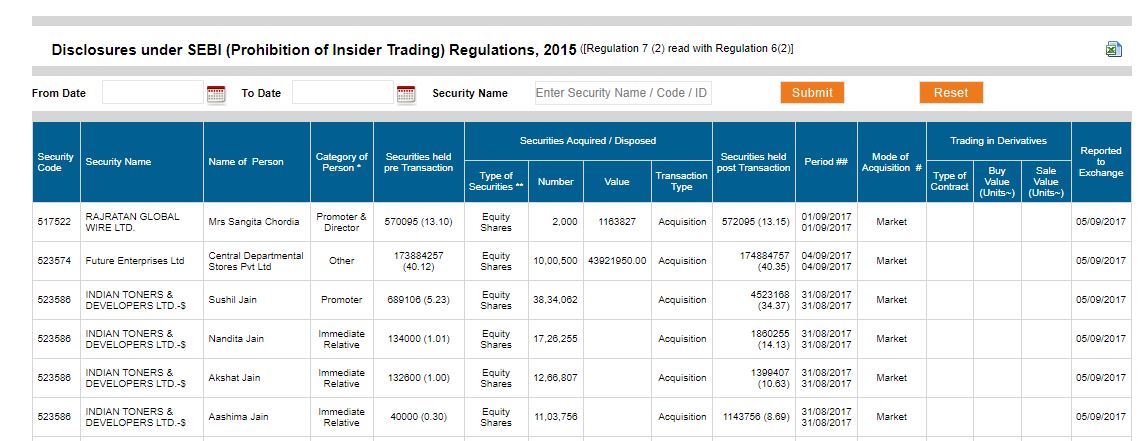

Today Promoters bought in bulk from Market. In my conservative estimate, worth 233 crs.

4 Likes

How odd! I can’t believe this happened almost immediately prior to the earnings announcement. I guess this means that Q2 was good.

EDIT: Also, how did you arrive at the Rs. 233Cr estimate? The market cap of the company is only ~Rs.400Cr. Assuming the 5th column is the number of shares bought, we have (Rs.297/share * (689,106+134,000+132,600+40,000) = Rs.295,812,000) ~ Rs. 30Cr.

1 Like

Sorry for the valuation mistake.

OK, so the correct increase in promoter shareholding is in the 7th column : 2,000+100,500+3,834,062+1,726,255+1,266,807+1,103,756 = 8,033,443.

This means you are correct in that Rs. 233Cr was bought by the promoters…But then how is it possible that the promoters bought 50% of the company on Aug 31, 2017? The BSE reports that the free float market cap is just Rs. 120Cr.

Yes I am thoroughly confused. Is something emerging because of amalgamation ?

That’s what I think. I just read the insider trading disclosures and it seems like what the promoters held in ITDL indirectly through the various parent companies they now hold directly.

I don’t know why the type of transaction listed in the table is “market” when this seems to be just a transfer of shares.

The BSE turnover data shows just 4153 shares traded on 31st August. In fact, on most of the days the trading volume is in just a few thousand shares. So this is does not seem to be a ‘market’ purchase. Something is wrong somewhere.

Date Open Price High Price Low Price Close Price WAP No.of Shares No. of Trades Total Turnover (Rs.)31-Aug-17 298.00 298.00 290.00 294.95 292.78 4,153 103 1,215,926.00

The Co. will be considering an interim dividend at the board meeting on November 27, called to consider the September qtr. results. This will be a maiden dividend from the co. after more than perhaps a decade & a half of existence. This could be an inflection point for the Co. looking for market cap, coming as it does after the merger with the profitable subsidiary.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/c6151672-324a-4027-b014-416323ddea5e.pdf

6 Likes

i think they have done well to re-structure their organisation. But sales especially from fully owner US subsidiary have been soft. Any inputs on that @RajeevJ ?

ITDL has seen a huge run up in last few years. At this level i am happy to take some profits of the table. SP Tulsian has been giving lofty targets for the last few years. He is still talking about 400 plus so again the mkt may give it to him.

Can somebody please tell me why the PE ratios for Indian Toners is 30 on screener.in and 42 on valuersearchonline.com?

From what I calculated with FY17 results, the PE prior to the amalgamation is 17.69 and after the amalgamation PE is 18.14.

No. of shares increased by ~50 lacs, all of which were allotted to promoters. If you have noticed, mcap went up to ~400 crs from ~240 crs prior to amalgamation, keeping share price hovering around 300.

Disclosure- was invested but sold all of holding after realizing what is happening (perils of being a newbie investor)

Thanks but my questions was dealing more with the nitty-gritty of the pre/post merger effects on the earnings (and also extended to book value):

Pre-merger consolidated results of ITDL for FY2017:

BV: 96.35Cr

Earnings (subtracting minority interest): 13.56Cr

Shares outstanding: 0.8Cr

BV/Share: 120.43

EPS: 16.95

Post-merger consolidated results of ITDL for FY2017:

BV: 134.1Cr (including the previously subtracted minority interest, i believe share capital might also increase? but I think this should be negligible)

Earnings: 21.68Cr

Shares outstanding: 1.316Cr

BV/share: 102

EPS: 16.54

Now assuming the current price of ~Rs.300/share (I’m approximating any share price after the run up),

we have:

Post market cap: 300*1.316 = Rs.394Cr

Post PE: 300/16.54 = 18.13

Post PB: 2.94

I am basically asking if these calculations are correct, and that my my hypothesis that this reverse merger was EPS neutral is true.

I believe screener.in arrived at a PE=30 by dividing the Post Market Cap by the Pre Earnings - 394Cr/13.56Cr. I don’t think this is correct as it does not make sense on a per share basis.

I have no idea what valueresearchonline.com did.

1 Like

Impressive set of Q2 numbers:

Revenue increased 14% YoY and 45.88% QoQ.

Net Profit Jumped 34% YoY and 111% QoQ.

Net profit margin expands to 23.81% from 20.23% YoY.

Interim dividend of Rs. 1.5 per share declared.

Disclosure: Invested

1 Like

Are we doing apples to apples comparison since the amalgamation of the subsidiary and share capital for both the period are different ?

1.50 dividend looks less to me. my expectation was more.

do we have any concall or presentation from the management for the results ?

Hi, your calculation is perfect.

I spoke to the management regarding the high PE multiple displayed on website. We sat dow and calculated a PE of approx 18 post amalgamation.

I have substantially increased my holding here despite my earlier message. Indian toner has a long way to go. The stock should double from here to catch up with industry PE.

Disc: added new holdings in 300-330 range

1 Like

Hi Rajeev, can you please expand on ‘looking for market cap’?

Rewarding shareholders is a good way to build market cap.

Do you think they are looking to build it up the valuation and exit?

Any active trackers? How were Q3 numbers?

The revenue growth was 8% with profit 33%. But bulk of profit was due to tax deferment.

Revenue Growth is muted, possibly because US subsidiary not getting traction it should.

However with 10% of cash compared to mcap and 70% promoter holding with latest restructuring it continues to be good bet.

Disl: Invested.

1 Like