Unbelievable Can’t imagine you selling Shilpa and all the other beautiful Pharma stocks (I think I am in love with pharma sector .

But this shows the ruthlessness of a true professional. Act rationally with logic, not with heart.

Hiteshbhai, what are your views on the market for the near term? Do you think the market has made some intermediate top and likely to move southwards? Is that the reason you are readjusting the portfolio / moving to cash ??

Pls answer the same if you feel comfortable.

Rgds.

Its very difficult to predict markets atleast in the short term. I have been cautiously bullish since a long time. But my current shift from pharma has not got too much to do with market levels.

Some things did not add up for me in my invesetments in torrent and alembic. Both did not react to far better than expected quarters during the abilify opportunity. Plus I was uncomfortable with the kind of capex that was going on in a lot of pharma companies. It was almost as if most companies had loads of cash flow and wanted to blow it off in capexes. And now as usually happens after huge capex in specific sector, demand begins to face headwinds for one or the other reason. Without people realising it, the leaders have corrected equal or more than 50% from their tops. While people may consider this as a bottom fishing opportunity, I would like to see for some more time how things pan out.

There has been a fair bit of price erosion in US markets and according to Sun Pharma boss, it appears to be the new norms. This should affect margins and returns which could lead to de rating of the whole sector. Thats probably what we have been seeing in the ongoing correction in the stock prices of pharma companies.

Another thing is that a sector which has had a superb bull run since 2008-09 till 2016 which is almost 7=8 years undergoes correction I think the time correction element also needs to be taken into account. There has to be sufficient consolidation post this correction before the sector picks up investor fancy. For a clear example one can see how real estate sector suffered and for how long before the current comeback.

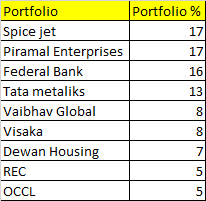

Could you please review my below portfolio. So far portfolio has given me 60% return in last 1.5 yrs and please let me know where i need to improve in terms of stocks or allocation. Some stocks like federal bank, Tata metaliks, vaibhah global have been added in last qtr.

I am a very avid reader of your posts and totally appreciate your candid and transparent views. I am very curious, as I am sure others are, to know the sector(s) where the allocation has moved to since you have moved out of pharma completely?

@trilok, I dont track cement sector too closely. But I had earlier done some trading in kcp ltd and again entered during recent correction. Its more of a techno funda bet for me.

@VivekSukumaran I have been more into agri sector stocks and some financials including nbfc added after moving out of pharma sector.

Hitesh, if you are comfortable, can you disclose new additions including investment thesis? It’s always a pleasure reading your thoughts and investment process. Look forward seeing more new company threads from you.

Thanks Amit

Hitesh bhai, since you mentioned that you have interest in Agrochem stocks, I would like to know your opinion on Sharda Cropchem. It is asset light business built around taking advantage of difficult registration process in western countries. It has good ROE but it is difficult to make assessment of future growth prospects. How do you approach business like this?

@Ankur_Lakhia more than growth , the authenticity that 100% of asset marked as intangible asset are not accounting gimmick .Specially considering employee profile at linked does not look so promising to create so much intangible asset. Sorry for my lack of understanding of business model .More damage has been done historically focusing on P&L and forgetting balance sheet

Hitesh Sir - An unusual question. Selling not investing.

Thanks to reading at Valuepickr, learnings from you and friends here and of course luck, I have done pretty well, better than many of MF Schemes, on a 3 & 1 year basis. However, from a investment strategy perspective, I am a novice.

I need your advice about selling 10-15% of my PF. Need some money to repay family debt.

In my PF; Repco, Granules, Cera, Symphony & PI have been laggards on a two year basis. What is your opinion on these? Which ones can be sold off? Do want to continue with winners. Please help.

@yatharth, Selling is always a difficult art to master. I myself havent been able to formulate a specific strategy on the selling aspect.

But since you want to sell part of your portfolio, the ideal thing would be to do some proportional selling in most of the stocks you own. Alternatively you could list your stocks based on your conviction and valuations and try to figure out which companies need to be trimmed in the PF.

About laggards, companies like Cera, Symphony and PI have demonstrated great growth in the past and are taking the breather which is usually a sideways correction till valuations catch up before the next upmove.

I had earlier owned sharda crop and exited. It has a very good asset light business model. Their strength is the registrations that they possess in various geographies which gives them some advantage over peers. But when I used to track it closely one big risk that I felt was there for the company was about forex. They buy in one geography and sell in another geography and if they suffer from currency fluctuations, then it can affect profits. Management in form of Mr Bubna comes across as a person who has immense knowledge in his field.

First of all I dont track the cos mentioned viz. wallfort and vardhman holdings.

About new additions to the portfolio, I have mentioned in various company threads about my holdings wherever possible as a part of standard disclosure . I wont be able to discuss individual companies.

Hi Hitesh Bhai,

I was NOT in bull mkt especially bull craze of 2006-08 so have no memories/feelings of how craze looks like

I don’t know about current valuations but I am puzzled at certain things like Dmart, CDSL, PNB Hosuing and some 7-8 examples like that.

Dmart: How can astute investor like Damani will sell DMART at ~70% discount to market[IPO Price: 300, Current Price: 930)

CDSL: BSE setting double price at IPO(double wrt previous dilution) and after that also price rising more than 100% from IPO price

PNB Housing: How can NBFC with ROE of 17% will get valuations of 50 PE ratio just because PAT have extraordinary growth … I mean at growth of 50% and ROE 17% soon they will hit CAR level & again have to dilute equity

Wrt bull market of 2000-2008, in which year bull craze has reached as per you experience(I guess we might be still away from 2008 craze)?

Trilok, the low float and the lock in period for the institutional ownership is the catalyst which is adding impetus to dmart,cdsl and Au finance…As far as pnb hsg is concerned it is clearly a sector leader with high growth and very low npa…also there is certain amount of predictability for it’s future earnings and hence commanding premium valuations…

- which other stock you like?

- which other stock you like?