Any news about what happened in the shareholder’s meeting today regarding merger with CapF?

IDFC Bank shareholders give approval for merger with Capital First

1 Like

In a interview on etnow vaidya explains why the merger is beneficial for booth the interested parties

Good days ahead for the merged entities

1 Like

When are Capital first shareholders going in for voting for the merger?

Would the shooting down of it’s bigger/ higher ranked competitors like Axis and Yes by RBI help IDFC Bank garner higher market share or at least attract more investor attention? I think so. If IDFCBank is late in joining the party then these two established competitors are going to be in disarray due to absence of clear leadership and lose some time if not the entire growth story. Would like to know what other investors think. I am buying IDFCBank on every dip the stock offers. thanks,

Copying the questions I posted on Capital-First thread, as there seems to be a different group active on this thread. Mods, please delete/merge as you see fit.

-

Since the swap ratio is 139:10, what happens if I have only 1 share of CapitalFirst? Mathematically, I should get 13.9 shares of IDFC Bank, but how do they account for fractional holding of 0.9 ?

-

Price has corrected by almost 50% from highs. Can some with technical analysis skills look at the chart of either CapFirst or IDFC Bank and share if there is scope for further correction ? Or the cleanup is done and things can only get better from here (hopefully) ?

-

Given that most NBFC’s are getting thrashed due to questions on incremental capital availability/cost of capital, CapitalFirst’s merger with IDFC Bank gives it access to low cost CASA deposits. In that sense, it may be better off than many pure-play NBFC’s - in a small way atleast. Is this a valid argument?

-

When is the merger expected to be consummated? Can someone throw light on the expected EPS, Book Value for IDFC Bank post-merger ? Along with calculation logic if possible.

- Yes, as i understand, banks have access to cblo, repo borrowings in money market which nbfcs do not have. Iirc, idfc-banks q1 overall borrowing cost is 7.2-7.3% ( This is including the high interest infra bonds due to mature in 2-3 years which constitute large part of the borrowing at present ) which is 150 bps lower than capf.

Combined BV is 38/- as of q1. You can expect capf to de-list from around 15th dec. And receive idfcbank shares in Jan 1st or 2nd week.

2 Likes

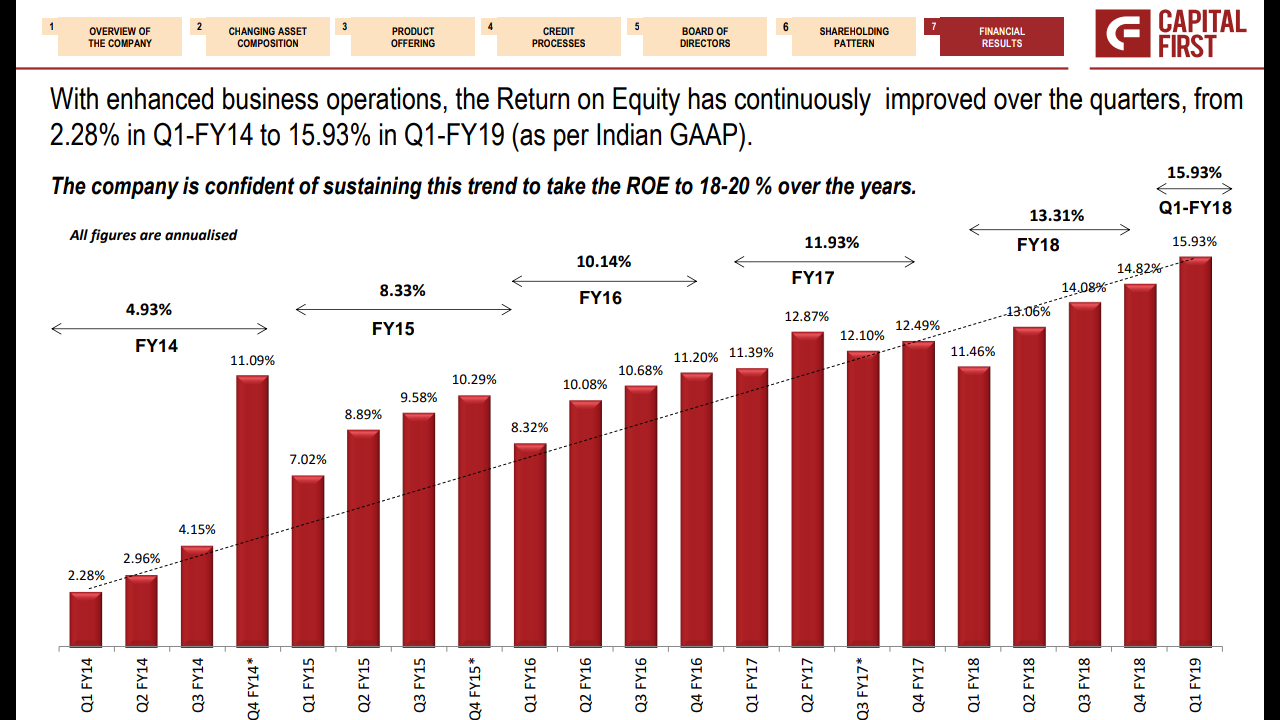

A screenshot from capf q1 fy19 presentation showing how the RoEs have grown in last 5 years… (Although in a low interest rate scenario)… Remains to be seen whether this can be replicated for the merged entity.

Hi Vaibhav. What’s your opinion on the MSME exposure of Capital First? Is that risk going to materialize in a rising rate environment? Even though stock has corrected almost 50% from highs and most of it might be priced in.

I hear that they have passed on interest hike to 50% of the book. Going forward, merger with bank should help in reducing cost of funds. The book held well during gst roll-out and demon which are positive signs. But one has to be watchful all the time.

1 Like

Lowest cost funds for banks is CASA and I fail to see a game plan to increase the liability side of the franchise once it’s merged with IDFC. Sure Mr. Vaidya will bring in his experience of good underwriting practice and increasing the SME and retail lending, but what I don’t understand is what will he do differently than current IDFC management to attract retail customers to deposit. Something which even the established pvt banks struggle at times.

1 Like

7 million capf customers (some would open idfc bank accounts), more branches, higher interest on savings (my guess, 6% or higher), new partnerships (such as with zerodha) etc…i think building casa would take time.

They have already got kiosks everywhere, helping to attract crowds…

Building a CASA franchise requires a lot of effort & also experience. To get a customer to keep money in CASA, the whole payments apparatus has to be built including bill/utility payments etc.

As an example IDFC Bank has tied up with Zerodha, to build a seamless account like ICICI Direct, wherein the customer keeps some portion of the money he wishes to deploy in MFs and Equity Share purchase. This is a Win-Win for both, given that Zerodha is crumbling under the weight of operations right now.

In essence it involves building the plumbing/works for the flow of various types of payments through a CASA account.

IDFC Bank has been building the plumbing so far, hopefully Vaidyanathan will take the infrastructure and quickly scale it up. I think the liabilities target is not a lot, given the size of book of Capital First.

It will be naive to assume that most banks have built in the infrastructure/plumbing for CASA. ICICI Direct has been a very successful product (although at a decline stage of product lifecycle). How many banks have been able to successfully imitate that.

1 Like

Q2 results are out:

On that face of it looks pretty poor

The 600 cr provision is finally done - hopefully no more bad loans / provisioning remain

However, my issue is the stagnation / fall in the revenues… with the increasing cost, there is a significant loss… my worry is that the growth May have plateaued and probably only the change in the management can reboot the growth…

Was planning to invest after a correction after this result (merger will take place between q2 and q3 result) as the provisioning / write offs would have been done now… however considering the market condition may wait for a bit longer to check what actions the new management will take to get back on the growth

Lets wait for the concall to see how Mr Lall spins his story this time…

Disc : invested and looking to increase stake at opportune time

Of the total provisions of nearly Rs 601.38 crore in second quarter, provision of Rs 344.48 crore is due to reclassification as per regulatory provisioning norms, Rs 197.13 crore is provision against investments including mark to market provisions in accordance with RBI guidelines, the bank said.

NPAs are reduced (nnpa 0.59%,gnpa 1.63%) which is good to see. Operating performance has been bad(high other expenses qoq) … Can it be partially put down to old management having no incentive… As they would be leaving in a month and handing over the keys to Mr. Vaidyanathan?

Disclosure : invested and looking to add further.

Q2 investor presentation -

Again posting Mr. Vaidyanathan’s interview which would be taken as how the new management assesses growth road-map for the future -

Whats in a name ? Not sure of the value add, except for adding to painting charges in all the branches and other retail outlets.

3 Likes

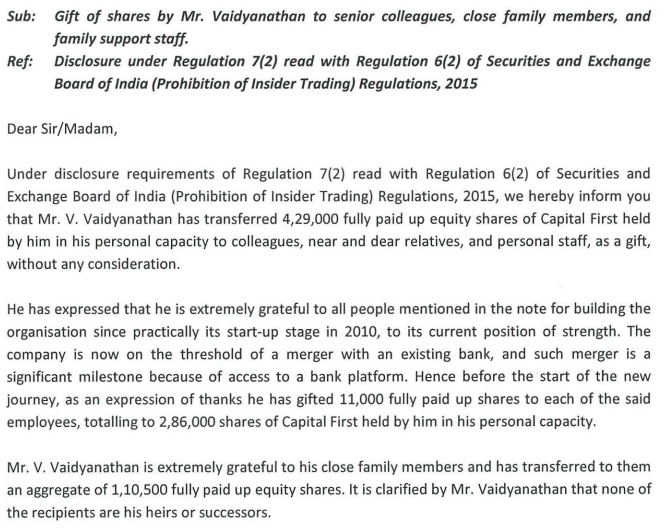

Mr. V. Vaidyanathan has proposed to board to share almost 10% of his personal holding in CF with senior colleagues, close family members, and family support staff. Shows the self-less character of the leader who is truly passionate about building an eternal organization by moving to banking platform and not after any monetary gains. He has not only shared his wealth with existing colleagues but also with former colleagues. This will just increase the loyalty and respect from the people that work closely with him. And as we know that loyalty goes long way in maintaining culture for an eternal organization. A special leader on the verge of doing super special things.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/790a2f27-6900-4dd2-9469-34a3066fb713.pdf

Disc: invested in CF and accumulating in SIP mode. Views may be biased.

2 Likes