Did some analysis of the company. here are some facts / observations

Management :

They have done what they told they will do - capacity plans since 2013-14 onward is executed to the plan.

they are focused on building customer centric products - Even though they sell CTP - still sold as liquid / heated form , special grades for Anodes, Graphite UHP’s , Advanced carbon etc.

Have seen them increasing capacity by 100,000 MT through debottelnecking alone.

Results like this is there to see in the annual reports - i think they have the vision, they understand chemistry and R&D pretty well and they are hungry.

They hired a industry veteran , who is paid much more than CEO !!! . Its a Uncle and Kids Management otherwise…

They started doing ESOP’s , not allocated it to the family members in the company

"PRODUCTS"

It is the only player in India to produce Carbon Black from Coal Tar distillation process which offers cleaner product with ultra low sulphur content; competitors use crude based feed stock (CBFS) route which incidentally has high sulphur content

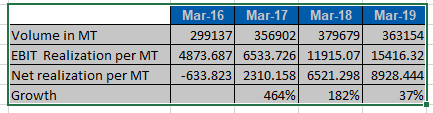

Due to high value / custom products, realization is improving.

In this, contribution of Specialty Carbon and Advanced carbon in 2019 is about 10%.

In Q32020 they are online with the capacity expansion of Specialty Carbon Black - 60,000 Tones. . Advanced Carbon black will come online by 2021. 20k tones of capacity . This will help company improve margin and realization further.

Risks

a. They run supply side risk of devalued raw material inventory when crude price falls after they have bought the inventory - 45 days worth of stock of raw material. this is seen in 2 years already

b. When the demand environment is bad, they start producing CTP - conventional product… so overall sales is managed around 1800 Cr per year, with 10% Net Profit. (my guestimate for FY2020 )

At current price levels., company is at 58% discount to intrinsic value of around 120 Rs - very conservative estimate. I have assumed degrowh for 2021, 2022, 2023… Just to be cautious of COVID19 sitiuation.

Note : this is my first attempt to write on the forum . Any feedback is welcome!!!. thanks

Whats your logic behind the estimate of 120/-. Thank you

The main risks I see with them following a conversation with their investor relations

Expansion plans stand delayed for both ACM and SCB. For the advanced carbon material they were looking at manufacturing the end product for Li ion battery makers but unfortunately those plans are shelved and they are going for an intermediate product.

Their realizations are turning south. Don’t expect Q4FY20 to be better than Q3 since the prices have gone down and the covid impact.

As a CTP manufacturer they will never get a premium valuation because the end product is a commodity which is cyclical and whose price is not in the company’s control. You can already view how bad their Q3 results were be because of the lower aluminium/tyre industry demand and price reductions.

Having said this, I believe the company is taking right steps in this unfavourable environment and so it deserves a more wait and watch approach

Discl - Invested since beginning of the year and holding for near term.

SEBI extended the timeline to announce Q4 results from 30th June to 31st July. Many companies complained that they are not able to source the revenue, since some of their associates/subsidiaries or even auditors are in containment zones.

Disc : Holding - planning to exit due to cyclical nature impact and tensions across India China issue. No thoughts on future

Good Set of dividend given

I’m holding it at avg 56/share. Looking to further add on major dips - i expect another washout in Q1fy21 based on conversations with the company. Reasons to continue holding

Portfolio transformation - delivered on SCB capacity

Rational decision - To delay ACM because they will no longer produce the final product and only the intermediate and therefore will have lower profitability than original plan. Makes sense to delay right now in uncertain demands to conserve cash

Earnings- I think a lot of the losses are notional ones and while scary it doesn’t actually lower the cash in the bank which can be seen in CFO > Profit before taxes. The investments in subsidiaries has gone south and I’m thinking it might the market might be more unforgiving than necessary with them owing to the terrible economic situation we are in.

Overall still there are significant downsides to the business itself but all depends on how definitively they are able to transform themselves from commodity CTP player to specialized chemicals. I believe they can do it considering the strong competencies already present

I feel that the stock will take more beating but could be a winner in 5 year timeline if the end industry demand rises.

Another reason - There was a post from an employee on LinkedIn that they were happy that the company(Himadri) did not cut pay during these times. Now I don’t know if this still stands true but I felt it was a nice gesture by the company to not cut pay

Modern high rise pvt ltd whose directors are also CEO of himadri Co holds Rs182 crores of equity shares of Himadri Co and at the same time Himadri Co holds preference shares of modern high rise pvt ltd of equivalent amount . Is it a matter of concern ?

I would like to understand this before investing in the co

Recently the anti dumping duties wherein government are considering to raise are increasingly making more Indian companies to prefer Indian goods than cheap China materials.

Same you can notice in Thirumalai Chemicals charts am unsure what products/exposure might been in consideration for HSCL under anti dumping list. Definitely not an company trigger for the price movements, its purely market driven based on news - dead cat bounce.

I didn’t find any news since January for anti dumping of carbon or dye or rest of the products . . Also u can see it’s peers such as rain, bodal chemicals not performing as exactly as HSCL.

Is this a run due to auto/true sector?

The company is dependent on china products as raw material to finish their goods . .what has company thought of this going Further?

Capex is getting done in for some of its products.

This huge buy in market indicates some momentum/news to come to light and may indicate good entry point.

Based on my conversations with IR, the management doesn’t give much importance to anti-dumping duty related events and consider it a low business impact event. The reason they cited was better product quality as they have a lower sulphur content compared to cheaper Chinese imports.

I’m not looking too much into the price rise recently because it is pretty much the same company it was in Jan when it was trading at ~70, and when it trading at ~30 in march. Nothing has really changed except for a big one-time loss in investment in the Chinese subsidiary.

This is a cyclical business and currently they have delayed their capacity extension plans so as to better manage current cash flow.

In conclusion, I believe it will take 2-3 years to unlock the true value.

I see in the latest investor presentation (just strated reading into this company) that they make advanced carbon materials (ACM) that can/will be use used in lithium ion batteries (LiB). With huge demand and government focus on indigenous production of LiB’s going ahead, Himadri seems to be a beneficiary of it.

Couldn’t find any competitor of Himadri in this area. Anyone any clue?

they have been promising Advanced carbons since last 5 years, but no performance yet. I dont think the management has the skills/ idea of whats needed for it. The project has started long time back never seen light . Wait and watch mode for me

Hi , I was hoping you would through some information on if they restarted investment into capex and ACM plans. I dont see any updates of that in the filings they have made and I remember you had some success with IR before.

Do you know anything about why promoter sold some shares? . I am a bit concerned why Bains Capital is dumping stock almost daily now… What do they know that we dont… I remember they bought at close to 320 Rs per share.

thanks upfront if you could share any information here.