Is it time to look at upstream Oil and Gas companies??

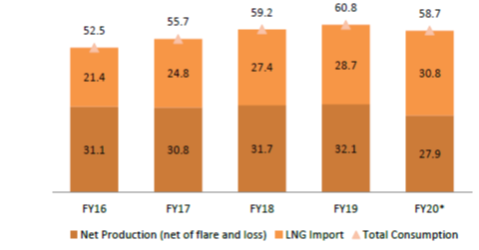

India is highly reliant on import of Oil and gas for its requirements. Lets look at the level of imports we have

Source: care rating

It’s clear that the imports are constantly increasing and reached a point where imports have exceeded the domestic production. While crude prices are determined by market forces, Domestic gas prices are fixed by Gas pricing policy, 2014 which considers the weighted average of gas prices in US ( Henry Hub), UK(National balancing Point ), Canada ( Alberta Gas), Russia with a lag of one quarter. Prices are fixed for a period of 6 months once in April and October every year.

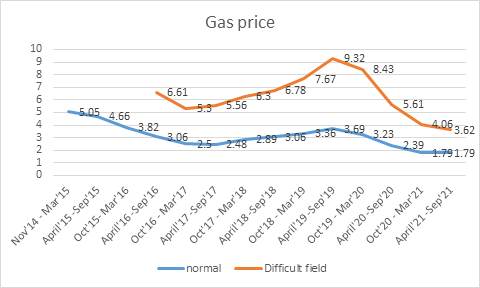

Let’s take a look at the gas prices in the past.

Source: PPAC

Gas prices for normal fields have come down from 3 .69 $/mmBtu in the Oct’19 to 1.79 $ in Oct’20 to Sept’21. The gas prices are currently at 7 year low. Due to the above pricing where the prices are fixed based on the average in gas surplus countries, the landed cost of gas imports are higher than the domestic gas prices.

In the past 6 to 7 months global gas prices have moved up significantly due to the North American heat wave. The current gas price at Henry Hub is 3.80 $/MMbtu. Gas industry is expecting a price rise of around 50 to 60 % when gas prices are up for revision in October( Source interview by ONGC chairman).

I have focused on a much smaller player, Hind Oil exploration. The company started production of natural gas from Dirok gas field in 2017 where it has a 27% participating interest.

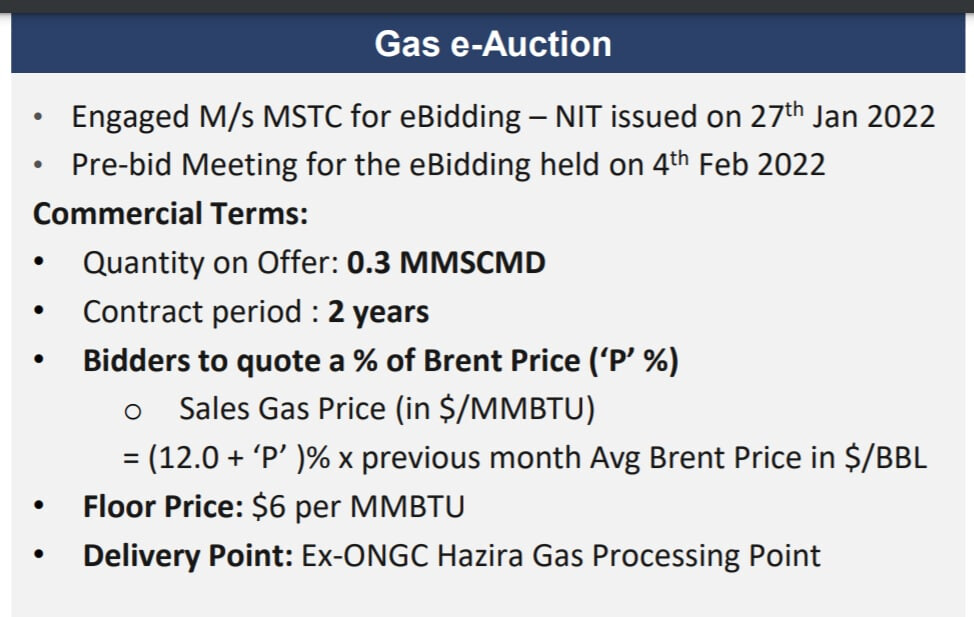

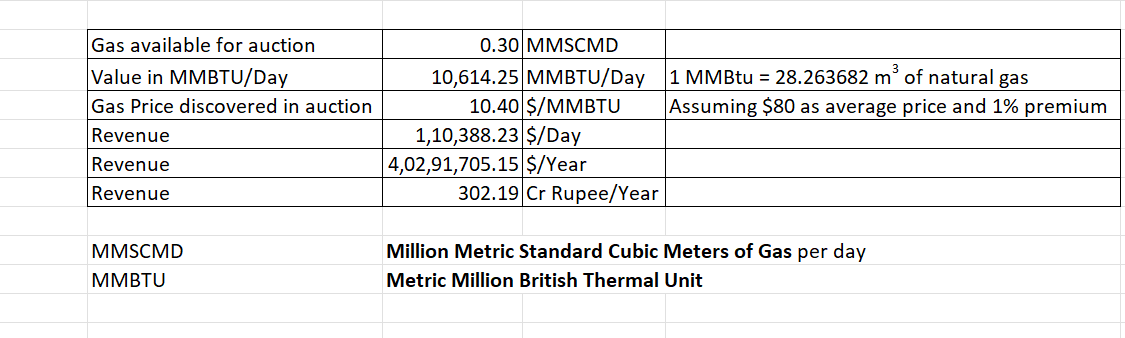

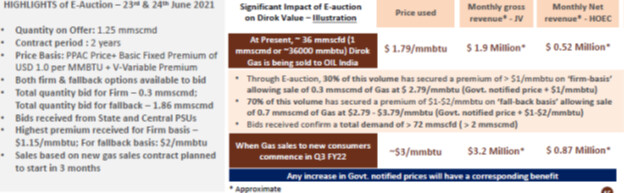

As part of reforms on natural gas pricing norms govt has up with norms for e bidding in case of fields with marketing and pricing freedom. The company was for some time talking about an e auction and finally in Q1. The company has up with an e auction for its gas produced in Dirok field on a firm and fall back basis in Q1’21.

source: company Q4’21 presentation

Company received very good bids from various customers for the whole quantity on offer and company expects to start sales a per the new contract from Q3’22. As per the company contracts are in final stage of conclusion. Thus e auction may further increase revenue in addition to the increase in Govt administered prices in Q3’22.

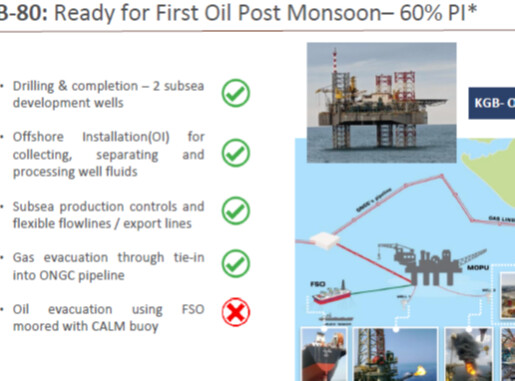

Production updates from B80

The B-80 field was awarded to the company in the Discovered small field round 1 held by DGH where the company has a participation interest of 60%(pending govt approval). The company expects to produce 5000 boepd of oil and 15mmcmd of gas( 8000 barrels of oil equivalent). The company’s share of revenue from oil will move to 37% from 13% once the block starts production. They have marketing as well as pricing freedom for gas produced from this field. And the gas produced will be evacuated through ONGC pipeline and Gujarat will be the target market. This assures better offtake as well as premium for gas. The field was supposed to deliver first oil by June 2020. But the project got delayed multiple times due to covid pandemic and weather uncertainties. Finally, it was expected to start production from the site in the weather window in April – May’22. However, the company had to halt the project through midway due to Tauktae. As per latest investor presentation Q1’22 company has informed the major parts of the project are over and production is expected to start in Q3’22.

Updates from the company as in latest investor presentation.

As per initial estimates the whole final part of the project was expected to be completed within 45 to 60 days.

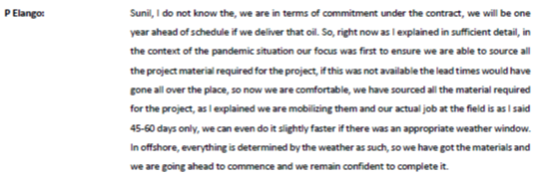

Excerpts from concall from Q221.

As a significant part of this final part is over now, the company is expected to start production in Q322 itself

The gas produced will be sold out immediately and will be revenue accretive from day 1 of production. Company has close to 900000 barrels of oil storage capacity and company is not planning to start sale of oil immediately on oil production. They intend to keep on producing for 2 months and then come up with a sale. So the revenue from oil sales will be more significant in q4’22 only.

Key risks

As already mentioned B-80 was initially projected to deliver first oil by June 2020. The timeline for project completion was changed twice since. The company attributed the delay to covid pandemic wherein company was unable to procure critical infrastructure items like flexible pipeline and SPM. Then there was the weather uncertainties. Eventhough this items are all procured now, monsoon is still an uncertainty.

The quality of oil is still to be tested. The company has mentioned that the quality will be close to that of Brent crude but it is yet to be verified.

International prices of both crude and natural gas is very strong as of now. Natural gas price had great run due to severe heat waves in North America. But once heat waves subside the natural gas prices may start correcting. And this may affect the price revision in April 2023. Similarly the way OPEC carries out its business will decide the crude prices.

The company is expected to get benefit of e auction from Q3’22. However, it is to be noted only 1/3rd of the contract are on firm pricing and the remaining will be on fall back pricing which means the offtake and pricing on 2/3rd production will be based on natural gas demand. The company has had offtake issues for gas produced in Dirok fields in multiple quarters in FY ’20. Dirok sales will depend on demand in North East until gas grid connects North East with rest of the country.

To conclude there are multiple tailwinds for the oil and gas industry in the form of higher administered gas prices expected when gas price comes up for revision in October 2022. The company has additional advantage of e auction prices for its Dirok gas from Q3’22 in addition to commencement of production of oil from B80, one of their priced assets.

Discl: Invested in Hind Oil from lower level and hence biased. Tracking ONGC as well. Currently holding purely as a cyclical bet. Has been holding and tracking the company since 2017, has been a disappointment for long. Not a SEBI registered advisor. Please do your own due diligence.