Sharing a thread on intellect by sapling capitals

Using other people words on the stock as I am not good with words and presentations

It isnt the software product enterpreneur that need to learn how to run a software product company, he has all the skillset, its the indian investor/vc community that needs to learn to value them to inspire risk taking for the enterpreneurs to dedicate their life to the pursuit.

Stunning results from #IntellectDesign , pat of 80 crores as against loss of 11 crores last year. Sequentially a stunning growth of 35% in bottomline. Trading at ridiculously cheap valuations now for a software product company with great products. long way to go. (on last qtr results)

To sell cement 2day, u gotta make it 2day

To sell cement day after, u gotta make a new batch to sell.

Develop a software product 2day,

Sell it 2day, 2moro, next year.

Simple Stuff Desi analysts dont get,

& then they go value product tech cmpnies like conventional products.

Temenos a company, #Intellect recently beat amongst 20 others in a Canadian bank deal trades at a valuation of $10 billion( 70k crores) at a price sales X of 10. Intellect doesnot even consider them competition, Palantir, a cmpny that intellect considers so, trades $55 billion.

In this context,to see #Intellect trade at a sub $1 Billion valuation is appalling, yet we love it when such a thing happens as it provides a great opportunity to back up the truck and load. Thank you Desi Analysts! (Feb 5 post)

What analysts cant get through their heads is the power of generating expenseless Revenue. Quarter gone by #intellect generated an almost expenseless 80% Ebidta margin (License+SAAS+AMC) revenue of 206 crores. The current valuation doesnot even begin to bake in the size of that .

The operational expenses have stabilised around 285 crores for the past 3 quarters for #Intellect, all incremental sales beyond that is directly moving to bottomline with the business turnin net cash positive, there are no interest servicing expense. Evident in the numbers below

https://pbs.twimg.com/media/EtdbZKGUYAsm581?format=png&name=360x360

Essentially what this means is even if the topline grows 10% an incrementally, even that 10 % increase in topline would directly mean a 30% jump in bottom line.

Thats the operational leverage that comes into play once a software product gets references in the mkt.

The product does not need to be sold as hard as the product develops a natural pull in the mkt with increasing references, even the discounting reduces over the years this all adds to the bottom line.

A S.Product becomes a cash generating machine beyond a point

As the product gets sold to more and more products and with the incorporation of customers demanded domain dictated changes the product with increased features evolves into a much more useful one for the next buyer thus snowballing its value proposition with time.

What reduces the marketing costs further is the rating of the product by analysts like Gartner, Forrester, etc. A lot of RFP’s come to the market only seeking technical bids from vendors present in Gartner quadrant. This auto selection reduces the need to market extensively.

What delivers further optionality over core products are the 2 new Platforms #Intellect has developed namely Iturmeric and IDX Iturmeric is a platform on which customer can develop his business processes on drag and drop tool without the need to code. Customers love such things

Whereas IDX could prove to be the real game-changer for Intellect, its just got rated the best in the world by Novarica, its an ML/AI based data tool that helps insurers underwrite better.

What makes IDX a game changer is that IDX requires no customisation at all, its a buy and use system and is pure money from Intellects perspective and being a ML based system it gets better every time its used.

If IDX scales it will give a hockey stick look to Intellect numbers.

Software deployed in US banks havent been changed in the longest time due to the pain involved in carrying out such massive chnge.

Covid has truly made ppl realize the shortcomings of incumbent software and the drastic neeed to replace them with cutting edge.

Opportunity Galore!

Excerpt from Temenos call: Talking about shifting operations from other locations to India to save cost. Shows the competitive advantage #Intellect has. #Intellect has spent 1300 crores in product RnD. The same work in Europe would have cost 5x( more than Intellect’s mktcap)

Unlike IT sevices, software products is a different animal.

A product has a much more long gestation period.branding is a huge element of the selling of the product especially in developed countries.

Everyone knows the likes of TCS, HCL, infosys in the developed economies.

But their havnt been too many Indian product success stories. The fact that its an expensive game can be ascertained from the fact that #Intellect has spent close to 1700 crores in SG&A expenses to build its brand.

Similarly the product acceptance is also dependent on vendors having a local support presence to aid the customer, thus it requires building up of a partner network, all these are expenses that have to be incurred upfront.

But every incremental sale doesnot require the same amount of per unit marketing,rnd spend as the infra is already setup and thus bottomline explodes.we are at that inflection point for intellect with the bottomline likely to look significantly higher than what it is today.

#Temenos in latest call talking about how US banks are still using 50 year old software representing a great opportunity for new products to replace the incumbent. Same addresable mkt for #Intellect. #Temenos at 36% margins from Europe. Huge sales & margin upside for Intellect.

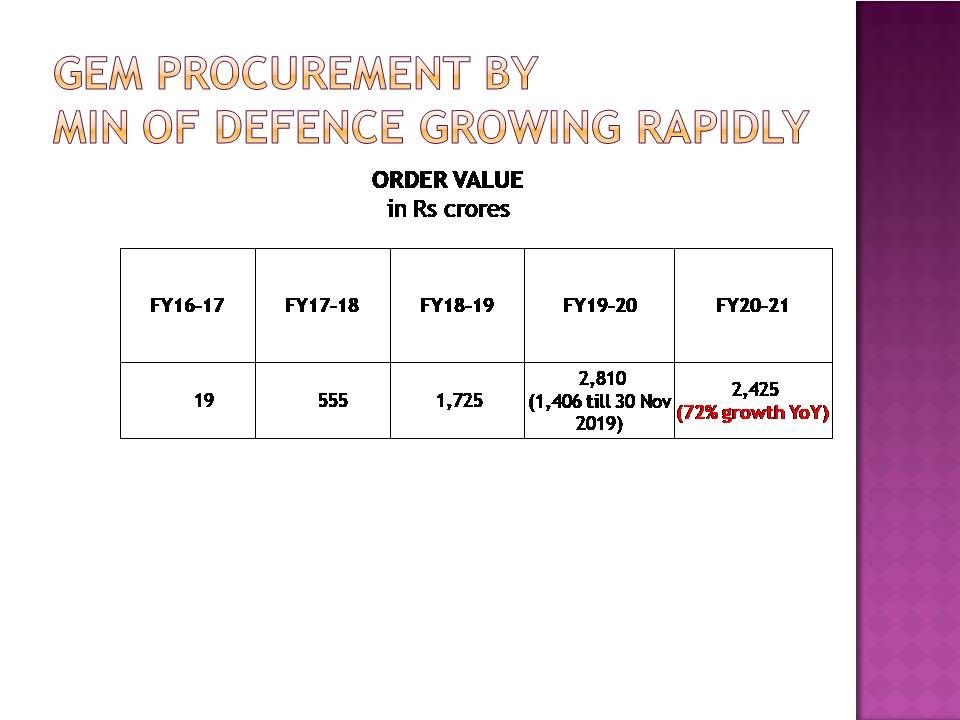

With the GEM portal of the government working at full steam, #intellect stands to gain additional revenue stream to benefit from the uptake of procurement in GEM.

#Intellect launches it IDX AI, ML based Aadhar processing solution called Magic Aadhar. Yet another amazing use case for its AI ML platform called IDX. It will help reduce friction by protecting customers’ personal Aadhar data from being misused.

#Intellect now has a SAAS ARR of more than $21 million. Most analysts donot understand the significance of that number and how things scale in SAAS, will only dawn upon them too late.

Temenos achieved an EBIDTA margin of 44% in Q4 Fy19 with European costs structure, thats the kind of upside to current margins #Intellect can achieve as the expenseless ARR’s keep increasing qoq.

The same improved further to 47% in the most recent quarter.

Recently Temenos also announced its targets for the year 2025 including a 15% SAAS ARR cagr for next 5 years.

Does throw light on the humongous opportunity size available to

Temenos CEO on the Opportunity size available to the Software products players in the banking space.

$63 Billion growing at 8% Cagr for next 5 years.

A wonderful session by #intellect today , an initiative a lot of tech companies can replicate. Intellect has a Net promoter score of 60 which is industry leading. Even Gartner has noted that #intellect has received the best ratings from Customers vis a vis competition.

Disclosure: As above

Though regret due to to covid time due to fear could allocate just 7% to the stock