Pre-commissioning team is on board at KGB offshore installation now.

We need to replace few equipment which will be delivered in next couple of weeks.

Service engineers from OEM will be onsite this week.

Overall we target to complete all commissioining and testing activities to commence production activities by end of March 2022.

Oil will be produced first and then Gas immediately after that.

All offshore facilities which are weather dependendent have been completed.

Getting global experts has been difficult due to covid wave.

Covid wave 3 impacted quite a few of our employees.

Gas contract will be awarded by the end of the month.

Gas contract price - Brent crude *(12%+ premium %) with $6 as floor price.

Hi, everyone. I am a new investor in the company. I went through their Q3 concall and the management said that the production from B-80 will start in March, however, the oil realizations will come in the p&l from June onwards. They said that they will store the oil for the time being. Can someone please tell me why they are doing this?

The oil which will come out of B80 wells will be stored in a floating vessel which remains in position. The tankers which will lift the oil from this vessel is generally of 240, 000 barrels capacity. The production of B80 will be around 4000 barrels of oil. So HOEC needs to store 60 days of production in the floating vessel and then move it to the tanker. Tankers will come, take out the oil from storage vessel and then move. Tanker hiring costs a good amount hence those lifting oil will need quick filling and release of vessel.

You can refer to investor presentation below: http://www.valoremadvisors.com/hoec/

Happy to hear that the weather window dependent part of the installation is over. So we may actually see production starting from March’22. I understand that production from an offshore facility is challenging, but the gap between the initial first oil target of June’20 and now is really frustrating. Now with brent crude crossing 115 $ , it can be a unique hedging bet. But for this to work the company should start producing from B-80 as the current contribution of oil in its EBITDA is negligible.

Company mentioned that they have started selling gas from Dirok at a premium to Govt administered prices on the basis of e auction concluded earlier. About 20 % of gas from Dirok was sold at premium. And Iam happy to see the company naming their customers in North East viz, NRL, BCPL, NEEPCO and AGCL.

Also the gas prices will come up for revision in April and industry expects a steep increase tracking weighted average of gas prices at major gas hubs in the last quarter.

Key risks

Company has been continuously changing the target date for oil production. So it needs to be seen whether it will start producing in March’22.

The quality of crude produced from B-80 is yet to be known, eventhough the company once mentioned that it will be close to that of Brent crude.

The offtake of gas from Dirok is not guaranteed and hence we may not know whether the company will benefit fully from higher govt administered gas prices. In the absence of pipeline, company is fully dependent on North East companies for the offtake. There were quarters in FY19-20 where the production had to be curtailed due to reduced offtake.

Looks like the US and Europe will depend on other countries for import of oil and Gas.

Russia May stop supply till d December.

HOEC can be huge beneficiary of this.

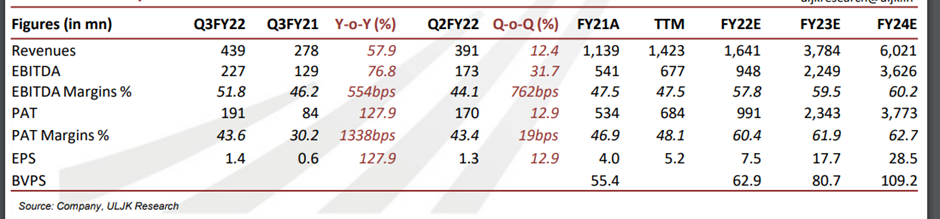

ULJK has given TGP 300+ levels , however just one doubt about that report is that they have considered full year revenue at 378.4 crore , shouldn’t it be more considering premium they are gonna get on GAS

Gas prices are likely to move up from $2.9 to $6.5 from 1st April 2022. This is a steep hike of 114%. HOEC had sales of 44Cr last quarter which is primarily gas sales from Dirok. So the sales should go up to 90Cr+ per quarter from Dirok only. That means 350Cr kind of sales for FY23 from Dirok gas only. B80 should be 400Cr plus. So the figure looks surprising to me as well.

Risk: Government doesn’t allow the gas prices to rise.

Domestic natural gas prices hiked to 6.10$ per MMBtu. However, B- 80 disappoints with production further delayed due to unanticipated production issues. Corrective action being undertaken by the company. No timeline mentioned

Please see the earlier post of Raj1968 for your answer. Gas price was raised from April only and not 6 months back. Please make your own due diligence before posting queries, lest VP moderator will intervene.

Further to my earlier comments, I would like to bring the experts/seniors attention to a clear case of insider trading in HOEC. Recently the Company declared Q4 and 21-22 annual result. Result was broadly in expected lines. There was no mention of eagerly awaited update on D80 production. This is expected to be a game changer. But Company informed that they will conduct con-call on 2nd June. All of a sudden on 31st May, huge volume spike was observed. On 1st June, after business hour, company uploaded investor presentation on stock exchange website, where D80 production commencement was announced. Predictably stock went up 10% on 2nd June, but closed in red amidst huge volume. It was a clear case of dumping on news. It is apparent that insiders were involved in this case. Buying low and dumping on news with huge volume proves this.

We know that, it is common practice in India. But stock exchanges and SEBI are expected to do surveillance in this regard. As genuine small investors, we are always at the receiving end. Can’t we stand up and force authorities to tackle this menace?

First Oil production and Gas sales commences from Block MB/OSDSF/B80/2016 (B-80)

HOEC is pleased to announce that both the wells D-1 and D-2 have been individually brought online

for production after successfully addressing the technical issues faced during pre-commissioning

operations. Gas sales to GSPC commenced from ONGC’s Gas Processing Terminal at Hazira.

Prior to commencement of sales, gas produced from well D-2 was processed to meet the specifications

and packed into ONGC pipeline from May 31, 2022 onwards. Subsequently, Gas Transportation

Agreement (GTA) between ONGC and HOEC was executed on June 03, 2022.

Currently, D-1 Oil well on production is being flowed at lower rates for safe stabilisation of all

operational parameters. Produced oil is being transferred through pipeline to a HOEC group-owned

Floating Storage Offloading vessel (FSO). FSO has the capacity to store over six months of production.

Processed gas is being exported through the ONGC pipeline network to its Hazira Gas Processing

Terminal. ONGC then redelivers B-80 gas into the flagship HVJ pipeline owned by GAIL. GSPC then

offtakes the B-80 gas to deliver it to the end consumers through its vast pipeline network. We expect

the entire production and sales operations to stabilise over the next few weeks.

HOEC is pleased to be the first Indian private operator to complete a green field development in

Mumbai Offshore Region. B-80 has earned the distinction of being the first offshore field on

production, under the path-breaking Discovered Small Field (DSF) Policy of the Government of India

with a Revenue Sharing Model. DSF encourages participation of private sector to increase domestic

production both from offshore and onshore discovered fields in India.

HOEC places on record its deep appreciation and gratitude for the excellent support extended by DGH

and ONGC.

The D1 block will have the output of roughly 4000 barrels per day. HOEC has 50% interest. So from revenue stand point 4000*$1009077 ~ 275 Cr revenue per quarter. i.e. ~135 Cr. I am excluding the gas output of 10 mmscfd gas which they commenced from 31 may. Management has not committed any date so far for the oil output commencement. Let us say it takes another year(just a pessimistic assumption). Excluding all other revenue streams, the oil revenue from B-80 field itself provides the revenue of 550 Cr. per year. Is this a fair understanding on outlook for the B-80 oil contribution?

One change - HOEC has 60% participating interest. Oil alone can contribute 650-800 cr annual revenue at $100 per barrel. Gas should be another 275-300 cr.

I think one year is on the higher side. If the production has started, they would need a 2-3 months for stabilization and couple of months of storage.

@menoopatil- A small clarification. HOEC has 60% production share from B80 and not 50% as mentioned by you. Moreover, you can not ignore gas production from D2 as it is 10 mmscfd. This number is huge. As per supply contract with GSPC for 2 years, monthly sale of gas price in US$/mmbtu will be calculated @ 22.2% of previous months average Brent crude oil price in US$/barrel.Floor price will be US$6/barrel. See. With average Brent @100US$/barrel now, gas price now is 22US$/mmbtu. At 60% share, it is capable of contributing more than 200 cr profit annually at peak production capacity depending upon prevailing crude price.