HINDUSTAN ORGANIC CHEMICALS LIMITED(HOCL) is a PSU incorporated in 1960 under the Ministry of Chemicals & Fertilisers. It is the second largest producer of Phenol and Acetone in India.

It has two manufacturing units, viz. Rasayani Unit (total 14 plants for different chemical products located in this unit), which manufactures Aniline, Nitro-benzene, Formaldehyde and Nitrogen oxide. The Kochi Unit was set up for producing 40,000 TPA of Phenol , 24640 TPA of Acetone and Hydrogen Peroxide(5225 TPA later expanded to 14000 MTPA using de-bottlenecking) in 1987. one subsidiary unit, viz. Hindustan Fluorocarbons Limited, a plastic chemical and is situated in Medak District of Telangana.

Product portfolio : Nitrobenzene, Hydrogen, Aniline, Sulphuric acid, Oleums, Formaldehyde, Nitrotoluenes, Concentrated Nitric Acid, Nitrogen tetroxide, Caustic soda ,Lye, Chlorine, Phenol, Acetone and Hydrogen peroxide. Last 3 are from Kochi plant rest all from rasayani plant.

I am not going to discuss Rasayani plant as it was shutdown and will be liquidated soon.

Kochi Plant product details:

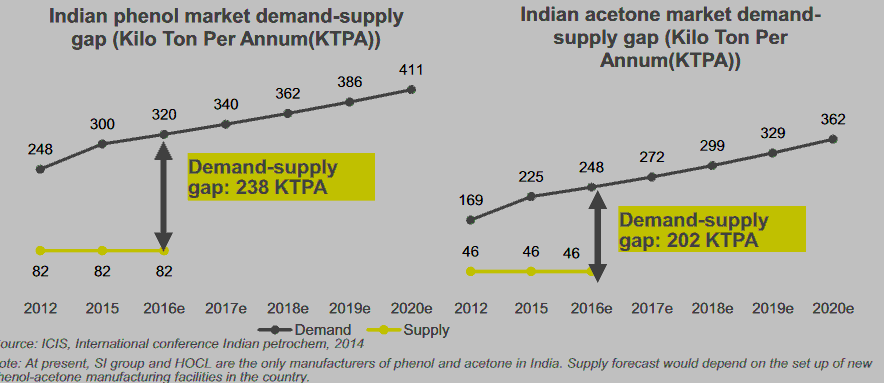

PHENOL is used in the manufacture of preservatives, disinfectants, lubricating oils, herbicides, insecticides, pharmaceuticals, etc. Hocl and SI(unlisted) is only producing this in india. India requires about 2.5 lakh tonnes to 3 lakh tonnes of phenol. Out of that the domestic market is producing only 80,000 tonnes. The balance 2.2 lakh tonnes is imported. Competitor (might be Deepak Fert) is producing another 40,000 tonnes. So, 80,000 tonnes is the installed capacity in India and the balance is imported. This data is according to 2015 stats, now the import quantum is much bigger. Last year Hocl manufactured 10609 TPA, which is very less mainly because of working capital issues, plant were shut down for several days.

ACETONE is another product with wide usage as a solvent for Cellulose Acetate, Nitrocellulose, Celluloid, Cellulose Ether, chlorinated Rubber, various resins, fats and oils and an absorbent for Acetylene Gas. The Indian acetone market, currently estimated at 180.5 thousand MT, is expected to grow at a rate of around 11.0 percent till 2022. Currently india imports more than 80 percent of acetone consumption in India. Indian companies manufactured 25000 metric tons, HOCL manufactured 14000 of the same.

HYDROGEN PEROXIDE is an eco-friendly chemical with wide application in Paper and Textile Industries for Bleaching purpose as a substitute for hazardous Chlorine. It is also used in Electronic and metallurgical industries, Effluent Treatment Plants, Sewage Treatment and for removal of Toxic Pollutants from Industrial Gas Streams. I don’t have the india production data for this but HOCL produced 9000 TPA in FY 18.

Subsidiary Unit Hindustan Flouro Carbons Limited (A Subsidiary Company of HOCL),Telangana makes PTFE. Hocl plans to divest the stake in this company and bidding process is already completed for the same.

What happened in the past (Bad times):

HOCL was a blue chip Company till mid 1990’s and all plants are making good profits. But suffered heavily due to steep fall (50-60%) in international prices of its main products, e.g., Phenol, Acetone and Aniline during 1999 other than changes in customs duty resulted in loss of revenue to the Company that adversely affected its profitability. The Company could not implement plans and projects to cope with economic liberalization and globalization, ex: The projects Caustic Soda (20,000 MTPA), PU Systems, Jawaharlal Nehru Port Trust (JNPT) Tank Terminal became NPA assets for several reasons. The Company had borrowings (Bonds) to the extent of ₹250 crore for the said projects, with annual interest burden of ₹31 crore.

HOCL rasayani plant used manufacture 14 products with 2300 permanent employees. Most of the capacities of rasayani plant is less than 10000 TPA without any economies of scale. During no anti dumping duty phase, HOCL unable to compete with cheap imports because of high crude prices resulting losses. Later company issues commercial paper with 250 cr for Caustic soda plant set-up by agreeing power cost @4rs with Maha govt. But when the project completed power price was changed to 8rs halting the project even before start.

HOCL has stopped 14 plants operation in Rasayani because of commercial viability and working capital issues. Subsequently 2300 employees wage cost on govt revised guidelines is simply mounting the debt pile. Bleeding with continued losses, HOCL was registered for BIFR as a sick company in January 2005. Subsequently, a rehabilitation proposal was approved and implemented by the Government during 2006-07. As a result, the company made a profit of Rs. 17.04 crore during 2006-07 and Rs 13.61 crore in 2007-08 and came out of the BIFR in May, 2008. As per rehabilitation package terms, HOCL has been given time for redemption from 2011 starting 20% for five years for total 270 cr.

However since 2011, anti dumping duty is expired from JAPAN, EU , USA and Taiwan and the process of re imposition of ADD is delayed by 2 years and this resulted once again mounting losses for HOCL, particularly Rasayani plant is idle with huge employee base. Moreover the rehabilitation package is 70% used for employee VRS and other non operating expenses such as paying the debts and not on any other aspect to strengthen its functioning. This resulted HOCL once again running behind working capital issues. Govt had postponed redemption action to 2017 with 25% redeem every year starting 2017 in four yearly instalments. HOCL by 2016 , company had accumulated losses of 1100cr other than 270cr govt revival package. With accumulated losses resulting in erosion of net worth of the Company, HOCL was again referred to BIFR for the second time in 2014, since then it never recovered.

HOCL Kochi plant is always generating profit, but this is moved to rasayani wage expenses. This inturn creating working capital issues for Kochi plant as well.

Ex: HOCL Kochi unit sourcing its main raw material LPG and Benzene from BPCL which has an adjacent refinery (KRL). The supply of raw material is through pipeline. Since HOCL could not clear the dues of raw material suppliers which had accumulated to the extent of Rs. 100 crore resulting in BPCL stopping the supply of raw material to Kochi unit.

HOCL did the below actions to overcome the crisis

• Sale of surplus obsolete unserviceable Plant and Machinery at Rasayani. The Company has realized ₹40 crore over the years by way of sale of old plant and machineries.

• An amount of ₹72 crore can be realized as upfront lease premium from CONCOR towards 60 Acre of land proposed to be leased at Rasayani.

• Similar negotiations with M/s HPCL and BPCL for leasing of land.

• Scouted for 1million ton aniline project setup with gujarat state PSU majors.

• Trying to sell unused land to create working capital liquidity issues.

Being the PSU where govt approval required for all decisions simply didn’t work in the short term for handling the crisis.

So the problems of high debt, idle assets, technical up-gradation failures, working capital issues, laziness in decision making, failing in taking protective measures of govt company , all in all ground level issues faced by distressed PSU is happened.

Recent Updates in right direction:

• HOCL Rasayani plant is 1000+ acres in size with plants, accommodation occupying 300+ acres. Finally govt approved the land sale last year to BPCL. BPCL bought 442 acres from HOCL at a rate of 1.4cr per acre resulting 600cr, company received 350cr and balance amount will be settled this year.

• Similarly HOCL manufactures N2O4 rocket propellant exclusively for ISRO, considering this ISRO bought corresponding unit for 30cr and govt gave bridge loan of 300 cr to clear all bond paper redemption.

• HOCL board approved another 240 acre land sale to BPCL in march, this will generate another 400cr.

• Similarly company holds 8 acre land in Panvel, selling process through NBCC is in progress.

• Rasayani plant already shut down and all the employees were taken VRS adoption, resulting no further cash flow to this plant.

Totally these 1400cr will help HOCL coming out from all the short, long term liabilities and running the Kochi unit normally. Kochi unit generates 5cr profit per month when it run successfully during 2015. Kochi plant is running normally in the current year, this is started generating operating profits after several years.

Next Planned actions:

• Streamlining Kochi operations, SAP ERP implementation is done for the same.

• Up gradation on Kochi plant with the below priorities.

• Kochi plants are producing phenol and acetone and they are money earning plants. These plants are not having the latest technology. Change of catalyst from Solid Phosphoric Acid (SPA) to Zeolite technology catalyst involving a capital expenditure of Rs. 60 crore , by which the capacity of the plant can be increased from the present 54000 MTPA to 90000 MTPA and the production cost can be reduced by 5%.

• It is also proposed to increase the capacity of the existing Phenol plant from 40000 MTPA to 68000 MTPA by debottlenecking / revamping with estimated of Rs. 200 crore.

Currently the main chemicals Phenol, Acetone and Hydrogen Peroxide all are having only 20-30% domestic production, india is depending on import of all these.

Ref: • India: phenol production volume 2021 | Statista

All these 3 product projected growths are anywhere between 6-10%

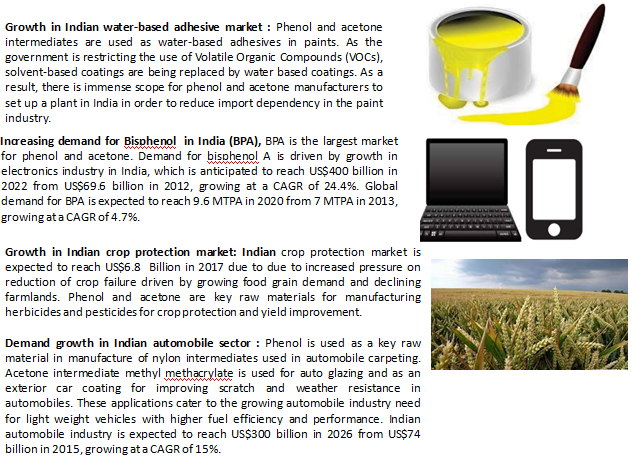

Demand Drivers for company products

Currently no new projects are planned and any new project for 100KTPA acetone will be 600 crore with a breakeven period of 4.5 years.

Under these circumstances company is in a nice spot w.r.to opportunities. Atleast the recent actions initiated by mgmt giving hope of company moving in a right direction.

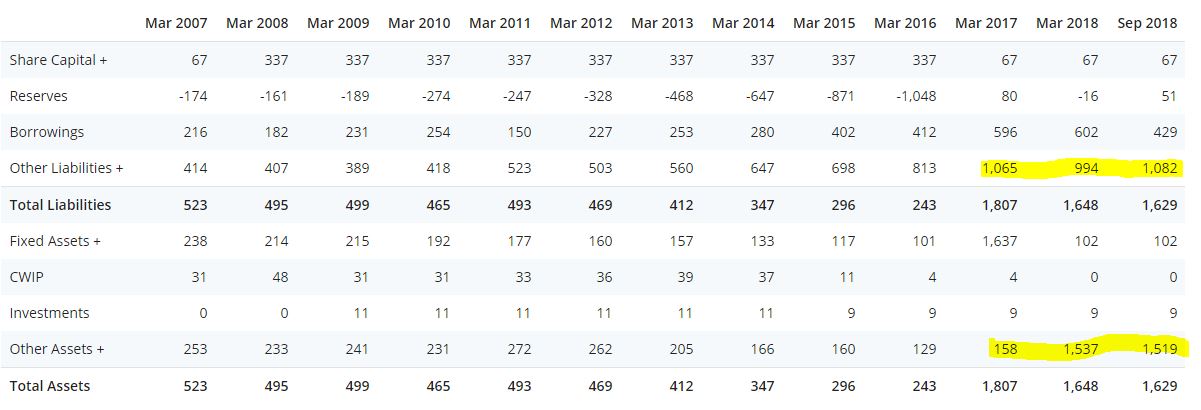

Financials

Observations:

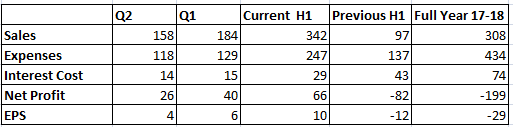

For H1 company reported sales of 342cr vs 97cr last year registering 3X growth implying no dearth of demand.

Net profit of 66cr vs net loss of 82crores, other income played a major role in this. But good to see the operational profit also coming as 20crores.

EPS of 10rs vs -12rs for the half year ended with Sep,2018.

Positives:

- Anti dumping duty on all the products, protecting the company. Most of the countries Taiwan, EU, Middle-east, Japan others till 2020 October,with Duty amount ranging between 80$-250$ per MT.

- Working capital issues are cleared, running the KOCHI plant normally for 6 months continuesly the first time in last 6-7 years.

- Major working capital issues are resolved and concrete plans of kochi plant upgradation.

- Only 2 companies in acetone and Phenol, less than 5 companies operating in Hydrogen peroxide providing no headroom for much competition. No new projects atleast for next 3 years coming up in india leaving demand to propel as expected.

Negatives:

- PSU tag and past history of referring to BIFR state.

- High crude prices will dent margins

- Regulatory changes w.r.to Anti Dumping Duty might spoil the show, currently the ADD exists for 2020 on

Disclosure:

Currently stock price @34rs with a market cap of 225cr. I am considering it as a turnaround story with the changes and i am invested in this company.

( Ofcourse we still have a problem of complete understanding of other income category).

( Ofcourse we still have a problem of complete understanding of other income category).