Indian Embedded Value is the main matrix used to analyze Life insurance company, which they do not publish every quarter.

Their stated position is we will publish IEV half-yearly in-line with best industry practices. Their competitors do it every quarter. I really do not know what best industry practices this group follow. Top management in all the organizations of the group seem to follow most opaque and crooked policy in name of transparency and corporate governance.

It is difficult to analyze the company given management choose not publish IEV for reasons best know to them.

It is difficult to analyse the performance of the insurance companies as the embedded value is a function of many assumptions…however we can always compare the performance of HDFC life and ICICI pru and use them as bench marks…

HDFC life is way better than icici life in terms of performance but HDFC is almost 2.5 times costlier on the basis of price to EV…other way of looking at it is that ICICI pru is undervalued…

HDFC will command that premium due to their excellent mgt and unique initiatives but we need to define that premium…for my calculation purpose i am keeping a 40% premium for HDFC life over icici life…so with HDFC life as a benchmark which has a PEV ratio of minimum 6-6.25, the ICICI should have a PEV of 3.75…to reach that PEV, the ICICI share should be valued at Rs. 491…

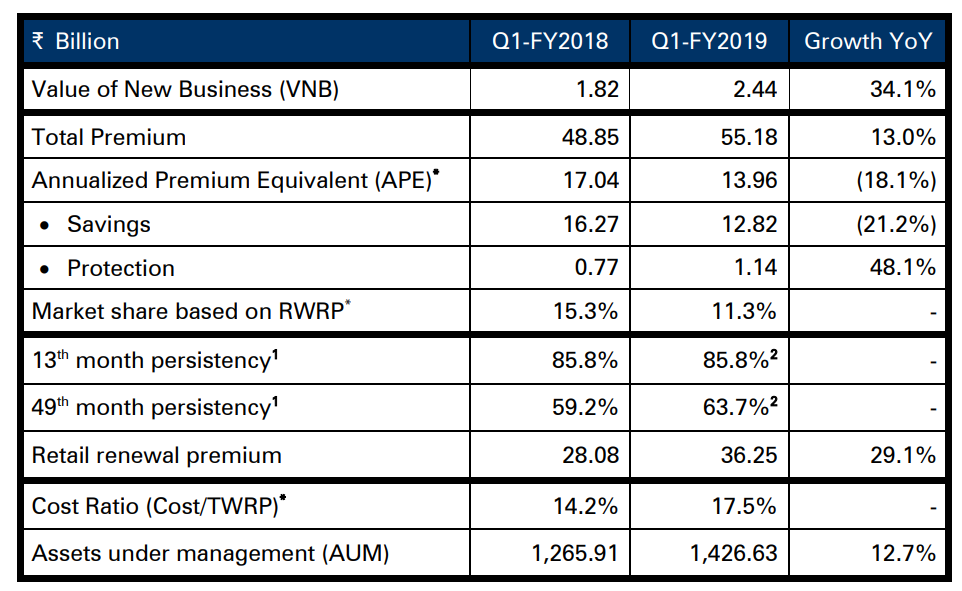

There was de-growth in APE for the Q1 FY19. The management claimed that de-growth was due to high base in Q1 FY18 & equity market performance. The de-growth was much lesser in the month of June. The protection APE continued to grow which has aided in growth of VNB.

The renewal premium growth came in at 29%, which I find to be very good.

There was marked improvement in the 49th month persistency & that also I find to be very good.

As % of protection business grows, the cost ratios will continue to inch up.

The VNB margin increased by 100bps to 17.5% compared to March’18 due to higher protection buinsess share & lower APE. Let’s see if they can maintain/improve VNB margins through the year.

Overall I find results to be satisfactory. Insurers start making money from 2nd, 3rd years of their business due to high cost of acquisition. The growth in renewal premium & 5th year persistency numbers are very good in that direction.

The company is focused on growing VNB & VNB margin through up-scaling protection side of the business. This direction will bring product mix closer to competitors like HDFC Life or Max Life & hopefully VNB margins will also be closer to them over time.

In the short term (FY19), if company can stem the de-growth in savings side of business & continue to grow protection side of business at this rate, we might see healthy VNB growth (50%+) by the end of the year.

On the question of EV development, one can assume the unwind of 7-10% and add VNB of the current year to get approximate estimate of EV for next year.

Disc - The stock forms > 5% of my portfolio and no transactions in last 90 days. This is not a buy/sell recommendation & investors are advised to do their own due diligence. I am not a SEBI registered analyst.

This should be cause of concern for investors. We don’t even have one matrix to compare life insurance companies!

I would argue that assumption which affect the valuation of Life insurance companies should be decided by regulator. Also they should be disclosed more readily by companies.

Can someone please explain as to why did ICICI Pru go after the ULIP market in such an aggressive manner, given the cyclicality in this segment and very lower margins? What are the advantages of being in this business apart from the growth that was witnessed in the last few years in this segment?

Uploading the H1 investor presentation for reference. Slide 22, VNB drivers (4P’s concept is pretty interesting - Premium Growth (APE), Protection Premium Growth, Persistency and Productivity) is an interesting read!.

Q4 FY20 was quite eventful quarter for the life insurance sector. Few changes worth mentioning -

Budget proposed an option of availing lower personal income tax rates if 80c and other exemptions are not availed.

In my opinion, this causes fundamental disruption in insurance industry as ~40% of the sales happen in Q4 FY20. Whether this really impacts the growth of insurance companies needs to be observed but this causes uncertainty. Further, if one takes long term view of budget making processes, it is quite probable that old system might be completely done away with.

Budget also abolished the dividend distribution tax (DDT) and dividends are now taxed in the hands of recipients. The impact on insurance companies depends on dividend inflow vs. dividend outflow. If outflow is less than inflow, insurance company will end up paying more taxes.

Above two changes, along with rapidly falling equity markets, falling interest rates and COVID-19 provides quite a lot of headwinds to insurance sector IMO.

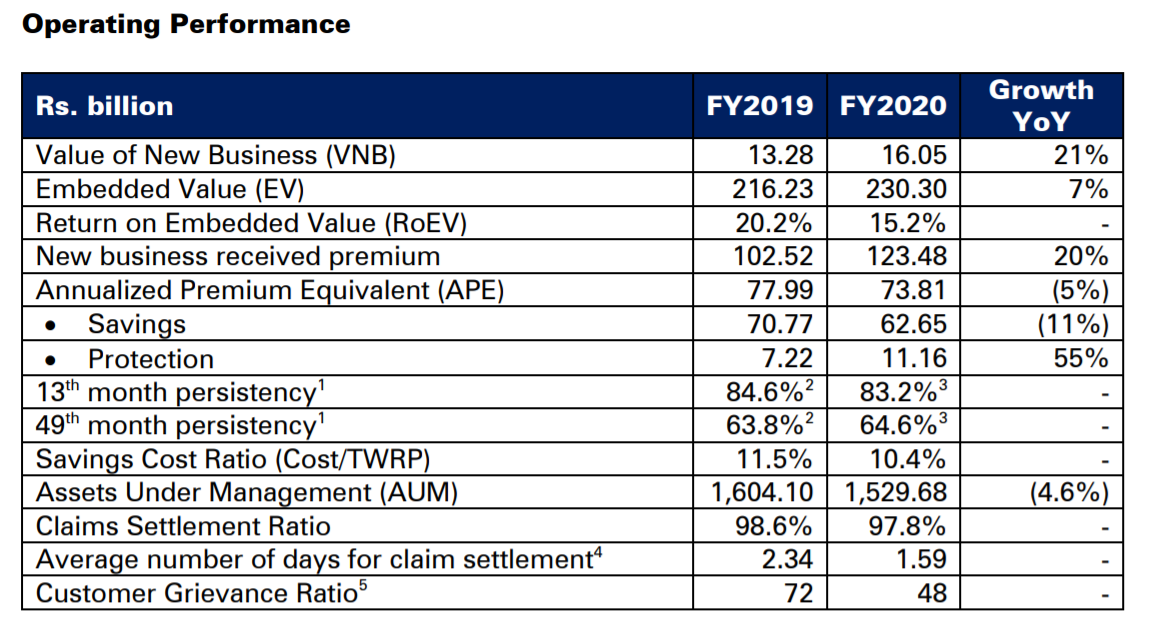

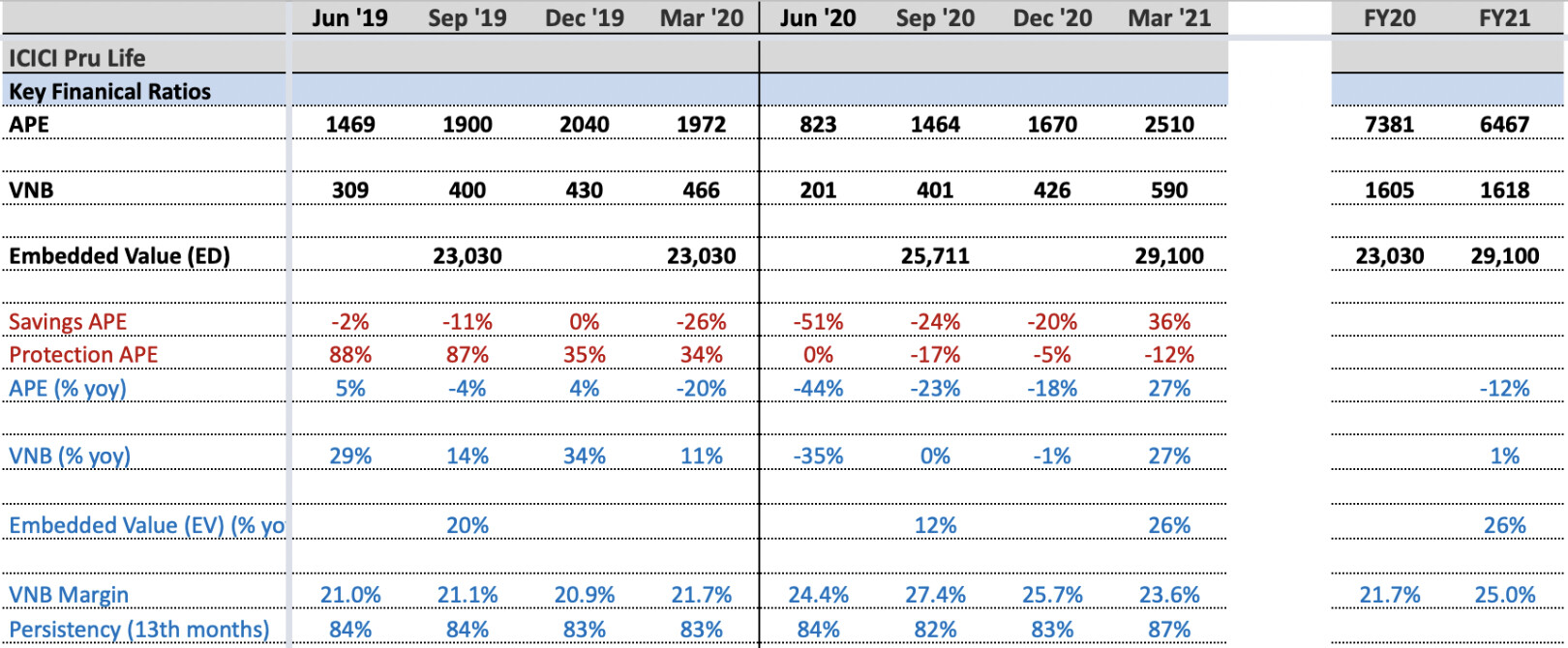

The company had good growth of 21% in VNB in FY20 but EV growth was only 7%. The growth in VNB was led by increasing share of protection and savings business.

The reduced growth in EV was led by two factors - first, lower unwind caused by lower interest rates. Second, -ve economic and investment variance. This was largely caused by sharp fall in equity markets. That resulted in reduced AUM and hence reduced corresponding fees.

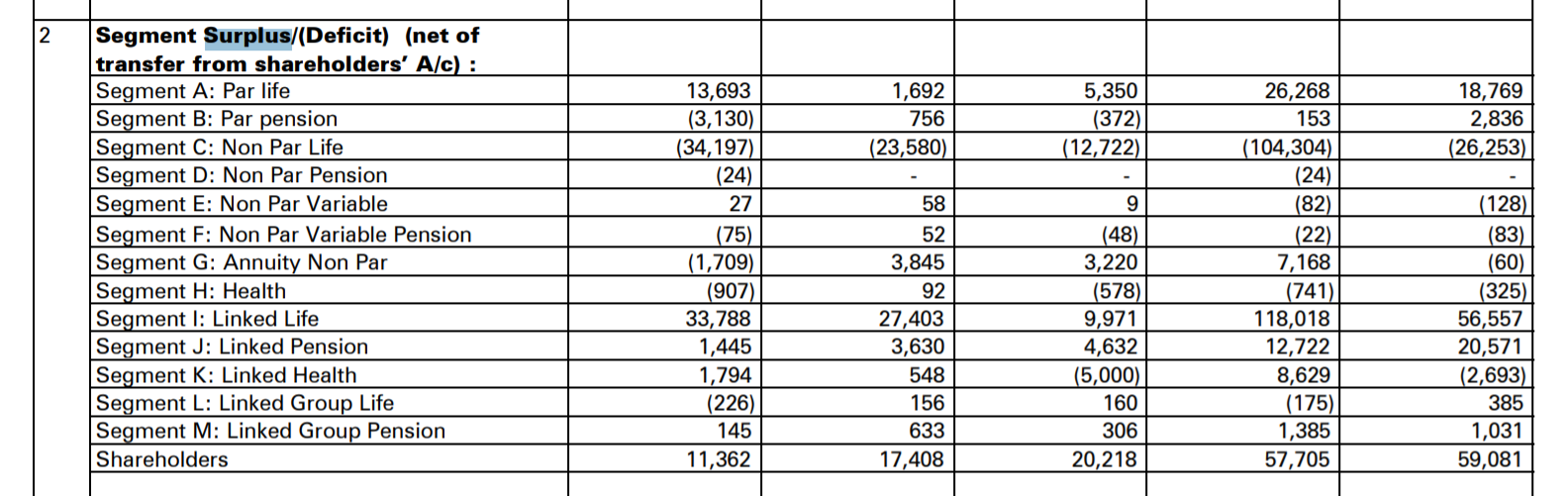

The growth in protection business results in a lot new business margin strain. This can be seen in two parameters - 1) solvency ratio going down from 215% to 194% 2) split of surplus across different product segments as shown below.

There was a deficit of 1043cr in Non Par Life segment in FY20 as business grew. Protection business has very high VNB margins but very high acquisition costs and smaller ticket sizes. This is precisely the reason PE ratio is not a right metric to use for insurance business.

Further, profitability in the protection product is built on the basis of persistency. If persistency falls, the companies will see a lot losses.

Due to strong growth in protection across insurers, reinsurance rates went up in the market. These rates would be passed on to end customers leading to rise in premiums. Further, falling interest rates shall result in larger premiums to be paid for new business protection. I-Pru is looking to maintain VNB margins in percentage terms even with this price hike. If they manage to grow premiums in protection, one should see very strong growth in absolute VNB. Whether premiums will grow in current environment of COVID and other economic problems is very hard to figure out.

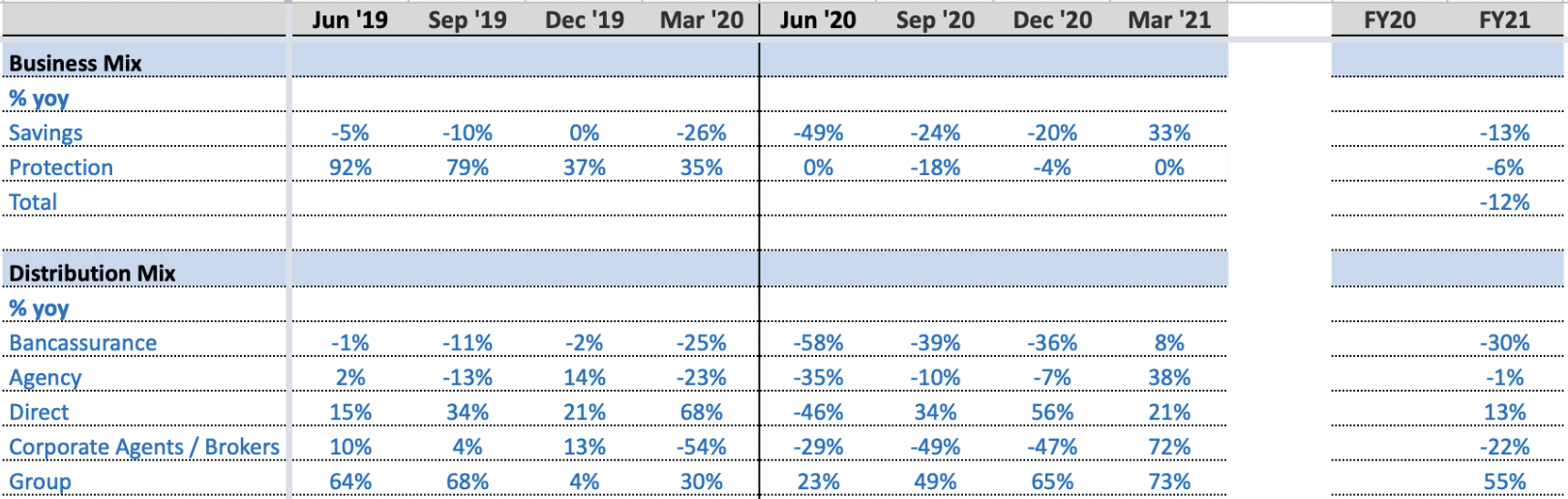

One thing was very clear in both HDFC Life/I-Pru is ULIP is not the flavor of the season and both of them continue to see weakness in that part. Whether similar weakness will be seen in MF as well or whether there will be fund flows to MF is again very hard to predict.

Limited Pay Protection Plans - In these plans, one still get mortality coverage for 20-30-35 years but one can pay higher premiums for 7-8 years. The company designs the products in such a way that - absolute VNB across the policy tenure remains the same. Due to this, VNB margins are lower for limited pay products due to higher premiums in denominator.

The company had zero NPA since inception and has no exposure to troubled names in current environment.

ICICI bank contributed 47% of the total APE and total contribution of the Banca channel was 51%.

Another simple point I wanted to bring out was investment risk in rapidly falling interest rate scenario.

For regular paying term plan with sum assured of 1cr, if one does a simple linear reverse discounting at 4%, you will get premium x. This assumes that - for every year that company receives premium, it can invest at least at 4% return to meet required obligations. What if you can not find the instrument that provides 4% return?

Disc - Sold off position in HDFC Life post budget. No investments in any life insurance company. This is not a buy/sell recommendation. I am not a SEBI registered advisor. Please do your own due diligence.

ICICI Prudential has taken an acquisition of 5% in Westlife Development Ltd (McDonalds franchisee in India).

What is the impact/rationale of this investment? Is this just a long term investment of the company’s float?

Disclosure: Not invested. Researching this company.

VNB %: up from 21.7% in FY20 to 25.1% in FY21 (driven by share of non-linked business increasing to 36% from 20%)

Outlook

Growth to pick up: given the substantial product & distribution diversification is now behind us … ICICI Pru Life has corrected the high dependence on ULIPs and ICICI Bk, and with this impact now in the base, growth momentum should pick up going forward

Going through the videos posted on this channel one can see most of the cases involve misselling by ICICI Bank and ICICI Pru Life, is it a coincidence or it is the actual ground reality?

Also, is this an industry-wide trend?

Want to invest, studying the company.

Can anyone please explain why hdfc life is so richly valued to compared to icici prudential. IEV for both are comparable…prudential is 3x IEV and hdfc life is 5xIEV. What is the market looking at? Any pointers? Thanks!!