Shankara looks interesting. Considering the success of similar model in the West and housing continues to be a key economic activity (in most tier-2/3 cities and near by rural areas, most construction will be independent houses built by self and not through RE developers) this seems to be well poised to take benefit of the housing growth.

A couple of questions that come to my mind. If any one has looked at these, will be great to know the answers -

-

In most tier 2/3 cities there local dealers that sell building material. What advantage does Shankara offer to the buyers which will attract them? If I think of D-mart vs. kirana stores, D-Mart offers discount which is the value proposition. What is Shankara’s value prop to the customers?

-

What is the competitor land scape? Are there any other listed/unlisted players in the same space?

-

A number of analyst reports have come recently projecting 30% CAGR for NP over Fy18-20. What can upset this? We should think through this as at the current valuation (50 PE trailing), is there is much MoS?

-

The opportunity size seems huge 2-3 Lakh Cr. growing at 8-9% PA (did I get this right?) If this is true, why isn’t Shankara not able to grow the top line aggressively? Most analyst reports are projecting 10-15% growth and management also indicated mid teen kind of growth.

-

Are their own brands making money or are they just suckers? Does the management plan to focus on being a retailer for other brands or spend money on own brands (could require significant money to establish a brand).

-

Has any one done any scuttlebutt - either talking to the customers or their supply chain?

Regards

Disc - Not invested. Actively considering.

Added three more stores in Chennai by taking over operations of existing three stores of Vaigai sanitation. http://www.bseindia.com/xml-data/corpfiling/AttachLive/cd2db304-2437-4ec6-a180-6201a782fbb0.pdf

This gives me confidence that, Shankara is well set to exceed its target of adding 15-20 new stores annually. During the first 7 months of FY’18 itself, 15 shops got added already. At this rate, they may even add 26-30 shops during the whole of FY’18. This is much higher than the 11 shops (approximately) which they added during FY’17. I am very eager to see when will it reach (or, has it already reached?) the inflection point which I mentioned in the below post ![]()

I am tracking this company, Will try to answer as per my assessment of this company

Answers

Question 1- SBP can provide the varieties and options to the client which the local dealer cannot provide. Like SBP has tieup with 100 brands and 20000 SKUs which are increasing. These options which were not available to end users earlier in tier 2,3 cities are now available to them.

Question 2- Other local players.Stores like Hometown,lot of Home decor startups like Peperfry and others in the home decor category but not end to end. Still searching on the same.

Question 3-

Risk1 -In the Concalls the company management said they are changing the locations of their stores and changing the format of their stores to attract new customers. If this strategy fails and they are not able to increase the footfalls then it is a risk.

Risk2 -If they are not able to do the right inventory mix and not able to gauge the end client mindset by watching the market trends then it will pile up the inventory

Risk3- Presence only in South India. This can be taken as an opportunity as well as threat as if the demand for housing slows down in South India then it may impact the business. As an opportunity the business can spread to other parts of the country

Question 4- Yes the opportunity size can be that big as I heard for the Home decor market the market size was estimated to be 1.5lakh Cr in one of the episode of Awaaz Enterpreneur dedicated to Home Decor Segment. Others can comment

Question 5- They are having some in-house products for steel pipes,roofing sheets. Other than that I dont think if they have their own range

Question 6- No I have not done scuttlebutt. Others from South region can guide

Disc: Not invested as quoting at High PE, tracking closely

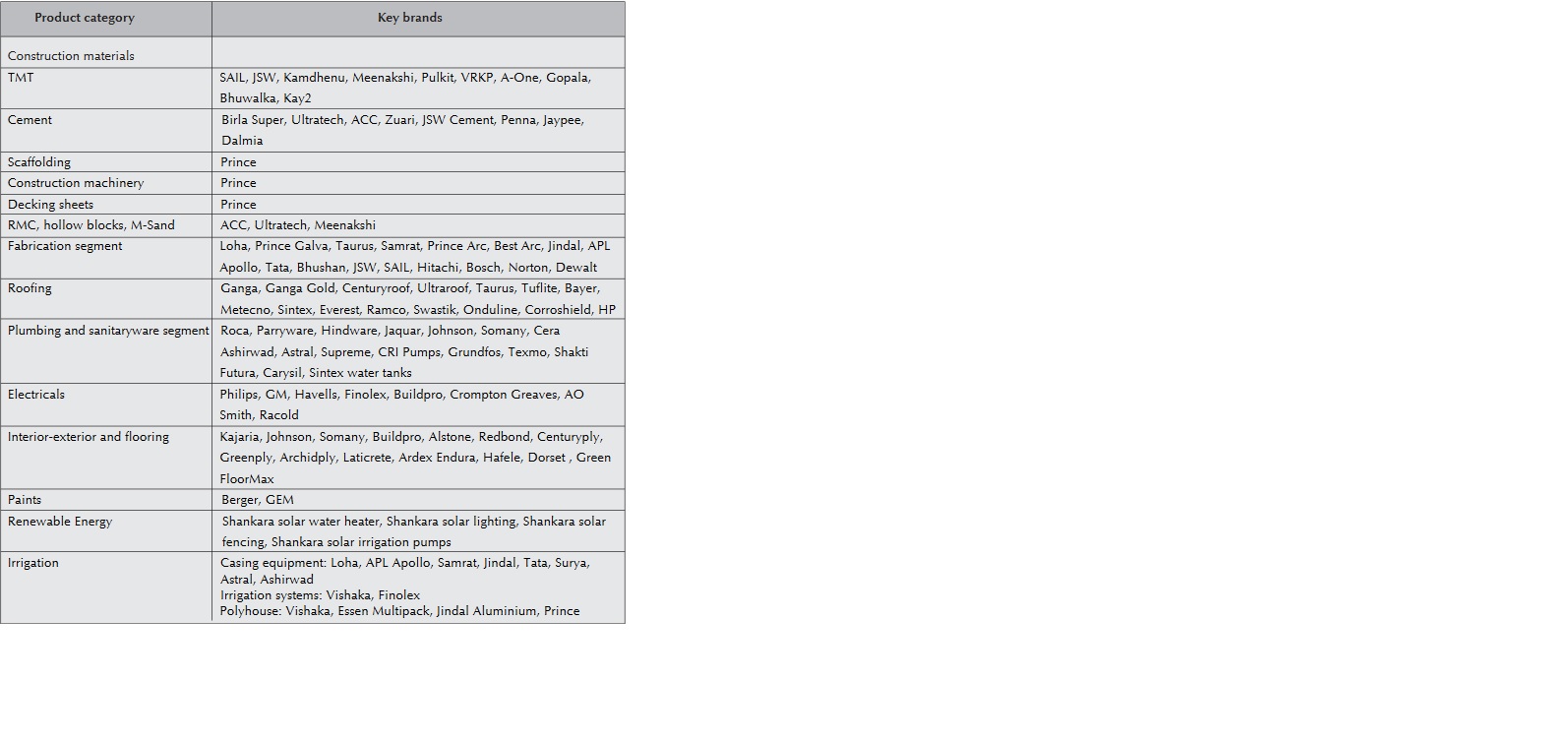

Was going through the AR of 2017. Below is the statement related for their own brands

"

. In addition to third party brands, we also sell our own private label

brands such as – Buildpro, Taurus, Ganga, Century, Ultraroof, Loha, Prince, Samrat and Shankara Solar. Currently

around half of the sales in our retail outlets are of our brands."

Below is the segmentwise brands listing.

Have been watching Shankara for last 3 months making new highs. But today made the decision to enter the stock. Catalyst was the Peter Lynch book “Beating the Street” where he says that he prefers retail and restaurant stocks as model can be replicated across whole country. Same is true for Shankara in Indian context. Here, retail stores have their own challenges and food preferences differ a lot. However, one thing is true for whole country and that is fascination about “apna Ghar”. That’s my simple thesis. Let’s see how management executes.

http://www.bseindia.com/corporates/ann.aspx?scrip=540425

Quarterly result publication .

Good set of results.

ROE and RCOE have been going up and D/E has been going down. GST has positive effects on the revenue (read page 7)

Investor ppt

http://www.bseindia.com/xml-data/corpfiling/AttachHis/6db6335e-44f5-42ee-a1c3-6dfefab2d228.pdf

Increasing share in Telangana and Karnataka. Own product sale increase in H1FY18.

Mgmt will add 15-20 stores every year. In 3-4 years the store count could touch 200. We are only talking South India. Rest of the India market is still up for grabs. Opportunity Size huge.

Negative is subdued demand due to slowdown in construction

~ Shankara BuildPro Mgmt

Slide 15. Current liabilities is wrong. It should be 530 odd crores not 1479 crores. I liked the presentation, very direct and no unnecessary stuff. Not sure why 45 crores of IPO proceeds was not included in roe calculations. Have these not been put to use?

Really liked the presentation. I like the business as it squarely fits in with what appears to be the government’s thrust for the economy. I expect to see improvement in real estate business from the end of 2018 based on my non scientific survey of whats going on in Pune. With its own products occupying a larger mix of the sales mix its margins will also improve. Overall I like the business and I expect this to be reflected more aggressively in the market price as well going forward. Shankara forms about 40% of my portfolio and this will turn out to be a really long term holding for me.

If it is 40% of you of then it calls for a detailed investment rationale for investing in this counter. Would you be able to write something up for benefit of all ?

Cheers

I will definitely try to put something together. But I think you have already done an absolutely fantastic job in the first entry of this thread by outlining the investment case really well and would recommend that entry to anyone who is looking for a starting point to analyzing this stock Not sure what more one can add. I can tell you how I decided upon Shankara though:

The investment case for me is:

- The business is simple (a very important consideration for me)

2 The business is scalable - There are meaningful moats

- The management seems to be doing a good job

- The story is very ‘marketable’ to large investors

In fact I mentioned this stock to an old fund management friend based out of Europe and he liked the story a lot. However he said Shankara is too small for his fund and he will look at it when its mcap is higher. I surmised this is the case with many large funds as well and foreigners will instantly compare it to home depot. Look at how the HD stock has performed in the last 15 years. As Shankara’s market cap rises, I believe it will start popping up on screens of larger foreign investors. Shankara thus gave me a great combination of a great business coupled with rising liquidity.This sense of what kind of demand this story would generate in addition to its business advantages so well covered by you prompted me to take a sizeable position in the stock at around six months back.

Comparison to Home Depot/ WalMart seems to be the latest rage in the Indian markets these days - how is that relevant to the Indian context? The attitudes and mindset in the US are very different to that in India. I am not talking about the “westernisation” of values we see in India today. Rather, DIY is huge in the US - how much do we really do that in India? People in the US take a certain amount of pride in buying and owning their tools. The DIY thing is something part of the American fabric…this has had a large role to play for HD. Will that be the case in India? Why would someone go to Shankara to buy Kajaria/ CERA etc. when they themselves are pushing hard for a retail play where they showcase their products? While I do not doubt that this is could turn out to be a worthy investment at this point it seems and feels more like a story stock.

From the experts on this counter, what is the bear case?

Disclosure: Not invested.

I agree that comparison to Home Depot are premature at this stage. Having said that, there is plenty of DIY in India, just that ppl engage others to do manual labor things on their part with full engagement. Shankara’s most successful stores are located in tier 3 cities. This in itself is a proof that there is a huge scope for building material retailing.

Kajaria/Cera pushing hard for retail play is favorable for Shankara. Why wouldn’t they like additional retail space at fractional cost of establishing their own network. This is similar to any other form of retailing. People were sceptical for FMCG retailing as well 10 years back, but landscape is totally different.

Besides, with 100 or so profitable stores, shankara has proven that this business model has legs. Future growth will depend on how company will be able to replicate it over it’s current geography and then to other part of country as well. Last thing any upcoming retailing business needs is too much growth aspiration in short time. Here, promoters looks pretty conservative with modest guidance of 15-20 new stores a year. I liked the fact they raised just 45 crs of fresh capital in the IPO, despite the fact that they could have easily raised much bigger amount in the name of fast expansion. With modest growth forecast of 15-20 stores per year, I don’t think it makes much sense to talk about bull/ bear case. Personally, I would any day prefer a 40% grower at 40+ pe rather than 10% grower at 15 pe.

Thanks

Disclosure- invested 10% of portfolio

With 60+ trailing PE, stock is now charting in unknown and potentially dangerous territory.

Would be interesting to know what chart is showing from technical point of view.

What is going on with this counter? Valuation book could be thrown out of the window. Who is buying at this price? Is there something which Mr Market knows and we are ignoring here.

I understand that, with Shankara, we have three different plays into one: Retail, Affordable housing and GST. Also, as @alimaye has rightly mentioned on this forum earlier, the story seems to be very marketable to large investors.

I am not knowledgeable to compare Shankara with Avenue Supermart, however, I see some similarities in the movements of both these stocks ever since they got listed. Both do not seem to be caring for valuations. Shankara’s current TTM P/E is 60, whereas for Avenue Supermarts, it is 121.

Both these companies have scalable business model and appears to have good management. Would like to understand from you all, if Shankara can catch up with Avenue Supermarts on its valuations one day (the way its stock price is moving up these days, I feel that it it may even happen). If not, why?

Disc: invested from Rs. 800 levels and it constitutes more than 15% of my portfolio

I think market is factoring in the fact that management is prudent with expansion with maintains good debt. Also once they reach critical mass in no of stores in 3 years, operating leverage would kick in as demand is expected to pick up significantly. We could see Top line and bottom line expansion once store expansion count is completed. Still feel valuations are expensive.

Disc: Reduced from 22% of pf to 15% now around 1500 price point.