Thanks much. This is interesting as it creates other follow up questions in my mind…

What other clearances have been awaited?

How can I tender my shares using a platform like Zerodha? I only see limit/market buy/sell option there…

Thanks much. This is interesting as it creates other follow up questions in my mind…

What other clearances have been awaited?

How can I tender my shares using a platform like Zerodha? I only see limit/market buy/sell option there…

you will get a Buyback form at your registered address - you are require to

duly fill it and submit to the mentioned address

alternatively one can do online also - this facility completely depends on

the broker you have…ICICI and HDFC have the option to apply for buyback on

their portal itself. so no need to do the physical mode mentioned above.

Zerodha allows emailing the tender form. Details are there in the wipro or tcs buyback thread

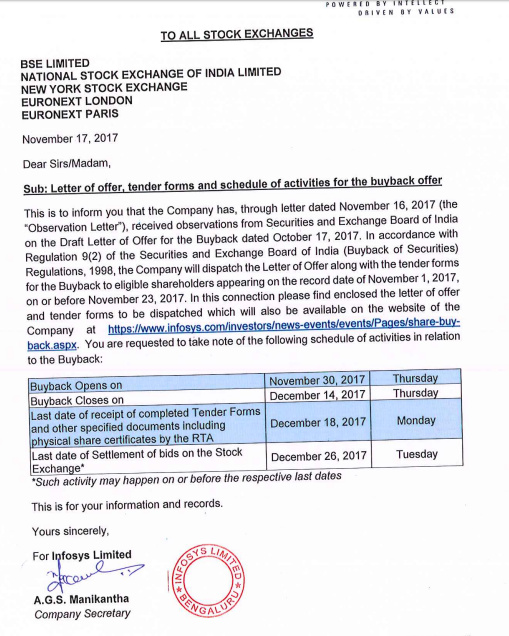

The latest on Buyback…

The full link here

http://www.bseindia.com/xml-data/corpfiling/AttachLive/ce71e23a-9a33-4585-bb22-8b754c3ddcaf.pdf

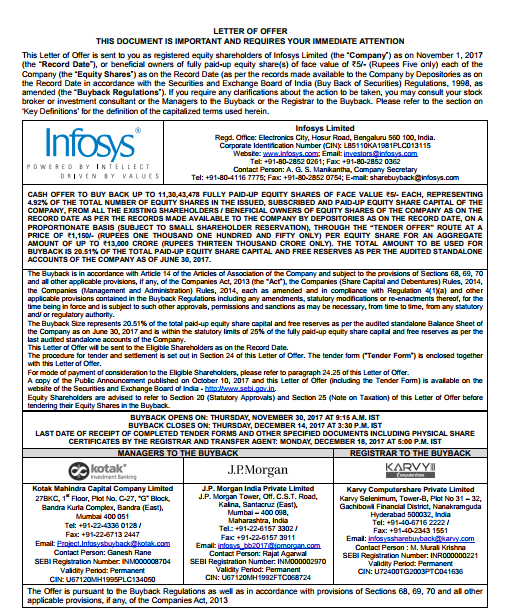

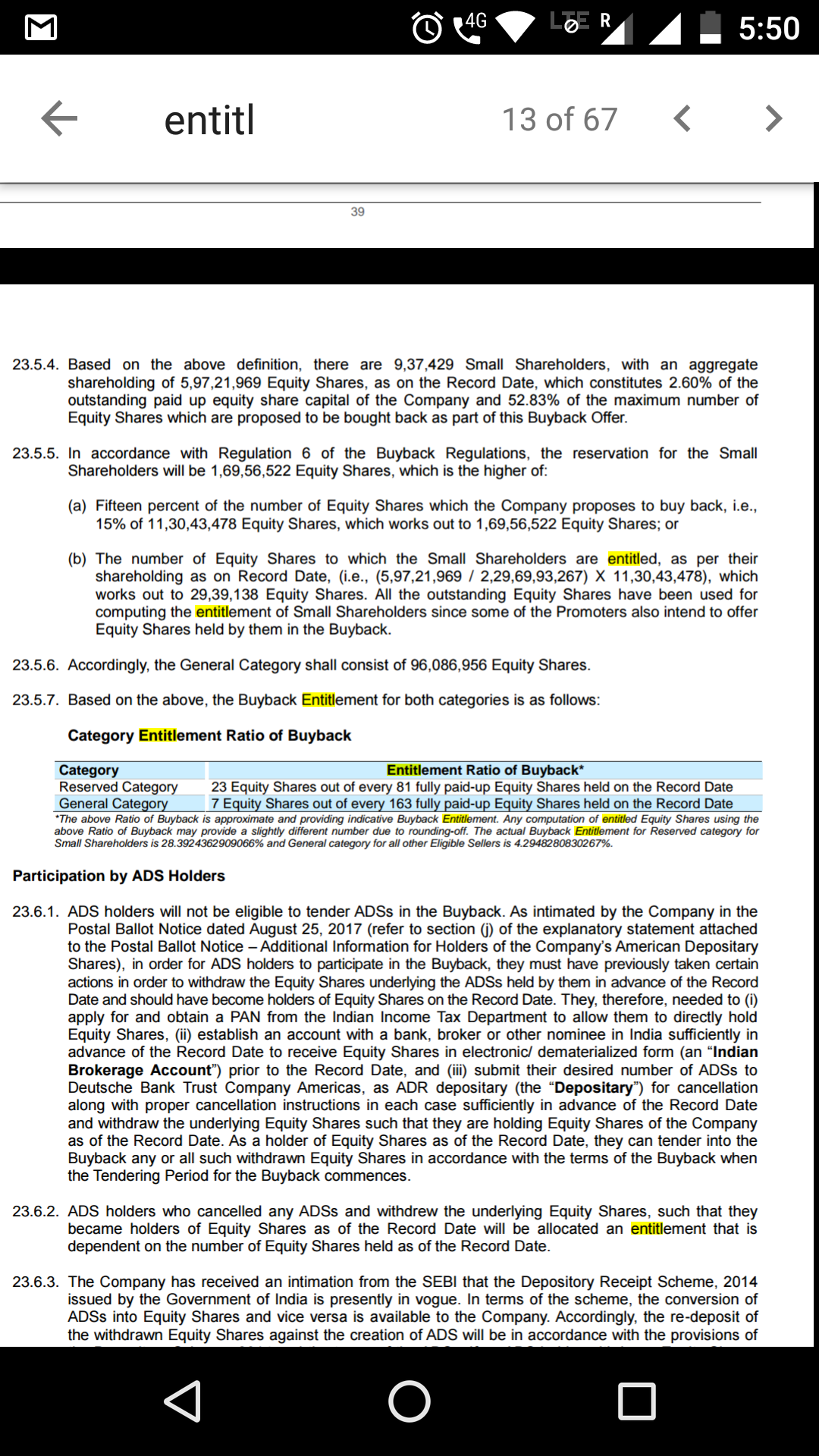

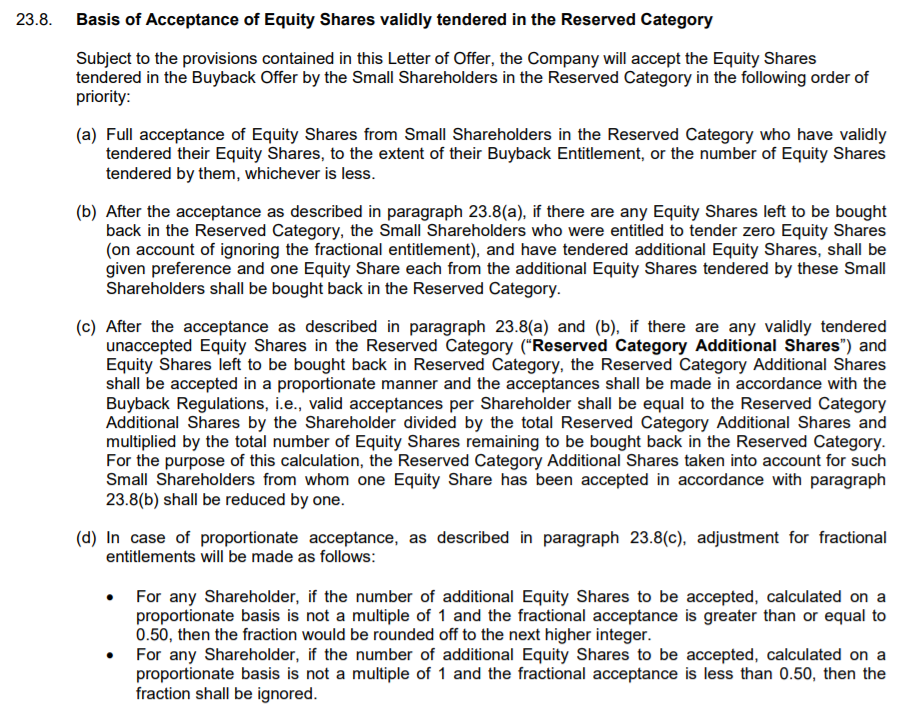

Is it ok to fill in more than alloted number of shares for buyback? Ef. If i hold 100 shares and 28 are alloted, what ahppems if I fill in 100 for buyback? Hypothetically, In case response is poor, will all my shares get tendered?

You can mention all shares that you wish to tender irrespective of eligibility. But make sure the quantity was held before record date. Else your entire application will get rejected.

Infy latest results.

Guidance marginally reduced.

Not very forthcoming on the decision to sell off Panaya acquired by prior regime and taken an impairment.

AI (Artificial Intelligence) finds just one mention as a sub-set of digital.

Capital allocation policy is shareholder friendly. The company is expecting to return 2 Billion from Cash on the Balance sheet plus 70% of the new free cash flow generated.

Anyone following the tech sector and/or Infy please comment on the future strategy

Infosys seems attractive with PE of 16. I dont expect share to grow much for next 1-2 years as company will be investing on reskilling the employees. Infact earning might go down for a while during this period. But it will grow in the long period. Need expert thoughts on outlook of infosys.

Looking at Cognizant and TCS valuation, Infosys appears very cheap. Should be a good buy around 1100. Tail wind of rupees depreciation will also help.

One of the reasons of P/E at 16, could be that, there was Tax Write back in Q2 or Q3.

Earnings look higher this year due to this and also partially due to share buy back during last year.

It certainly looks fairly valued as compared to TCS, and Few others.

I believe that, they are moving back to IT services model with some thrust on Digital Revenue generations from new technologies and areas.

Overall, recent run up in CMP from 900 to 1150, seems to have happened due to some of the above reasons.

One may expect decent returns from these levels, as compared to TCS and Few others which look partially overvalued.

Disc: Holding Infosys since over 3+ years.

Hi,

This is regarding Bonus shares issued by Infosys as of record date 05-09-2018. (1:1 bonus issue).

ICICI Direct demat account is showing less no. of bonus shares issued on 11-09-2018.

Trading permission message was delivered on 11-09-2018.

There is a shortfall of XX shares on Portfolio-> Equity page, and shortfall of YY shares in Demat Balance Allocated Quantity page.

Has anyone faced problem in bonus shares issued by Infosys on 11-09-2018.

I am checking with ICICI Direct, but this is first time, that I have faced such problem with my Demat account.

If any one has done some checking already in case of such a problem, it would be good to know.

Thanks.

Disc : Holding Infosys for over 3.5 years.

Infosys is so well tracked company that guidance, estimate and actuals seem to always converge. I am not adept in valuation, however I depend on online free tools, calculators and excels. Net profit grew by 14%, margins above 20, multiple large deals pipeline, digital service growing at 30%, is available at 15 to 16 PE. Sensex PE itself is 25! Also it generates Free cash plus has 60k cr cash balance. Mr. Parekh is also open for inorganic growth esp in New tech domain.

I have increased my position after 10% fall from my initial position, basis my above analysis.

Would like to have views on why market is not very bullish on infosys… Is it slow growth, automation taking away manpower cost advantage, Trump stance or a combination of these plus something else.

Calculation of future value & ROI for Infy.

One of the best large cap buys at this point. But you want to keep your expectations low as re rating is something which is unpredictable.

Except for PE expansion rest of the assumptions are ok .

You can expect near Capital appreciation of 10% CAGR for this stock + near 3% dividend yield … which is good by any standards

For a business that is growing at 10%, its difficult to ascribe a PE expansion or ascribe esp. a PE of 25.

The stock at least at this point (and until the management change their narrative and approach to growth - which should include large inorganic expansions - now with over $8 Bn in cash) will largely be traded on a div yield perspective.

However, a combination of buy-backs, inorganic expansion etc, should accelerate growth and improve ROI.

You have hit the point. Reskilling in AI, digital tech and smart acquisition is the only way forward. Also typical TCS, Infy type companies are not diversified like say a Reliance, Birla… This prohibits them in properly utilising cash in growth areas… I am sure the CXO of infosys know this… But when, what etc… We can hope but can’t forecast.

I feel tempted to load up on Infy, given attractive valuation esp when most quality stocks are so expensive… But then again risk reward is still not clear…

For a large cap It seems logical to pay a PE that is equal to it’s EPS growth. If one is willing to pay a higher price, then there must be a concrete reason. There isn’t one in Infy. Infy has shown negligible growth in EPS since last year, due to which it’s share price may lead the fall in IT.

On the other hand TCS has done better.

What will you pay for zero growth company, with 25% RoE. Zero?