Shankara Building Products - http://shankarabuildpro.com/

Promoter - Mr. Sukumar Srinivas (IIM Alumnus)

Background:

Shankara Building Products Ltd (SBPL) is one of the leading organised retailers of home

improvement and building products in India based on number of stores. As on December 31, 2016, it operated 103 Shankara BuildPro stores spread across 9 states and 1 union territory in India. It caters to a large customer base across various end-user segments in urban and semi-urban markets through its multi-channel sales approach, processing facilities, supply chain and logistics capabilities. Its retail operations are strategically suited to benefit from growth in housing demand, large market for home

improvement, and increasing customer involvement in home solution decisions which have

created a need for organized specialty home improvement and building product stores. SBPL’s

growth is further driven by its ability to make available an assortment of quality products under

a trusted corporate brand built over two decades. It also provides delivery and facilitates

installation services for select product categories.

Business Units: 3 (Retail, Processing, Enterprise)

Source: http://www.hdfcsec.com/Share-Market-Research/Research-Details/IPOReports/3021825

Promoter stake: 56.20 %

Based on IPO upper range of price 460 and Considering March EPS of 26, PE comes out to be 17.69. At the issue price, the stock was valued at 0.6 times on an EV/sales basis

Current Price = 686, Forward EPS FY 18 expected Projection of 33, Forward PE comes out to be 20.78

Retail stores growth from same store sales growth could reach 30-33% in FY2018

Net Revenue growth from FY 12-16 is CAGR 9.55%

Moat #1:Low cost player in Integrated Building Material, Scalable, Backward Integration

Moat #2: No competitor who provides integrated building materials under one roof

Moat #3: Agency Moat. Builder, Carpenters, Electricians and other Tradies can buy from the store and pass on the price increase to the customer. When the customer is not directly involved in the purchasing decision then higher prices can be used to bribe the purchaser’s agent (builder or other tradies) and can result in higher profit margins and sales volume. This is called as Agency problem. In similar instances globally, it has been found that margins remain low so as to offer quality, cheapest cost material, diverse product range to the customer. For ex: Bunnings. It is hard to keep margins in double digits in this business. So, you can play valuation on Sales volume and low cost advantage.

Moat #4: High entry barrier due to lot of moving parts. Typically it is very hard to keep this business profitable. Only few players can enter the integrated building materials retail Brick and Mortar Business. Lot of Regulatory approvals, Land Leases and Capital is required. Management is very critical to keep the cost optimized and manage moving parts including Suppliers, Customers, Technology, Logistics, Inventory, warehousing, Payable, Receivables, Capital Allocation, Store Geo Presence, Same Sales Growth. For ex: Masters chain in Australia got busted in no time due to incumbent player Bunnings. It is not easy to make money in this business as there are lot of moving parts.

Tailwind: Housing for all, Urbanisation, Increase in Population growth (projection of 11% from 2011-2021), GST (Unorganised to Organised), Have own Steel brands, Organised retail projected to grow at 22-24%.

Retail Key Products: Cement, Structural Steel,Bricks, Plumbing(PVC Pipes),Ceramic tiles, Sanitary Ware, Plywood, Laminates, Lighting.

Retail sale of above products constitute 34-38% of total sales. The balance takes place via institutional and wholesale channels.

Investment Rational:

a) Asset light strategy for opening retail shops

b) Backward integration with processing facilities, owned

warehouses and logistics

c) Strong track record and sound financial strength

d) Presence across the value chain through enterprise and channel

sales

Source: http://www.nirmalbang.com/Upload/Shankara%20Building%20Products%20Ltd.pdf

Management Latest Interview on April 06, 2017 Shankara building: We would be adding 15 to 20 stores every year: Sukumar Srinivas, Shankara Building, Real Estate News, ET RealEstate

- 15 to 20 store addition every year

- Consolidation in South India, looking to diversify geographically in next 2 years

- Margin improving albeit little, Aim to focus on Profit Margins…6.5% this year

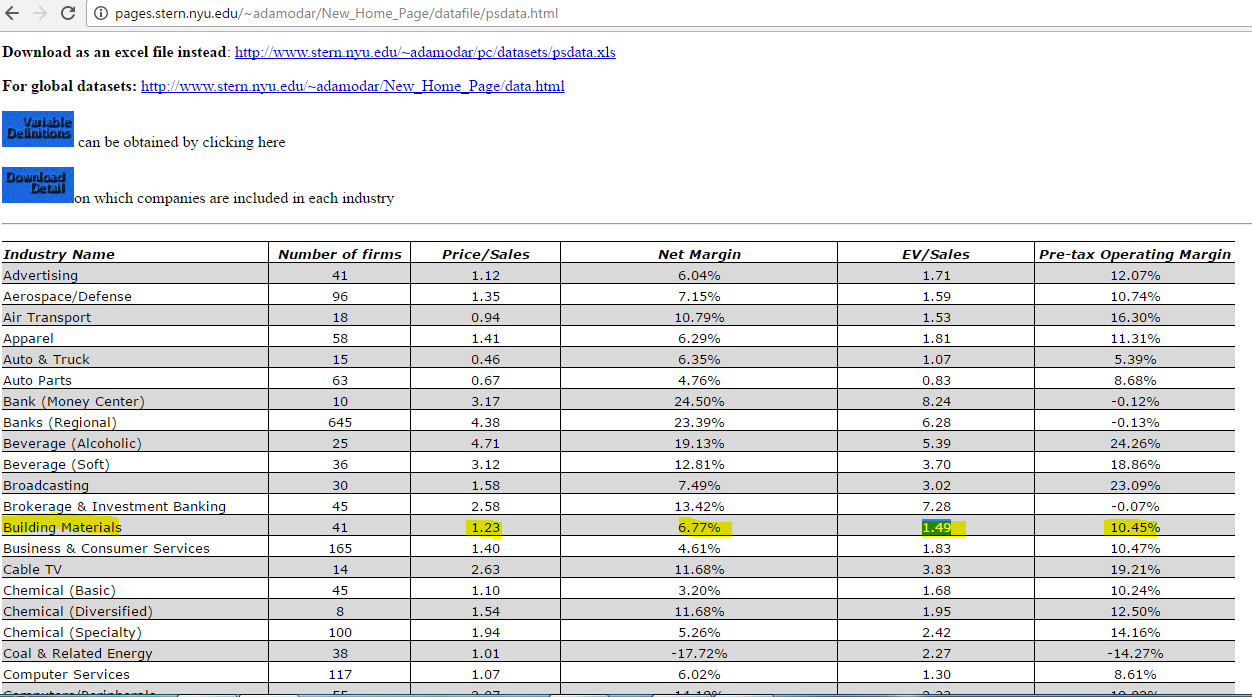

As per US data complied by Prof Damodran,

Yellow highlighted data shows Building materials valuation on P/S, Net Margins, EV/Sales

Cheers,

Amit

Disc: Invested 2-3% of PF recently,