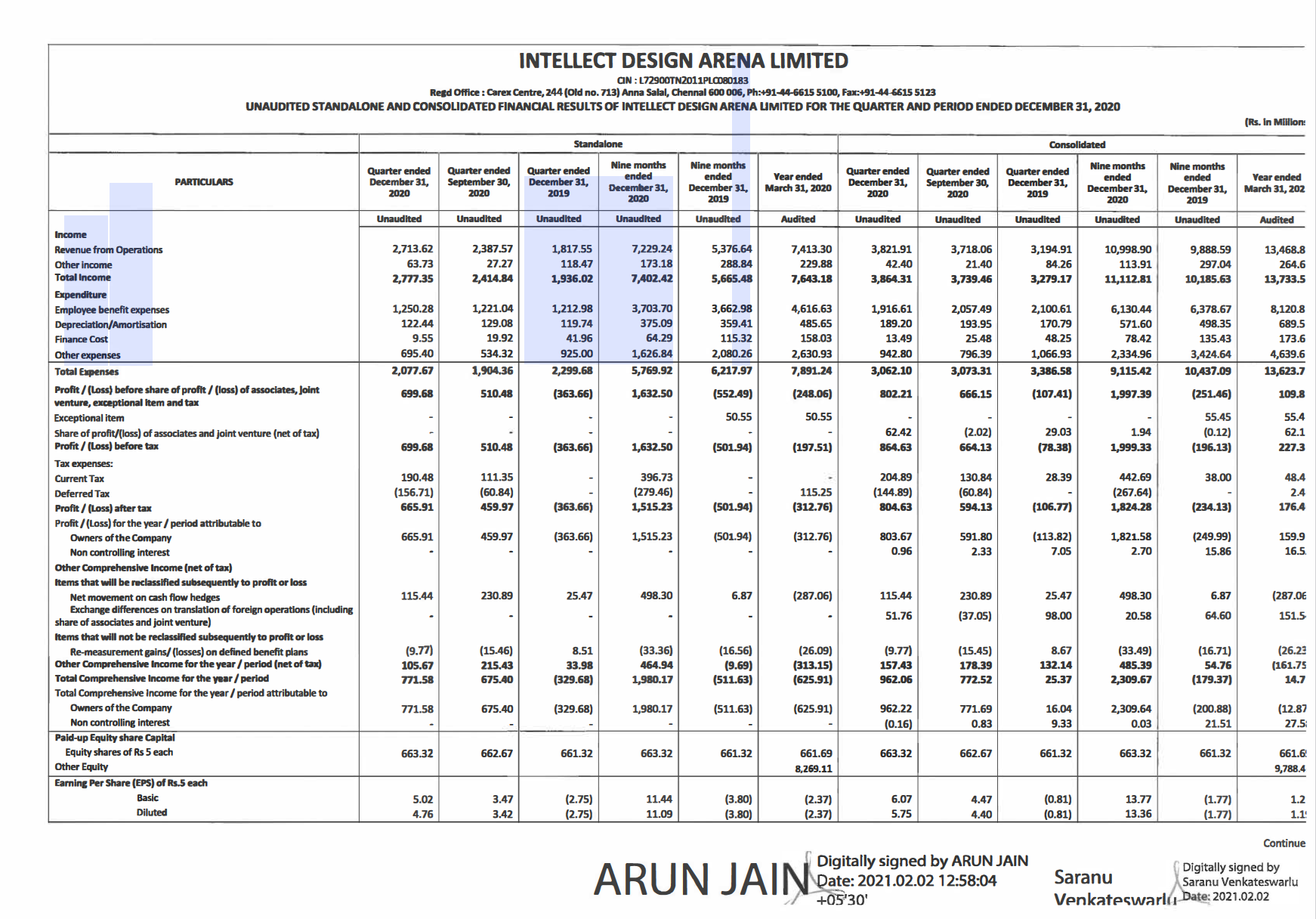

Intellect Design should report a topline of 200m dollars for FY21 having already achieved 46m in the first quarter. Recently temenos which is one of the biggest player in the sector acquired a co in the americas called kony at a valuation of 5x ev/sales. Kony’s expected revenue for fy20 was 115m dollars. The recent majesco deal happened at 4 times ev sales. I think intellect is in some ways superior than majesco because it has diverse products across the consumer/transaction banking and other niche products and in case the nos hold out well, the co should at the minimum trade at 4-5x sales. Ebitda margin can also inch up to 30 per over the next few quarters.

Temenos trades at 10/11x sales and close to 60 pe. Even if you want to give a 50 per discount to intellect considering temenos does about 35 er ebit margin and intellect can report ebit margin of 23-25 per in the next few quarters. Temenos converts all of its ebitda into operating cash flow. Intellect should get there soon but even if it does 60-70 per ebitda to cfo conversion, dont think more than 50 per discount to temenos’ valuation is warranted . target market cap can be in the range of 6000-7500 crores which is 4-5x sales.

maybe from q3 on onwards, intellect can start reporting close to 60cr pat every quarter because the management has guided in the concall that almost every additional topline beyond 46m , 90 per of it will flow to ebitda.

At 50m dollar run rate, intellect can report ebitda close to 15m viz 100 crores and a pat of 60 crores every quarter. Current market cap is 2500 crores. Even at these levels, feel there is a margin of safety.

This report from Dolat is very detailed. If someone wants to go through the report and understand the entire business & the prospects, I have attached here. The products, company history and valuations are all analyzed & projected in great detail. I am quoting the valuation part of the report for reference of Revenue & EPS growth estimate of 13%/152% CAGR over FY20-FY23.

License Revenue has robust growth aspects in comparison to AMC Revenue and hence the focus is to increase License Revenue.

Intellect’s Vision 60:60 ie, 60% License Revenue contribution and 60% Gross Margins. License Revenue has reached ~57% of Revenue over the years and is very close to the company’s aspiration.

Cloud Revenue consists of two business models: a) Monthly Subscription Model: Business is very consistent with constant growth. b) Consumption-based Model: Business is based on consumption and keeps fluctuating based on the volumes. There is a small dip in the consumption business during the quarter.

Budget Approvals and POC are taking shape as clients are adapting to the WFH business model.

Artificial Intelligence & Machine Learning:Intellect SEEC is being utilized for data in AI and ML activity and has 10 customers who pick up data packets from Intellect Design stations via AWS cloud at a reasonable price ranging from $1-2 per 100 data packets. Liberty Insurance is consuming the data for their underwriting Insurance.

Operating Leverage play has helped the EBITDA Margin expansion from 20% to 24% and EBITDA Margin is set to expand to 30% over the next 4 quarters. EBITDA Margin aspiration of 30% will come from 60% Gross Margin minus 22% from SG&A costs, 6% from ESOPs and 2% from provisioning.

iGTB: Overall customers count stood at 91 and pipeline looks healthy for H2. _The platform has solutions such as 1) digital liquidity with the help of cloud services, 2) Contextual Banking Experience - which is the first cloud product is gaining momentum in the market - and 3) Integrated Payments and Payment Services Hub during the current quarter.

iGCB: Intellect closed four deals including a multi-million Dollar upgrade deal with NABARD for their core banking and lending transformation. Positive Outlook in the European region as the firm has gained few clients from that geography and chasing a destiny deal which will be decided over the upcoming quarters. Quantum Banking which is a Central Banking product is reaching maturity by acquiring clients and critical mass in revenue.

Intellect SEEC: Intellect SEEC is a cloud-based platform which helps the customers use internal and external data to make decisions and is used in Risk Management, Business Development, etc. Platform has been expanding in Australia as the firm signed a large insurance client in the region along with another large client from UK. Business is a subscription-based model.

iRTM, iWealth & iGov: Wealth & RM has closed 2 deals in Singapore and with a very large account in India. Conversations for these platforms are encouraging and more deal wins are expected going ahead. iWealth has two ongoing client engagements in India & South East Asia. iGov Business is on growth trajectory over the next two quarters as business volumes accelerate over GeM portal.

Geographically, America has been struggling for the past few years however green shoots are visible and the geography will outperform going ahead.

DSO stood at 127 days as against 126 days in Q2FY20 and the DSO will improve in upcoming quarters as three new deals go live in the APAC region.

Debt: INR 707 Mn of debt on books, INR 600 Mn consists of Term Loans and INR 100 Mn consists of Short Term loans in form of Overdrafts.

Outlook: i) Technology in Financial Sector is becoming like API economy where solutions are available on the cloud and clients can select and modify their products as per the requirement. ii) Made an additional R&D Investment where products were launched on the cloud platform and Intellect has 900 APIs available as of today. iii) iTurmeric has been made available on AWS Cloud. iv) Product & Cloud platform has accelerated Intellect’s ability to secure deals with the clients and will contribute towards a healthy deal pipeline going ahead.

Intellect Design Arena.pdf (1.4 MB)

Attaching my note on the company. Hope the note adds value. The note was first written few months back so some tables might be slighly old. Valuation table has been updated based on current price and my earnings expectation post Q2. I have also included my takeaways from calls with company and TV interviews.

Dis: Took a decent size position at 240. Averaged up small at 285 and 320. 10% of equity portfolio

This is a super detailed and comprehensive note. Amazingly detailed

I have been tracking Intellect for some time and there has always been some reason for it to miss profitability till last fy. The last two quarters surprised significantly on the upside.

Can you help me with some more detail. Your assumptions for H2fy21 are super bullish. Likewise your assumptions on profitability growth are super bullish for the subs equent two years. In the past company has always flattered to deceive.

Can you elaborate your thoughts for this high growth percentage

Regarding topline growth, I don’t think my number for H2FY21 is bullish. INDA did $96m top line growth in H1FY21. I am building $199m for FY21. While there will be QoQ volatility in license revenues, overall I think the environment for digital adoption by banks is strong, more number of products are now in monetization stage, AMC and cloud based revenue should accelerate compared to earlier years. Bear in mind that AMC revenue lags license revenue growth by 6-8 quarters.

Regarding profitability, company is in stage 2 (more products in monetization stage) and thus R&D cost as % sales will come down. Please see that R&D capitalized has been stable in last several quarters. AMC revenue will increase as % of total sales and that comes with little incremental cost. Company indicates that incremenal margins on recurring revenues would be close to 80%. Please see how margins have moved from Q4F20 to Q2F21. INDA can also reach 30% EBITDA margin in next 4-6 quarters. GeM platform should also have high operating leverage.

If anything I see higher probability of upside risk (than downside risk) to my numbers for FY21 and FY22.

Great stuff! However,your EBITDA estimates seem quiet conservative given that Mr. Arun Jain is on record saying that IDA plans to achieve 30% margins at the EBITDA level within 4 quarters.He said it in the last concall.

Link to Earnings call held on 2nd February 2021 - https://www.youtube.com/watch?v=HVqiuqeu0OQ

Absolutely worth listening from 23:00 until end. Its extremely heartening to see an Indian company being proud to show off its Intellectual Property credentials. The credentials they have built is likely to force them to get acquired or get listed independently in the US and Mr. Arun Jain is hinting about it(getting its products listed in US) in his closing remarks.

Additionally,

when was the last time a senior guy from Liberty Insurance joined a Indian small cap company to lead its Insurance product business in US.

large deal won and gone live in 8 months in the midst of Covid19.

both of these this sounds absolutely path breaking.

While the management is calling it cautiously optimistic of its growth prospects, it looks like good times ahead for all stake holders.

AJ

Disclosure: Invested. Views are biased.

Management indicated that one can expect 30% EPS growth CAGR and low double digits to mid-teen top-line growth between FY21e and FY23e

Currently, only 2-3 products in the monetization stage which is driving financial performance

Intellect 2.0 will get over in March 2021 and Intellect 3.0 from Q1FY22 which will involve more products getting into “Aggressive Selling and Premium Pricing” stage

License-linked revenue crossed the 53% mark and management targets to increase the contribution of this segment to 60% which is important because it is 70-75% gross margin and therefore aids in achieving 30% EBITDA aspiration

iGTB: 4 out of the 5 platforms under iGTB performed well during the quarter. Digital Transaction Banking, Supply Chain Finance, and Trade SWIFT saw traction during the quarter | A top 10 US bank went live with Liquidity Management solution within 8 months in the lockdown – which shows the capability of execution | Launched 3 different upgrades across 3 sub-platforms in the iGTB space which saw strong traction

iGCB: won mega destiny deal in Germany with 2nd largest e-commerce retailer – OTTO. Intellect went through a comprehensive selection process wherein OTTO considered build vs. buy as well as RFPs from several other FinTech providers and Intellect emerged as leader | Won 1st cloud subscription deal in mid-tier bank in North America in Canada which had 20 competitors bidding for it | Ready to launch IDC 21 microservices version which is an open API and Cloud native platform | Management sees good traction in the Lending Product and Central Banking product in the upcoming year

SEEC: is a product pertaining to insurance business which is 100% cloud and 100% subscription. Data platform is at the heart of the business | Won 10th customer in this segment | “Magic Submission” module which was launched in November as an AI powered hyper automation tool is gaining immense traction

GEM portal has crossed INR 10,000 Cr of GMV in Q3FY21

In my opinion SAAS/Cloud based solutions are the way forward, more and more disruptive solutions are offered . These onsite installations are going to go away soon.

Watch this SAAS company (at the moment this is the only one that I have come across )

Bank / FI doesn’t have to spend millions to develop in house softwares , just rely on SAAS based cloud solutions.

from Personal experience, Banks are unlikely to go towards Cloud adoption, and even if they do, it will be limited to productivity apps. Banking (core banking, Risk management, P&L) kind of systems will never go to SAAS (possibility still exists for them to go to personal cloud).

Reasoning for it is the Regulations, Internal Controls (banks typically dont like their systems in cloud).

Banking is all about payments, big data and analytics these days. The core data continue to sit in internal servers and data warehouses and not on cloud due to known and well documented confidentiality and security issues. The payment, analytics, customer engagement and screening applications are on cloud and communicate with the servers/ storage via API’s which are well secured. Banks all over the world is adopting these technologies at a frantic pace - you can talk anyone from the industry(or just google it) and understand this better.

Looks like a lot of retail investors are making the same old mistake. Look at the volume once the circuit move to 20%.

I’m not recommending anyone to buy or sell, but if you are convinced on the fundamentals. then don’t fall into the short term trading trap - what you may miss out today could be an opportunity which comes only once in a while.

AJ

Disclosure: Invested, added today and my views are biased.