Does anyone have an idea why the stock is tanking? Is this a good opportunity to buy the shares?

Earning this quarter may be little effected by appreciation in Rupee.

Thanks

Very good earnings considering FX, amazing EBITDA margins and CFO (FCF - ~24% of market cap). Stock should see UC tommorow, open at ~800+ levels

500 cr annualized EBIDTA, 1100 Mcap, 200cr Debt. The most undervalued stock listed on NSE

Disclaimer: 19% of PF, hopefully a lot more after today

1 Like

I am perplexed why this stock is so unloved by the market.

Compared to FY2016,

-

EBITDA margin improved,

-

NPM improved, decent top-line growth, very good bottomline

-

more importantly, they paid off around 200cr from debt and Net Debt/Equity reduced to half compared with last year.

-

Q4FY17 EBITDA margin was the highest quarterly in the last years.

Any experienced members can throw more light on this please?

Just a terrible time to be an undervalued stock in the market, will be buying more - clearly, fair value is over Rs. 1,000/share

BPO industry seems to have low moat; what is the moat for HBS to in business for 5+ years?

The HDFC Securities report has a better explanation, but HGS isn’t a traditional BPO player, and has amazing customer stickyness. Also, moat is overrated - this is a stock that is growing your equity at literally ~25% p.a. (earnings yield adj. for dep and capex). HGS also has had amazing growth compared to other listed BPO players, because of their technology acquisitions.

Management could def. do a better job of capital allocation, but I am expecting ~Rs. 45-50/share dividends soon (they used to give ~20-25 a share earlier, before they ran into some margin issues with the Canadian acquisition).

i think it has got to do with lot of negative news surrounding the IT sector, expectation of strengthening of rupee. Most of the IT stocks are down. The entire sector is affected.

@manishinlucknow this is not about recent IT; the stock has traded cheap for most of its history at similar PE levels.

couple of reasons coule be, unlike IT this company is not debt averse, decreasing margins and BPO tag.

Could possibly go for rerating with increase in margins and decreasing debt (dividend has always been good, but with recent buybacks by IT companies, appeal of dividends would go down)!!

1 Like

Quite a disappointing set of numbers by HGS - one wonders what would have been different without the rupee depreciation w.r.t. profitability. Not only has profitability decreased, HGS’s revenue growth has also slowed down (6% CC growth)

Still, at this price all this and more is discounted. Assuming 6% rupee depreciation, we should see ~12% sustainable growth still, which is very healthy given current valuations (3-4x EV/EBITDA). My hopes of further improvement in earnings and especially quality of earnings is the digital push by HGS. Although we haven’t seen any effect of this in either margins or revenue growth, a quick look at HGS’s youtube page gives a glimpse of this technology:

https://www.youtube.com/watch?v=eJSXib2-X7c

In particular, the part about hiring nurses to conduct telephonic consultancy/after care services piqued my interest, especially considering the push towards Value Based Care in US, which is increasingly taking place of Fee for a service in the US healthcare system. What this means is that hospitals are compensated not for the service undertaken, but for outcomes, incentivising them to follow up with patients and remain in constant touch. This is someplace where HGS could find a lucrative niche, although only time will tell.

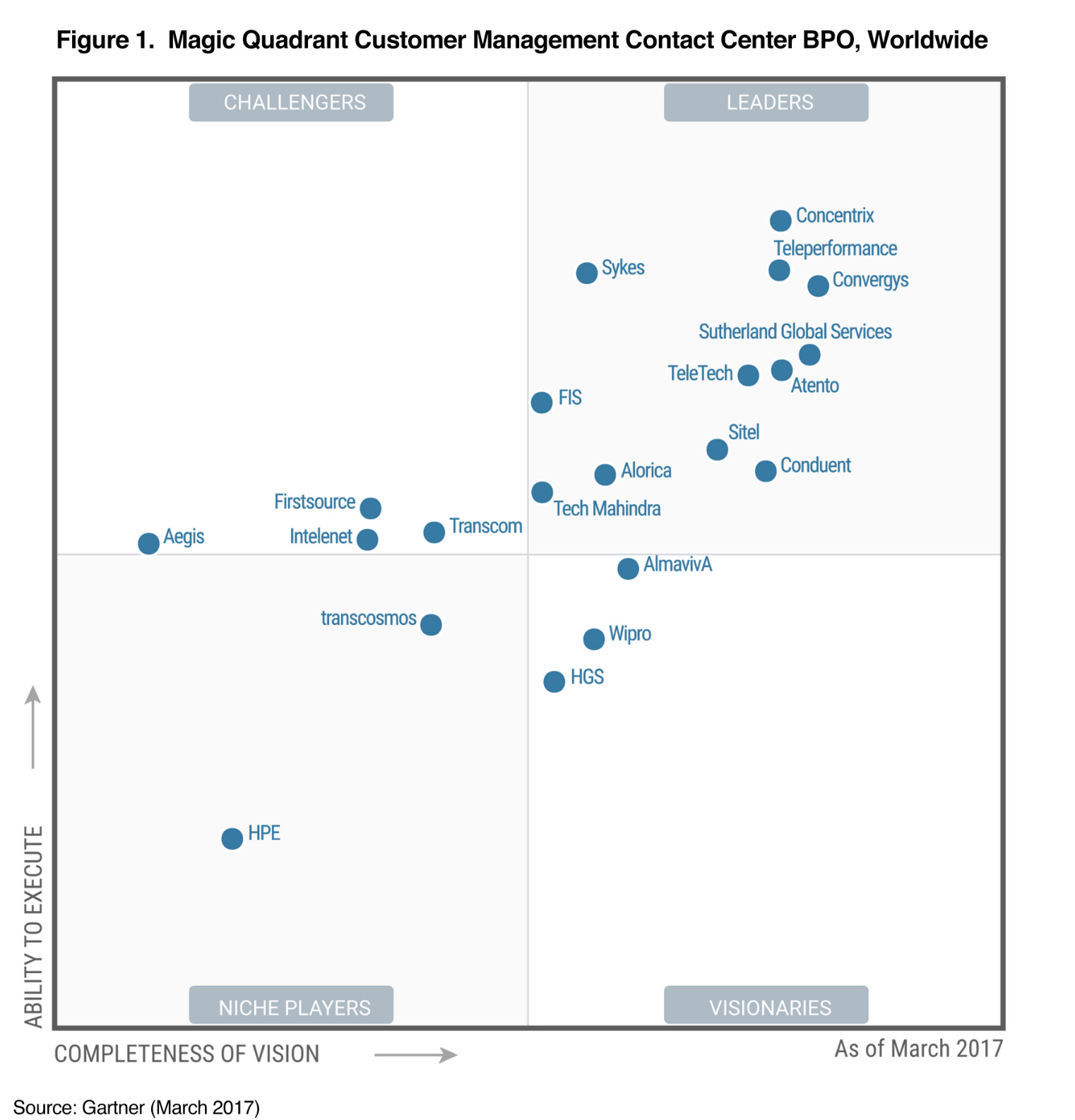

Also, although HGS’s digital capabilities have not yet shown any evidence in earnings (digital is a measly 4% of revenues IIRC, showing the low cross-sell penetration achieved even after years of launch), HGS’s positioning in Gartner’s magic quadrant as well as its move towards innovation is heartening.

At the same time, management commentary is bland and undescriptive, particularly the lack of highlighting of the move towards an opex rather than capex model. Maybe this is indicative of underlying weakness in being able to continue going forward?

Either way, I’m holding on. This is a company that has been buffeted by headwinds in almost every possible way over the last 2-3 years - slow turnaround of an acquisition, CAD/USD depreciation in 2015-6, INR appreciation, and large investments in digital technologies that have yet to paid off. Each of these could eventually mean revert, forcing the market to re-look at this business and re-rate to a higher multiple on the back of higher earnings.

Disc. Largest position in PF, heavily invested

6 Likes

http://www.bseindia.com/xml-data/corpfiling/AttachLive/f8852d45-ea41-42dd-9015-c1dd3677382b.pdf

very good second qtr result with 70%cash flow debt reduced available at less than 1 book value

2 Likes

if we compare it with first source solution it is available at more than 100% discount to its peer and the metrics such as roe roce and roa have improved this fy roe this fy 18 will be around 15% and debt is less than 500 cr and net cash positive with 350 cr cash in books and 100 cr in investments it is available at an earnings yield of 15% makes this attractive bet in this expensive market even assuming 1.5 book value and an eps of 95 for fy 18 the PBV x PE of 10 fair value works to 1000 and the market cap 0f 2100 and enterprise value of 2600 still availble at less than 6 evebita

i request feed back on valuation front

2 Likes

Presentation from latest investor meeting

http://www.bseindia.com/xml-data/corpfiling/AttachLive/e0646e43-4462-41ec-8949-05635db64181.pdf

Key takeaways:

Well on a stabilized path to profitability after being rocked by Canada issues and loss of telecom clients

Have continuously diversified beyond telecom

Company does not seem to have a stated dividend policy, it felt like they are conserving the cash to line up an acquisition (this is my opinion)

Of the various biz segments

-Healthcare is performing well and expected to have double digit growth

-India HR biz is very strong. They are by far the leaders in some segments. Strong growth and returns business that does not get the multiple it deserves as its a relatively smaller piece (it should ideally get Quess/TL multiple)

-UK biz seems to be lagging a bit

-Philippines felt like its also plateauing

-Jamaica is the big growth driver.

-There is a upcoming Canadian min wage hike around the corner. The company has already put in place a plan to counter its impact. While details were scant, the management seemed confident that impact will be minimal if any

Overall, in my view, it looked like a competent management team who are nimble to chase pockets of growth. And if they deliver on growth, there seems no reason why it should trade at where it does today.

2 Likes

2 Likes

Hgs have sold off the CRM Buisness and this quarter has given a very good result with 15 rupees dividend and the stock has hit upper circuit today anybody can please share some thoughts on this.

Q1 result looks goos with consolidated EPS of 22.97 and they declared that they are going to add 2000jobs in Q2 and 3k in q3

But still the price is below 700 with pE of just around 6.

Any thing wrong with the company?

Can you provide the source of this info?

| Press Release Titled 'Business Process Management Industry Gets A Boost During COVID-19 | 09/11/20 20:40 | |

|---|---|---|

| This is with reference to Press Release titled ‘Business Process Management Industry Gets a Boost During COVID-19’ submitted to the Stock Exchanges on September 10, 2020. |

The sub-heading of the said Press Release ‘As global brands seek innovative customer experience solutions during the pandemic, HGS announces plans to add more than 2,000 U.S.-based jobs through Q3’ may please be read as ‘As global brands seek innovative customer experience solutions during the pandemic, HGS announces plans to add more than 2,000 U.S.-based jobs through Q2’.|

1 Like

2 Likes