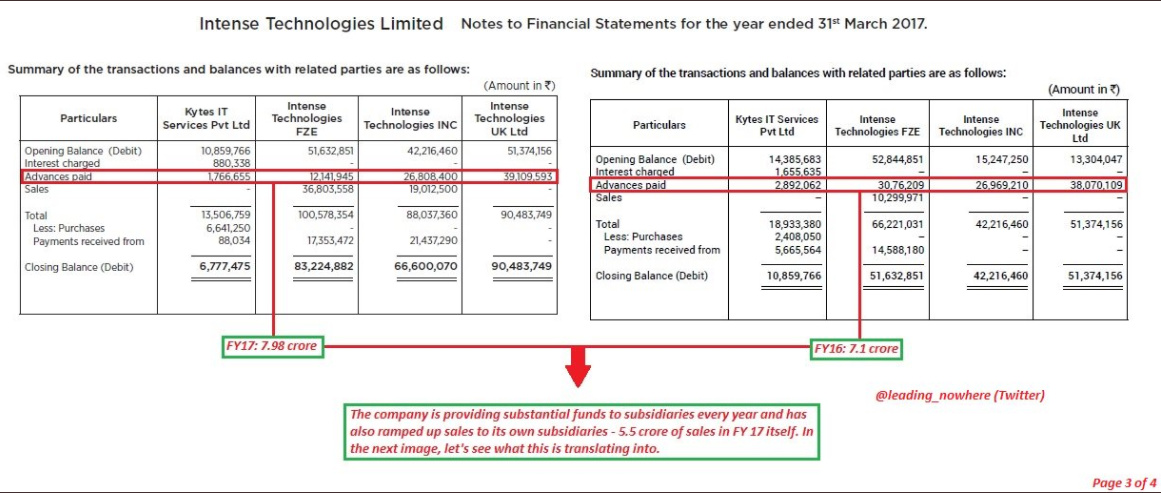

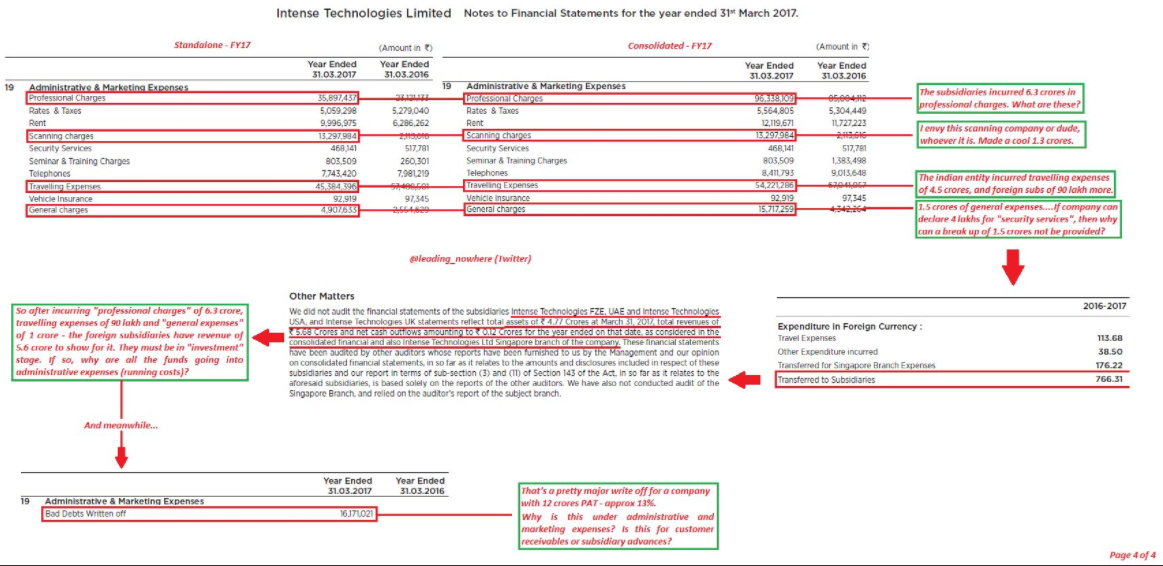

Thanks @rkdeelip for putting it here. I saw this analysis on twitter. The whole discussion chain is a learning experience. The author has found few good points however he should have done some more work to get answer.

- The 8cr increase in computers is due to server buying for BSNL. In conf-call management gave this information. There was huge cry over depreciation. This H/W buying was a factor. As per BSNL contract they need to buy servers and maintain software. The BSNL contract has created uncertainty which management gave guidance to overcome by end of this year.

- You need to pay tax upfront (that goes out of cash flow) and put in provision. Someone pointed it on twitter.

- Revenue decline due to GST is head first time. But when you have Indian customers as major one contributing to revenue this can happen. I don’t think management will lie in conf call on this. One reason could be customer not ready to recognize the bill due to delay in GST roll over.

- Advance to subsidiaries is high. This is natural. Subsidiaries are having only Sales & Marketing force with some administrative staff. As per AR CEO salary has doubled. He works from USA. His salary has to be given advance from parent company. Generally parent company which gets business from subsidiaries effort of S&M will have this structure. Considering the sales for cost, I don’t think it is high. It is 10 - 12% of revenue for S&M. Which is needed for them.

- Scanning charges are up significantly. I guess it may be due to JIO customer onboarding.

- My take on write off was different. I have mentioned it in earlier post. This write-off has come after three years of growth. Sometimes management goes wrong in customer assessment. 1.6Cr should be taken as% of cumulative sales in last three years.

Disclosure:- I have not bought and sold any shares since last three months. Hold in PF.

12 Likes

Intense is very slow to release their quarterly numbers this year. Could this indicate things not very good so far? Results going to be on Dec 12th as per BSE notification. Also C.K. Shastri created a pledge with 1.7% share holding on 22/11/17 with reasons of working capital needs. (Pledge Notification) This could indicate that BSNL revenue flowing or any good revenue coming in current quarter as well. Views @thestocklady, @hrishikesh ?

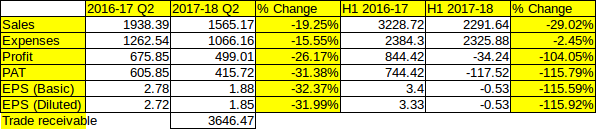

Q2 2017-18 results announced. The Quarter back on green in profits, mainly due to lower expenses. But compared to year ago quarter, sales and Profits are a dampener.

Trade receivable is 3646.47 and all figures in Lakhs.

Detailed Results can be viewed here - http://www.bseindia.com/xml-data/corpfiling/AttachLive/eb58dcbf-aaf2-40c1-8b8d-815703833be6.pdf

Conference call tomorrow at 12 Noon.

Disc: Invested at higher levels and no transaction in last 2 months

1 Like

What is the outcome of concall ? Any one who has attended PL share.

Confcall transcript

http://www.bseindia.com/xml-data/corpfiling/AttachLive/396dfd48-28f7-4b23-81a5-ffef52c38175.pdf

Thank you Zoro.

Here is my summary notes (Validate yourself)

Overview:

- We are going with lot of system integrators and partners than direct selling

- We see traction is coming in the international market than what we see in the domestic market

- World is moving away from the services side to enterprise, the product side, and we believe we are well positioned to seize the opportunity which is coming up.

- Uniserve Nxt: a lot of robotic process automachine, the BPM, low base platform which it can configure and we can deploy any large scale implementation using micro-services and a whole lot of things. In robotics, focusing on automated testing, financial re-conciliation, bot based chat systems. In these domains we would want to be leaders. We may look at Mobile IoT related solutions for the automobile industry, through a customer.

BSNL Deal: We offered linking the Aadhar part of the data in Phase 1 of the project in a free of cost and is evaluated by customer.

Phase one is customer onboarding and data migration and scanning.

Phase 2 got go-ahead. They comprises of bill presentment, interactive bill

delivery, communication, campaign management, coupons (loyalty). This phase is

revenue sharing model and we see the bare minimum revenues from that is slated

to be around Rs. 40 crore to Rs. 50 crore in over about next five years.

Part of Phase 2 is expected to be live by January. So, we are very confident that we will bounce back.

Revenue:

- Most of our revenue comes from digital engagement. then we have B2B analytics.

- Cross selling and up-selling is continuing with the existing accounts.

- This is first FY that we actually have good numbers with system integrators/alliance partnership.

We hope to close some new discussions this FY itself. - Revenue Visibility : One of our managed services contracts are close to Rs. 150 crore (21 country deal).

min revenue of almost Rs. 6 crore to Rs. 7 crore per annum from Govt customer deal (BSNL) - Predictable part Rs. 30 crore to Rs. 40 crore is from our existing customers.

- Most of receivables from Sept collected already.Our normal receivables cycle is about120 to 150 days and we are trying to reduce that.

- Some contentious issues remains with two of our accounts on the receivables on the balance what has not been collected.

- 2017 - revenue breakup- 60% from from India and rest from International.

- Subsidiary revenues - Europian subsidiary only expenses and revenue comes to parent. America , Middle East and Africa started seeing revenues.

- Revenue Target - In 2022 about $100 million

- Revenue realization in terms of license fees and other things is higher in Europe and US (compared to India).

Customer Accounts:

- We have about four large strategic accounts, and large accounts we have close to ten plus accounts.

- In india, 10 to 15 customers and we are leaders in Telecom and Insurance. One large bank is our customer (HDFC Bank).

- Currently tie up with Oracle, IBM and AWS in cloud.

- We are very conscious about our reputation so we are taking careful steps especially for first time engagements.

- Most competition from US

- Selling cycle - 12 to 18 months. Involves, discussion process,realization to buy, the pilot, BOC, then the contractual agreement. In discussion with few at contractual stage. So long gestation period and tough to predict Q on Q.

- A large telecom player in the Central America signed for the quarter Q3.

Promoter Holding:

Pledge:we have pledged our shares as we have aken some bank limit for things like bank guarantees.

Holding: Between the directors, promotes and employees, close to 35% plus holding.

Personal Perspective:

I do see the management as sincere and after having some exposure to enterprise product space, I tent to agree most of their arguments on challenges and unpredictability.

Especially on BSNL where govt PSU moves very slowly. I do see good times ahead where real comparison is Annually on revenue and Profit., not Q-on-Q.

Much depends on how Uniserve Nxt turns out as that is their flagship product and engine to do everything they trying to do. International visibility and System Integrator revenue share increasing is good sign.

Disc: My largest bet is Intense and I continue to hold with heavy loss. Definitely biased.

9 Likes

Thanks for putting up the summary. I went through the transcript as well and found that your notes cover the whole concall pretty well.

Now some questions, if you or anyone else can answer -

-

They have repeatedly said they are looking for integrators to find new clients. Weren’t they doing the exact same thing earlier as well, when they had trouble scaling up and receivables issues with large integrators? What are they doing that is different than that model? May be the were earlier solely at the back-end while integrator was managing the front end part of the contract (dealing and implementing at client’s)? This time Intense is at the front end as well and integrators are just trying to help them sell with their overall enterprise portfolio?

-

When they say 100 million revenue by 2022 (they themselves preconditioned it). 100 million means 650 cr! They are currently at 70 cr. Probably they are seeing the potential in their product but aren’t sure if they can really scale well as they don;t have money and bandwidth!

-

Can anyone in Hyderabad or travelling there can actually go and check their office and software? I get a feeling the product is good, but any firsthand experience about visiting the office and product would be great.

-

What is this BSNL contract add to the topline annually? 25 cr? as this being 6 year contract for 150 cr.

1 Like

Great questions @Mridul.This helped me to look for answers!

From Q3-2016-17 conference call - CK Sastry says - " even we are working with large system

integrators; the good part of it is that we are able to now stand up on a very good

footing. Earlier what used to happen is we used to be behind the system integrator

and they used to drive the sale, they used to do everything and no transparency on

pricing. It was just that they used to do purchase from us. Now with the system

integrators, we are asking them to directly put us in front of the customers. We are

able to convince the end customer to place the license order directly on us."

“the growing trend amongst the customer community itself to speak to the original principle vendor

directly and depend on the SIs for project management”

Even another reply indicates, operations support earlier was with integrators. So no cross selling and up-selling and that is also changing.

Direct sales also happening like in Vodafone and Reliance deals, if I understand correctly again from Q3 2016-17 call transcript.

Hope this answers Q1.

Q2: Yes, I think they see potential and hope that much before that point a strategic partner can help them to show case the product in much better ways

Q4: from above notes : This phase is revenue sharing model and we see the bare minimum revenues from that is slated to be around Rs. 40 crore to Rs. 50 crore in over about next five years.

Now what way BSNL will go in 5 years, it is not easy to predict. If customers flee them in droves, revenue also will drop. I do see min revenue per year is 40 crore/5 that is approx 8 crore averaged over years, as per management.

2 Likes

Kuber India Fund purchased more than 1 Lakh shares of Intense Technologies yesterday.

Ref NSE bulk deal data

3 Likes

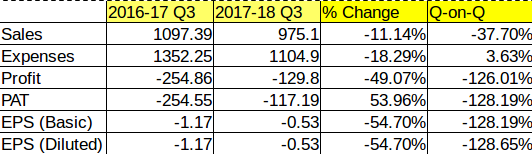

Results continues to be bad

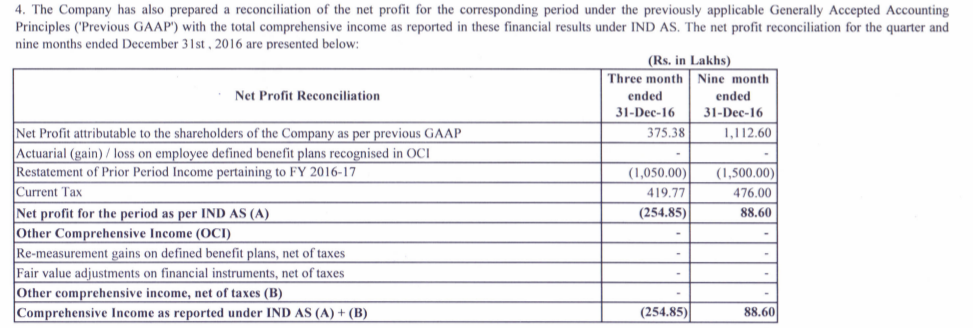

Apart from that 21.34% of 2016-17 revenue wiped out by a restatement for the period Sept 2016 (4.5 crore) and Dec 2016 (10.5 crore) which is more than 150% of current Quarter revenue supposedly due to invoice dispute making those periods as loss.

Impact on profit on the said periods are given below.

For more details and notes where last year accounts restated please refer

https://www.bseindia.com/xml-data/corpfiling/AttachLive/25f76171-21d2-4675-836d-202a3f1cb004.pdf

On a lighter note, I like their moto in the letter pad “Our intensity, Your Agility” … Looks likes literally true that they are intense in their actions and if I/you are agile we can survive their agility.

Disc: Reduced my exposure to this counter.

3 Likes

Q3 conference call transcript.

Keeping fingers crossed to see if word and deed will match and if the management can bring the company out of woods.

2 Likes