Doubt that the books are cooked given the promoters. Also, the Company has been generating fair bit of cash and has been pretty consistent with dividends; implying profits are not just accounting numbers.

Although, debt might raise some concerns, but on a net debt basis, the balance sheet looks fairly stable.

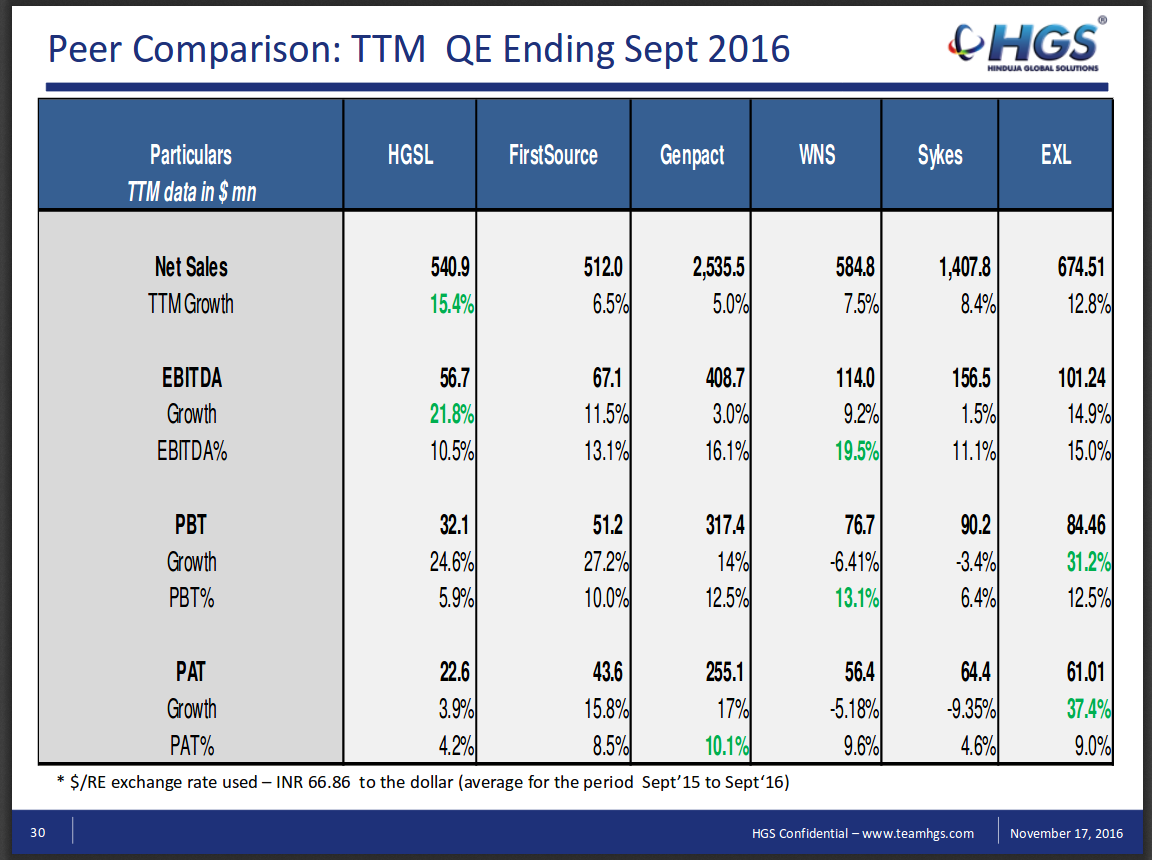

Profitability lately had taken a hit (not the last quarter, but prior) due to their acquisition of Mphasis BPO and troubles with Canadian operations. Appears that things are changing for good basis last quarter and consistent delivery on margin front will be a big positive for the share.

Noticed in BW print edition that HGS is ranked at # 15 on biggest employer with ~40k emloyees. Last year it was ranked 257. Not sure if right to conclude that SUCH massive hiring happened just within last year to propel the ranking sky high. OR some changes in survey methodology over time. unableo to check ARs at the moment as traveling

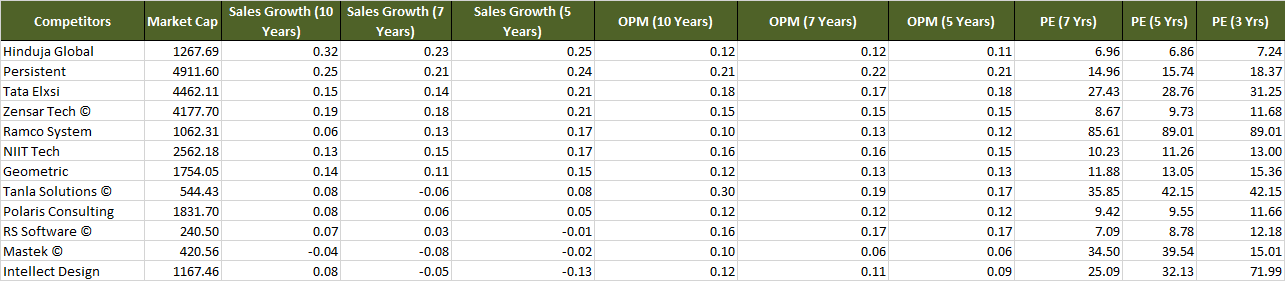

The company has registered a sales growth of 25% CAGR over the past 5 years. There seems to have been a dip in profits during FY15, but the company has regained lost ground during FY16. However other companies like Zensar, Mastek, Tanla had fared pretty well during 2015. Hinduja is heavily reliant of the Healthcare sector, but I couldn’t find any other companies operating in the same area as Hinduja during my brief research which could give us a better clue as to how the company is actually performing and the future value it promises.

Fundamentally it seems like the dream company, with a consolidated PE as low as 7, this is dirt cheap. Other solution providers at the same levels are all above Hinduja inspite of having lower sales growth and profits.

The company has been maintaining a stable profit margin, however it has declined in the preceding 3 years, so the scenario begs the question why are the increases in sales not resulting in higher profits. At the same time the debt to equity ratio has been steadily increasing. The other concern is that they have been raising short term debt to fund certain long term fixed assets. Although the debt bears very low interest rate of 2.9%, the company seems to have been been paying dividends too from the same short term debt.

The positive is that the company’s cumulative cash flows for the past 10 years and 3 years have been more than its PAT, thereby there has been good cash management. The promoters are credible and the promoter holding has been around 67% which is decent.

Are the cons i.e. increasing debt and disproportionate increase in sales with respect to profits enough to warrant such low PE? Any comments are welcome.

Dear seniors can somebody throw light on the difference between total comprehensive income and net profit why is it on lower side in Hgs case if some seniors can explain what is comprehensive income that will be also helpful pl.

@Gaurav this statement SAS made by them in their Q1-FY17 CONCALL. If you listen to the recording or read the transcript, you will find Mr. Sarkar making the statement towards the end of the call.

Do let me know if you can’t locate the same. FYI I use research bytes.com to read or listen to concalls.

Let us analyze, what is furious according to management

Revenue growth for Sep 15/16 = 15% YoY. Therefore a reasonable growth will be 6-7%, which is why the stock is trading at such low price-to-earnings ratio.

Even if the company was growing at a 0% growth, say forever, IMHO, such a low P/E multiple is not warranted. If this company does a leveraged recapitalization of itself, it could unlock significant value (as Charlie Munger’s investment philosophy for value stocks goes). Considering an EBIT of ~380cr, we can easily have an interest outgo of around ~200cr, which at a 11% rate of interest amounts to ~1820 cr, with the remaining 180cr of Operating Income and 30cr OI covers depreciation, CAPEX and WC, with an equity value of say ~200cr because of future growth on a base of 380cr.

Net Value given to shareholders = 1820 + 200 = 2020 cr vs M. Cap of 1200 cr

Apart from that, the business is growing at over 15% CAGR, and I expect it to grow faster at around 18% CAGR on the back of large baby boomer retirement in the US (~10,000 a day), leading to vast increase in its health care revenues, which now comprise ~40% of its revenues (IIRC) and almost all of its incremental growth, so as the share of health care increases, overall growth rate will increase.

Thus I believe that the company is being grossly undervalued by the market right now, and hold a large chunk of it in my portfolio.

P.S. Also note the large depreciation number in the Income Statement, its almost as large as PAT, which means cash earnings are double PAT (market cap is only ~3.5x PAT + Depreciation!). Only reason it doesn’t turn into cash flow is due to CAPEX and WC needs for a growing business, but I expect these pressures to decrease on the back of the work at home innovations.

The Essar group just sold its BPO arm Aegis with revenues of $400m for $275-$300m. HGS has $550M in sales (TTM), and should be valued at $400M with the same multiple. Subtracting $125m of debt, we have an equity value of $275M, implying a share price of over Rs. 886/share.

I concur with your observation. I also did a calculation on the revenue growth of the company and over the last 3-4 years, it has growth at an average rate of 21%, which is remarkable by any standards.

rev gwt

2013 - 27%

2014 - 26%

2015 - 12%

2016 - 18%

Avg - 21%

Also in an recent interview management said they can maintain this revenue growth for next 3-5 years easily.

Company seems to be grossly undervalued. I do not think it can remain so for very long.

Absolutely Gaurav! I have realized that Mr. Market is extremely cautious and scared of margin degrowth due to the currently unfavourable fluctuations in CAD/INR but I honestly think these are all short term woes that hide a gem of a company - 3x P/E growing at 25% p/a. I am happy with Mr.M not knowing about it because I have been only increasing my holding in HGS from 2015, and all the while the stock has gotten cheaper due to the growth and retained earnings!

Agreed, currency fluctuations are short term woes and will subside with time. I am not worried about them. I am more concerned about sustainability of revenue growth.

Since you are keeping track of the stock from last 1-2 year. What is your opinion about the management ability to convert guidance into reality?

They have guided for similar revenue growth for next 2-3 years which is very positive provided they can deliver.

I think they service a big chunk of Canada/ US through their centre in Philipines and not India; although I am lacking report which i read to support/ corroborate!