I do not agree that in AMC business the risk on fund manager leaving and the impact on the business is very high. I will agree that the sentiment on the stock for a few months will get impacted very big, not the fundamentals. Such falls can create a wondeful buying opportunity. It is not a fundamental risk with an established giant like HDFC group which have impeccable risk management. Coupled with a fact that there are very strict laid down procedures by SEBI in addition to the strict procedures and processes which HDFC AMC themselves will have.

Recollect Jubilant, when the earlier charismatic CEO quit, the stock tanked. And the street was saying - Oh, who can fill his shoes. And then the new CEO appears to be better and the stock zoomed. Stock price volatility is a friend for people who know the long term fundamentals and does not worry about the short term sentiment.

Not sure if this business is cyclical. It looks as simple as a business can get. As long as penetration has room to improve, all they have to do is increase distribution reach and garner funds…

Which are the most secular kind of businesses? FMCG I guess? They keep growing at a steady rate while sometimes have flat numbers due to external shocks, most recent ones being GST where most FMCG cos had flat/declining volume&PAT. AMC also displaying the same characteristics I feel. Once in a while, when the market is down, PAT may be flat or fall by a small % in the worst case.

These AMC businesses display very similar characteristics… High ROCEs, no capex requirements hence no debts, high dividend payouts…

I’m a rookie to investing, so please correct me if I’m wrong on my assumptions.

One difference which I could see in fmcg and AMC business is that fmcg products r essential part of daily life of each class of people while AMC for those who have good income ,savings and understand this option of investment

The other debate i see hear is that this Stock must be bought at the height of a bear market… IMV - such statements are applicable to all stocks… Not just AMCs…

The issue though are some of the follg questions.

how sure are we that AMCs will fall more than other stocks… There is no history to it… In fact there is history of data that HDFC AMC kept increasing its profits even in the worst bear markets of 2009 and in 2013.

who can say - here and now we are at the worst part of the bear markets… Nobody…

This event must be monitored closely as it might shake the system and hit confidence of debt fund investors. This looks like a classic case of asset liability mismatch.

Peter Lynch was a great Fund manager at Fidelity. He left in late 80s with a track record better than even Buffett in those years. That didn’t stop Fidelity juggernaut. People are important but this business is also about trust. They will be able to find the right people. Nobody is irreplaceable.

Please correct me if i am wrong. I think HDFC life Insurance also includes AMC apart from insurance. For their AMC, no restrictions on charges. They will have lot of exit load also for any discontinued insurance plans. Isn’t it better to own insurance company than pure AMC…

No. Life Insurance business of HDFC does not include any AMC. They sell ULIPs though. Also the NPS business, HDFC Pension Fund, is the subsidiary of HDFC Life.

Both are two different businesses and isn’t quite comparable.

financialisation of Savings ( the cagr growth was during the regime of large part of savings going to gold and RE). Now with formalisation of the economy. Mfs are to gain.

HDFC/SBI as a brand is well positioned to capture this growth due to brand value. They dont need superior returns but consistent decent returns. Large part of rural investors hardly invest basis detailed return analysis.

There is huge tailwind for the business

HDFC/SBI as brands if they maintain the simple format and do no nonsense products they are set to gain significantly in this tailwind.

Huge operating leverage is available(the costs are very low)

Lets look at no of increased distributors, direct to invest websites (fintech ones) . All these will be benefiting the business.

All the positives that one can identify in HDFC AMC are more or less present in Reliance Nippon AMC as well. The macro tailwind, increased financial savings, strong distribution, very high expected ROIC and the range of products on offer

Are those of you who are very bullish prospects of HDFC AMC equally (or proportionately) bullish on Reliance Nippon AMC as well? In terms of scale RMF is a top 5 player and top 3 in terms of profitability. They have some very good fund managers as well on the MF side and are probably ahead of the game in the PMS/AIF segments that cater to the affluent and the HNI segments.

Isn’t the difference in valuation accorded to the two an anomaly? HDFC AMC is valued at 34,000 Cr while Reliance Nippon is valued at 13,700 Cr. PAT of 721 Cr Vs PAT of 505 Cr for FY18

Even if one were to adjust for the promoter premium, why should Reliance Nippon trade at a 60% discount to HDFC AMC? All the tailwinds that work in favor of HDFC AMC should logically work well for Reliance Nippon AMC as well

Unless one has a tangible and logical answer to the above questions, my guess is one may just be getting carried away based on intangibles - this might end up being the correct decision for all you know, but are you comfortable paying a significant premium when you have an equally impressive franchise trading at 40% of the market value?

I have nothing in favor of or against HDFC AMC, I am just trying to ask some pertinent questions and probe why the market is so bullish on HDFC AMC at this point of time.

It is just track record of Reliance ADAG group of failing/poorly performing with all biz vs HDFC track record of impeccable capital allocation and wealth creation. No comparison…

Is that worth a 50% discount? Especially when each AMC is structured as a trust with each unit holder treated as a beneficiary? The regulations are very strong in the sense that siphoning money out of an MF is next to impossible

Capital allocation in an AMC business should matter lesser than in a normal business, this is a business that needs minimal incremental capital anyway. This is not a lending business or a bank where capital allocation is extremely important and you run the risk of capital erosion due to bad judgement by the promoters. Reliance Capital and Nippon hold an equal amount of stake, Nippon is one of the largest players in asset management business worldwide and should be able to be a watchdog in a lot of ways.

I still can’t wrap my head around why HDFC AMC should trade at such a steep premium. As a distributor I was equally comfortable with either AMC and so were investors/customers.

If I go by purely by the numbers and competitive position Reliance Nippon looks like a better buy compared to HDFC AMC at current market cap.

You can not quantify it so easily. But if you think long term, premium starts making sense. Premium always persists when established. People who paid premium for leader always made more money than those betting on followers assuming that premium will shrink. In 90% of scenarios leader did well to justify the premium.

Regulations can not change character. Aren’t all banks regulated by same RBI.

Sir, i think you just highlighted beauty of this business that any management can run with ease. Reading your comments i feel a strong franchise like hdfc deserves the premium valuation it is getting…

One basic question i am asking again as i didnt get answer earlier…can an AMC earn from the float until it invests that money, just like an insurance company? Is there any regulations behind it? Cash percentage is defined in all funds…does amc earn from such cash which it wants to hold for a more opportune time amd invest it for time being not as part of nav but for itself?

No, the money belongs to the unit holder and is invested with him/her as the beneficiary. Cash does earn something but all of that goes to the unit holder.

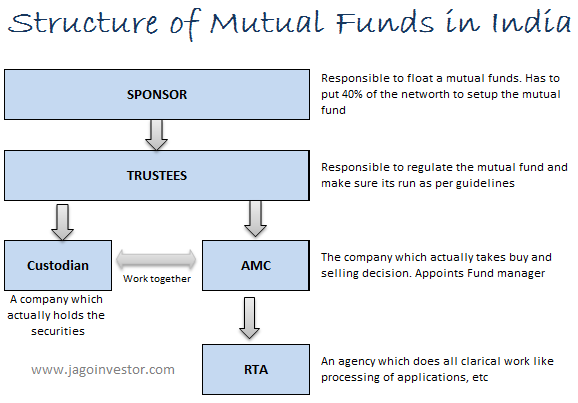

Which is why I suggest that everyone needs to understand the structure of an AMC better, it is not like any other company which has the flexibility to do what it wants once the money comes on the books.

To explain this better -

When one makes an investment transaction with any AMC, you choose a particular fund and a particular folio. Each folio defines the beneficiary structure - single holding, joint holding etc. The moment the money hits the bank account of the AMC, he invests the money on the unit holder’s behalf and there is no way he can use it for any other purpose - this is because a Mutual Fund is a Trust.

The trustees in turn appoint the AMC to manage the investment decision, a custodian to keep the securities secure and a registrar to manage the book keeping (essentially the mapping of which unit holder holds what mutual fund etc). What is getting listed here is the Asset Management Company which in turn appoints the fund managers to take decisions.

Accounting happens at 2 layers here -

Registrar and Transfer agent which is an independent body (Karvy, CAMS) that does the application processing and allotment of units once a unitholder makes a transaction. The securities are then held by a custodian and not by the AMC

Accounting of the AMC as a company, this happens in house as is the case with any other company

The AMC can invest the profits that it generates for itself, any money that belongs to the unit holder stays in the name of the unit holder only and never gets onto the books of the AMC. For this very reason, NAV allotment has to mandatorily happen as long the money gets transferred to the bank account within a cut off time.

As you can now see, siphoning off unit holders money is next to impossible due to the way MF’s have been structured and regulated. Most corporate governance issues are taken care of this way - this is regarding the unit holder’s money or as well call AUM. The money that AMC has generated from profits can be deployed for various uses like - investing in technology, paying higher distributor commissions, lending to a group company etc. I think those are the regulations one wants to study from a corporate governance and capital allocation point of view

I had similar questions when Hdfc AMC listed.The answer lies in the last 10 years how much of wealth created by Reliance Capital vs HDFC.Market always pays a premium/discount based on past perf.

This is hypothetical situation to stress importance of ethical management

Suppose X company promoter meet the AMC fund manager to inflate there stock prices , AMC fund manager with having handsome amount of AUM can (legally) do some favour to X company

For me to buy any business ethical promoters is first step and willing to pay some reasonable premium for that

There is difference between strict regulation and Ethical mind-set

Thanks

Ashit

The issue is not money that makes the AUM, the issue is the fees collected by the AMC that underlie its profits. With the track record of stealing investors money that ADAG group has, I would never even mention it in the same breath as HDFC for comparing. You would see excel sheet profits one day, and gaping holes another. You would never sleep easy. Just see what happened to RCOM vs. peers. That corp gov culture deserves a steep haircut.