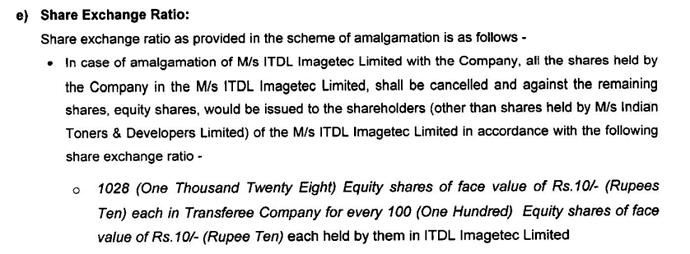

No, as per my understanding the shares of Indian Toners will get cancelled. So those 5,10,000 shares get nullified. See below

So essentially only the 4,90,000 shares get converted. Below is my calculation

No, as per my understanding the shares of Indian Toners will get cancelled. So those 5,10,000 shares get nullified. See below

So essentially only the 4,90,000 shares get converted. Below is my calculation

Thanks got it. I seem to have missed the most important part of the 51% being cancelled

Can anyone explain what is point in merging a subsidiary and floating another subsidiary at the same time?

The moot point is this fair to minority? Given the history and reputation of the promoters, one needs to tread with caution. While the multiple ascribed to the subsidiary looks OK, the dilution seems quite huge for the minority. Also were the shares not cancellled, the promoters would have owned ~ 64% v/s 69% that they will now currently own. Anyone who has any view on this.

No expert again. But i guess we will have to wait for their moves post amalgamation and recapitalization. In my opinion, as it stands now the company is signaling to the outside world that its EV is at least 337 crores. If the market fully captures the valuation gap it would be good for the shareholders - minority or otherwise

Expected Cash from Ops =26cr i.e ( 23 cr /Operating Profit/ + 3 cr /dep/ - negligible Wcap changes)

Interest cover = 3

Interest it can comfortably service = 8.7cr ( 26/3)

Cash & Investments(asper 2017 results) = 73cr

Implied Debt capacity =160 cr [ 87cr ( 8.7/10%) + 73cr ]

Expected market cap at current levels = 250 ( cr )

EV = 337cr = (250+160-73)

Expected market cap 250cr ?

Wil be helpful if u can explain the calculation of 250cr

Hi Sumit

Refer to rohits calculations.

Best

Bheeshma

Hi one small doubt

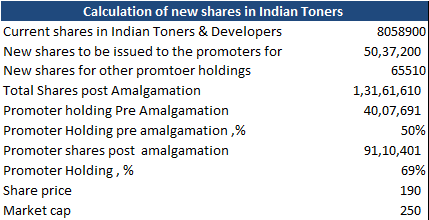

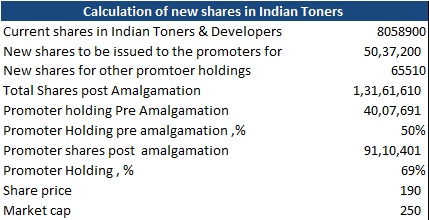

Total shares after merger*cmp -250 cr market cap

But earnings will also get divided by total shares outstanding after merger so is it correct to directly multiply it with cmp?

can u please share the source of info regarding the floating another subsidiary??

Please check post by kums17 in this thread on Feb 5. He has pasted a quote from the AR.

Sorry, didn’t understand this. Can you explain ?

To arrive at market cap of 250 cr , u have multiplied total shares outstanding after merger with CMP. But earnings will get diluted due to increase in number of shares outstanding.

My question is that how can change in number of shares outstanding change the earning power of the company?

From bussiness point of view der is no real change in earning power of the company.

Take the PAT before Minority and divide by the number of new shares… Compare this EPS with the current consolidated EPS. There shouldn’t be much change. I think ~ 2% kind of change in EPS.

Hi Sumit

Net Profit before minority = 2168.31 lacs

Total number of shares post amal = 1,31,61,610

EPS after amalgamtion = 16.47/share

Current EPS pre amal = 16.84/share

Best

Bheeshma

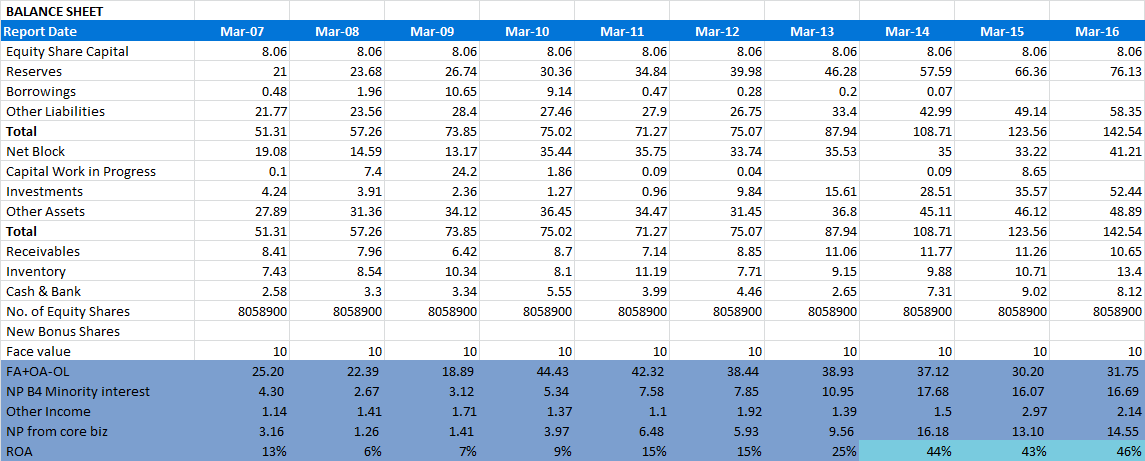

1.ROA from core bussiness is approx 43% of last three years so y this biz is not attracting competition…means what is the competitive advantage like low cost producer, brand, large distribution n/w,etc

2.Large amt invested in mutual funds - gives message it doesnt have reinvestment opportunitites…means i questioned myself y doesnt it buyback its shares or give div to SH.

Hi Sumit,

this is the main negative of the company. Promoters are not passing the profit share to minority share holders. If you see the latest results also 20 rupees dividend has been paid to subsidiary share holders (ITDL Imagetec). Now after this amalgamation, i hope this will stop.

Regards,

Neelavi

While reading annual report 2015-2016, I have noticed - ITDL has disclosed Independent Director –Mr. Sanjeev Goel, he is the director of subsidiary company ITDL Imagetec Ltd. As per Companies Act 2013, Independent Director should not have any relation with the company or it’s Subsidiary company which means the company is not following Corporate Governance.

As per Annual Report 2015-2016 pg no. 36 :

NCLT has accepted the amalgamation, ITDL has informed the BSE, does that mean amalgamation is finished or is there anything still pending.

Indian Toners hits upper circuit today.

The amalgamation which has been approved will lead to cleaner corporate structure. I hope they will start paying dividend to the merged as well which will boost investor confidence.

The GST rate is 18% for printer toners (please correct me if i am wrong).

Since ITIL is pan India player, GST rollout should help. From being undervalued this stock will now be fairly valued.

Disclosure: Invested

CRISIL has upgraded the outlook from stable to positive. I think BBB+ is the rating upper cap for companies of this size. At group level, total cash and equivalents stand at 73 crs and PAT for FY’17 was 22 crs. Excluding cash, trailing PE is 7.7 for merged entity. If I am not mistaking, today is the day of final hearing for scheme of amalgamation.