I have edited @Yogesh_s model. I dont see the stock being downgraded in 10 years. If at all what we have seen it could maintain the same PE or even be rerated upwards considering the history of blue chip consistent performing stocks in past decades of indian markets.

Similarly i dont see the growth rate coming down anytime soon. If HDFC Ltd and Bank can grow 20+% in last few decades, this business is as much as nascent stage as they were few decades back.

Those wanting to buy cheap, should remember india gives high PE to even moderate growth stories, and waiting to time the well discovered stock keeps one waiting probably for life. We cant miss opportunities thinking the tide will turn and india markets will behave differently for blue chips compared to history. Let it turn, then we shall see. At the moment the optimists and pessimistic are only making guesses, only time will tell what happens. Returns Calc_Revised.xls (29 KB)

I think you’re falling into confirmation bias here. Just because you’ve taken a stand on this stock, you are looking for or citing evidence that supports that stand. Clearly, any astute long time observer will tell you that the MF fund with one of the best long term track record going back 20+ years is HDFC. It is but natural that funds that are in the top decile spend time in lower deciles sooner or later - its in the nature of value investing. Most funds in the West with the best 10 year track records, spend atleast 2-3 years in the lowest deciles.

Secondly, it is being myopic to focus obsessively at valuation in the early stages of a market opportunity. This is not even a mid innings for this category. Indian economy is $2.6 trillion now and MF industry is but $350bn. Like west, at some point, it will be closer to 100% of GDP, when the economy itself is closer to $7-8trillion in 15-20 years. HDFC AMC itself could be a 1$ trn+ AMC by then. At 8% of AUM, the business could well be worth $80Bn or nearly 15x from here. DCF is a poor tool when most of the value lies in terminal years and it is a poor tool in an economy where discount rates will progressively fall over time as it develops (you should discount future CFs with discount rates materially lower as years progress). To use a tool well, it is important to know its limitations.

It was known that most of the HDFC schemes are underperforming but market gave a premium listing. I feel that this is a healthy correction to be bought into. What is obvious needs to be discounted and in that sense, underperformance is obvious. Where HDFC AMC might be better is their overall expense ratio among other funds due to average AUM, lineage, scarcity premium (which might still sustain after the listing of ICICI). Investors have not discarded this inspite of a long underperformance.

Thought regarding banks and AMCs during recessions:

It is true that AMCs get doubly hit in a bear market- lower notional value of AuM plus potential outflows however one needs to keep in mind that unlike banks this does not pose an existential risk to the business itself as Long as their fee income is able to support their operations, a very likely scenario barring the next depression.

For banks though, It is a completely different ball game no matter how good they are, in a prolonged recession NPAs pile up across sectors putting a serious strain on the equity base, the bank either has to be bailed out or capital raising needs to be done with huge dilution, both options highly damaging to equity holders.

Do some research on how even the best banks fared during the Asian crisis to understand why you would be far better off with HDFC AMC rather than HDFC bank during prolonged recessions.

It seems you are focused on long term secular opportunity and ignoring medium term cyclical pressures that will inevitably come with next bear market, whenever it happens (especially since AMC business is vulnerable to market whims). The whole idea is to buy the business when it is undervalued by good margin. Obviously, one needs to have patience and wait for such opportunity.

Besides, buying now and riding through bear market roller coaster looks easy but extremely difficult in practice and, also it creates psychological barrier in adding capital, precisely at a point when one should be adding capital and not just watching.

Fair points. We need to wait for a market cycle with significant downwards and sideways movement to see how this stock/ business reacts and responds to that.

Also, we should not over emphasise the parentage as a moat or something that will enable it to fare better. Yes HDFC/ HDFC Bank are bellwethers for the market. Does not mean the AMC will be as well…

This isn’t a business with no history of surviving a downcycle. It was incorporated in 1999. It has seen, survived and flourished over more bear markets than most people on this thread or board. And yet most of the great years still lie ahead.

I see the same sort of arguments on every expensive but quality company thread. The facts that need to be acknowledged are that these are quality companies without a doubt and also the fact that they are expensive as well, without a doubt. I see the ones that have made up their mind on the expensive valuation trying to talk down the quality (especially moat) of the business and the ones convinced of the quality and hence invested with probably a longer-term horizon trying to imply that valuations don’t matter as the runway is long. Both are right and wrong unfortunately.

An AMC business will grow as its AUM grows which can happen when savings in financial instruments grow, and/or the company is able to capture a larger market share and/or the company is able to improve its expense ratios. There is a good probability that HDFC AMC can pull-off the second but the third could be under regulation while the first will inevitably grow in AMC’s favour. These are all of course longer term events.

In the short-term however, lets not forget the massive bull market in the last few years which has caused a significant increase in AUM. In a bear market, AUMs could take a mark-down along with inflows decreasing and outflows increasing causing a negative lollapalooza as well. Also, there is a reason why a lot of IPOs happened around the last few months. Some cyclical businesses debuted at peak earnings, some average businesses were sold at insane valuations etc. All that mattered was a good story, marketing spends and the IPOs were marketed like blockbuster movies - A lot of IPOs have ended up much lower than listing price - Be it Apex frozen foods, Vadivaarhe, Silly monks, Advanced Enzymes, Hudco, CDSL, ICICI Securities, BSE etc etc. For every Avenue Supermarts, there are a handful of these expensive businesses which didn’t make it.

Businesses whose recent fortunes were tied to the bull market like CDSL, BSE and ICICI Securities have done poorly, probably because the market expects their earnings to moderate in the current year and probably next few which will make them cheap. I think this is what is ailing HDFC AMC as well going by the similarities in price-action where there is significant post-IPO offloading but due to this being the fag end of the bull market, there isn’t enough buying power to absorb such large blocks, making it look like a falling knife. I have made up my mind to stay away, just as I did with Avenue Supermarts because I can’t sleep peacefully paying these valuations but that doesn’t make these bad businesses by any stretch.

These rankings are based on Fund Manager performances. If we narrow down to the Large Cap universe (imo those will be usually benchmarked to Nifty50 and a reflector of overall market) then the top 5 managers who are listed in this have actually not seen as much compared to say Prashant Jain of HDFC.

Neelesh of Mirae: Mirae launched its flagship India Opportunities (now called India Equity) in April 2008 then Neelesh started managing Emerging BlueChip in July 2010. Their returns since inception has been roughly 17% and an excellent 27% respectively.

Harsha Upadhyaya of Kotak: He is a seasoned guy with his fund management starting in 2006 with UTI, then DSP and now Kotak. He currently manages equity opportunities fund since 2012 which was launched in 2004 and the earliest fund of Kotak was launched in 1998. This fund has returned ~19%.

Sohini Andani of SBI: She has been with SBI from late 2007. SBI launched 2 equity funds in the early 90s - Magnum Multiplier and Magnum Equity both she never managed. She manages Bluechip Equity which was launched in 2006 and has given a very poor return of 12% since inception. She took over the fund in 2010. She also took over Magnum Midcap in 2010 which has given a 16% return.

Sailesh Raj Bhan of Reliance: Reliance launched its growth and vision fund in 1995 which have given a good 22% and 19% returns respectively since inception. Sailesh manages Large Cap which has given a poor <12% return since 2007 and multi cap fund since 2005 which has given 18% since inception.

Mahesh Patil of Aditya Birla: ABSL launched one equity fund in 1995 which has given 18% since inception. Mahesh has not managed this. He has managed Frontline Equity which has given a good 21% since inception (2002) from 2005 onwards. He also manages Focussed Equity from 2010 onwards which was launched in 2005 and has given a mere <15%. His third open equity fund is Pure Value fund which he took over in 2014, this has given 18% since inception in 2008.

Now if we look at Prashant Jain and HDFC. HDFC launched 4 equity funds in or before 1996 - Capital Builder (15% since inception), Large Cap (a poor 12%), Equity launched in 1995 (19%) and Top 200 (20%) in 1996. Prashant has managed Top 200 from Jan 2002 onwards and Equity Fund from Jan 2003. HDFC has perhaps had the most equity funds running from the mid 90s onwards. Reliance, SBI and ABSL have had either 1 or 2 equity funds running before 1996. So as a company HDFC would have had more exposure to market cycles to their equity funds. HDFC Equity and MidCap are the largest Equity funds followed by Kotak Select Focus and then ABSL Frontline and then SBI BlueChip. A professional like Prashant Jain has seen the markets in a fund manager’s hat more than all the top 5 chaps.

An interesting article earlier this year in Morningstar says this about him

The funds managed by Prashant Jain will most probably run into rough weather this year as bank stocks falter. Also, the funds now infamously court more risk than a typical category peer. Over a 5-year period, the standard deviation of HDFC Equity (18.24%) and HDFC Top 200 (17.37) is significantly higher than the category average (14.24%). As mentioned above, his investments are made keeping in mind his perception of the next cycle. In various interactions, he has always emphasized that “when the market is moving from one theme to the other, you have to let go of your winning bets and buy something that is promising for the future. Till the time this works out, performance suffers.” We are not underplaying that, but would like to point out to his affinity for bank stocks. It was his investments in public sector banks which led to significant under performance in 2013 and 2015. While we still maintain that he is a steady fund manager when it comes to adhering to his investing style and mandate, and stand behind our Gold rating, in the short run, and this year specifically, his funds could be headed for a bumpy ride.

I guess he wouldn’t have made the cut in this because of the risk returns criteria.

Also imho Buyers and Sellers trade/invest with what they know and even if they know all the facts (which I doubt they do) do they value the facts similarly? My first level thoughts. I agree with @varun037 that if all facts were known to the decimal objectively by each participant then I doubt any trade would exist.This sounds like efficient market hypothesis to me. There is no doubt HDFC AMC is quite pricey and that is the reason most of us if we have invested or evaluating to invest would have just taken tracker positions. Like the way @phreakv6 has put the three ways in which HDFC can do well wrt to competitors and things which could not be in their control.

In India most financial products are sold and not a “pulled”. I don’t think it is ONLY due to fund manager track record HDFC mutual fund is having large market share. Most of the Hdfc mf investors wouldnot know/matter who’s the fund manager. This is largely due large distributor reach and brand they have dominant position. (Same as LIC in insurance). As long brand and trust is not shaken it is likely to keep market share.

While investors keep arguing about valuation and quality, employees are voting with their feet almost on a daily basis. I have not seen such rush for exit so soon in a supposedly promising company. I hope they know their industry better and not missing out on long term value creation. I have no doubt in my mind that this is a great company but will face significant cyclical and structural issues going forward.

AMC setup will find it difficult to attract start talent and retain them since AIF structure is significantly more remunerative for a star manager.

Clamp down on expense ratio

Big banks (SBI, ICICI, HDFC etc) are being accused of pushing common mass into their own funds irrespective of performance or suitability. There will be some kind of RBI regulation on this sooner than later.

This company can’t be compared with Page or HDFC bank. Can it deploy its capital to generate or grow profits ? Even dividends will be volatile in the long term.

Index funds will remain a long term threat as more and more folks will realise that it is not worth paying 2% for an additional 3-4% alpha. Some of these folks will shift to wealth management or AIF/PMS setup.

It is funny that the company which regularly invests in IPO priced its own IPO at 1200 but investors think it is fairly valued at 1700. I have never seen such a foolsome decision by a capital market participant in pricing its IPO. Or may be investors are fooling themselves in justifying CMP.

Disc: I will be a buyer at IPO price which should help me tide over impending cyclical weakness.

Employees selling post ipo does not mean they are short term oriented… They have held their esops may be for 10 or 15 yrs… Absolutely normal to take part of the profits at 170X in that time frame. What we don’t know is how much more shares they are still hoarding without selling.

Even now, every now and then, Hdfc Bank employees keep selling their esop shares in tens of thousands… Do they think Hdfc Bank has no future… And the markets accepts those shares happily…

Routine profit booking which is a fortune of their lifetime by employees can never be considered a negative…

Dmart was priced at Rs 300… By same logic, Mr. Damani does not know how to value his own company…

I am not saying the company is not overvalued. Everyone has his own risk perception and return requirements. If I am satisfied with 10% with minimal risk, I may buy company X while someone else may not. It is very personal in nature. Time horizon also matters much. Over a short period one company may not be a good investment but over a bigger period, it may become investment worthy. Some may want to time the market, some may not.

Everyone is saying it is overvalued or undervalued without any supporting calculations… I agree with @Yogesh_s matrix. It is a good what-if table and is helpful in checking quick opportunities. There are ample examples where overvalued stocks have performed and where they have not.

I would say HDFC AMC is a great business, cash cow… Very good return ratios. Their payout ratio is good.

Why I think it is better than other AMCs is because of parentage of HDFC Bank. They have people’s trust. After all, you are not going to give your money to anyone to manage. Their establishment cost is low. Whenever HDFC Bank opens a branch, HDFC AMC automatically gets a new sales point.

With expanding digital reach and markets, I see a huge opportunity to tap. I do not see a reason, why after 10 years, the asset management business cannot be 3-4 times the current market size. The direct funds are more beneficial to customers and asset management companies as well.

Currently, ICICI AMC is the largest, but ongoing issues with their MD and some miss-selling of ICICI Pru schemes, ICICI group’s reputation may have taken a beating. Add to this, huge investments in ICICI Securities leading to losses and then refunds to customers.

I personally feel that HDFC AMC should gain out of this also.

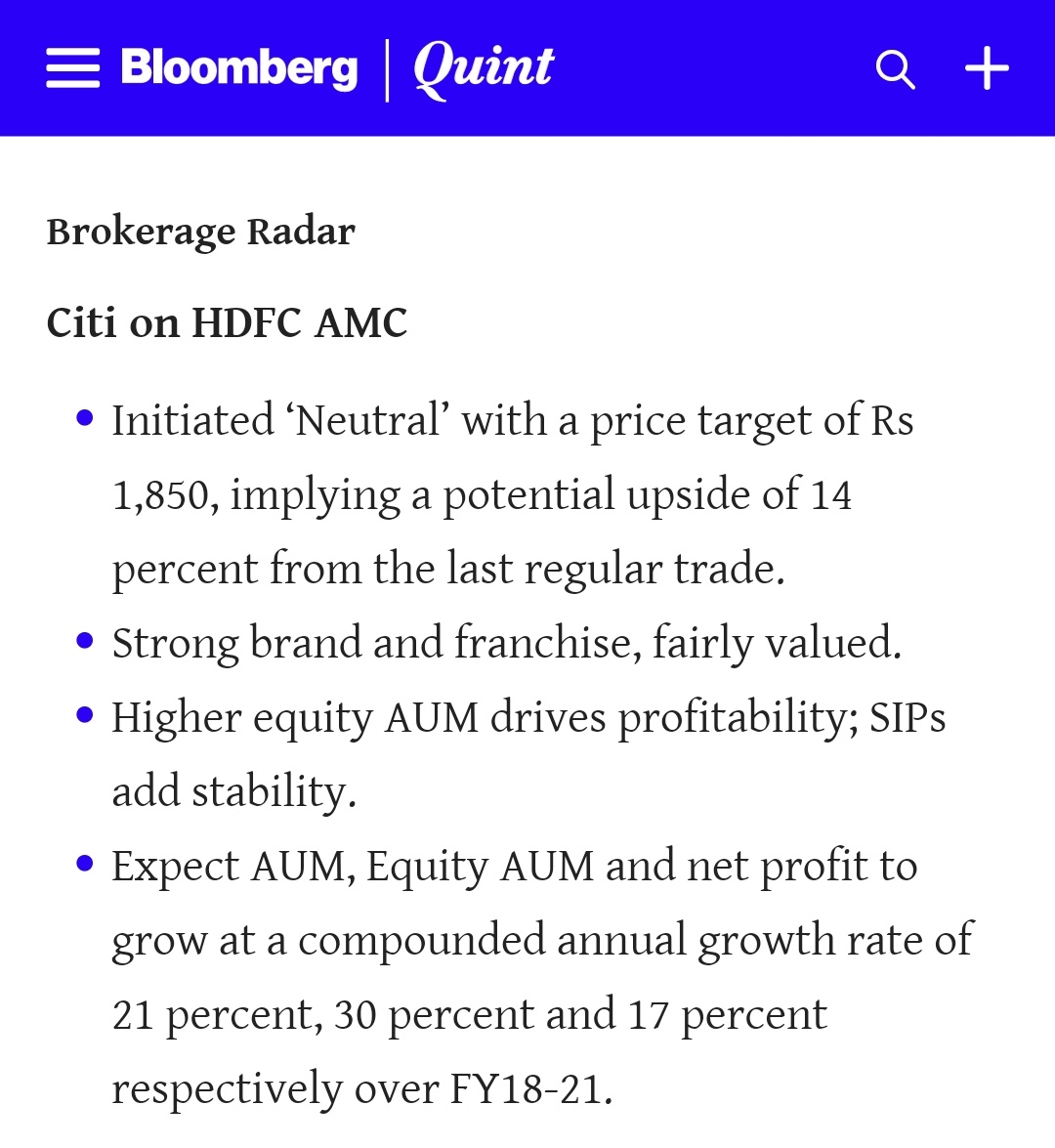

A basic question, but reading the last point from the image

Expect AUM, Equity AUM and net profit to grow at a compounded annual growth rate of 21 percent, 30 percent and 17 percent respectively over FY18-21.

If AUM growth is expected at 21/30% why is net profit growth only at 17%? Wasnt AMC business all about scale and operating leverage? What will be factors driving net profit to grow slower than the AMC growth?

Ok I think got the answer - they expect the Expense ratios to go lower from here on over next few years.

Looks like we are going down the same route of judgement on whether CMP indicates overvaluation or undervaluation (I don’t see anyone citing undervaluation). While this argument can continue eternally, how about the following scenario materializing? Would your investment hypothesis change materially?

Prashant Jain decides that he has had enough of managing a very large AMC and decides to run his own fund to rediscover the joy of money management. Now that he has more or less had his exit doors opened after the listing, he might as well take his 150+ Cr and walk.

My big grouse with HDFC AMC was always the larger than life persona of their CIO, he himself manages more than 50,000 Cr of equity money. So when his investment style goes out of favor, all their leading funds suffer - HDFC Equity, HDFC Top 200 (before the name change). If I were to compare this with say an ICICI Pru AMC, Naren S is the CIO but the funds are managed by different people. So the risk of someone exiting does not impact them all that much. I remember many of my customers exiting the IDFC mutual funds within a couple of weeks of Kenneth Andrade quitting IDFC AMC. The threat of Prashant Jain exiting at some point of time may be more real than one thinks right now, whenever someone gets an easy exit option the thought process completely changes (I have seen this happen in so many instances as a wealth manager)

In addition to this, one also needs to ponder -

What is the product pipeline of HDFC AMC? How does the management think about addressing the large opportunity that exists in addition to the MF route? Affluent segment is increasingly looking for differentiated solutions and there are no limits defined on the expense ratio an AIF can charge whereas MF expense ratios will always be under the scanner from here

What kind of investments are they making in technology to get a captive base of loyal customers? Some of the other AMC’s are making huge investments into digital channels

What separates HDFC AMC from other AMC’s other than the Prashant Jain factor on the equity AUM front? Strong parentage will no doubt ensure survival and relevance over a long period of time but will the competitive forces change materially if the regulator gets more active over time?

The factors for making a long term success of a company is very simple… The difficult or impossible thing to do is to implement those simple things over a long period of time… This is where very few groups or companies fail… And this is where Hdfc group stands out… It is in the DNA of the organisation…some years back, Hdfc banks high profile retail banking head quit Hdfc Bank to join stanchart or HSBC i think… Did stanchart become another Hdfc Bank… Or did Hdfc Bank went down under… It is the DNA of the organization which matters…

Yes, the risk of Prashanth Jain or anybody in Hdfc AMC leaving is possible… That possibility exists even in CEO’s of cos like page, jubilant, Titan etc leaving their Co… May be the possibilities are higher… Can anyone stop investing in them keeping such a risk in mind…

Hdfc as a group are not known to be pioneers in implementing technology at a large capex with poor Roi… Their investments are based on Roi… They don’t mind somewhat late, but be sure of capital allocation… The opposite strategy of groups like icici…

The comparison with corporates like Page and HDFC Bank are not relevant. Fund management business is a different ball game compared to any other business, the reliance on fund managers is huge. In other businesses you have teams that execute, in the AMC business the fund manager’s decision making is what keeps the motor running and determines the bulk of the fund performance. You can fire a couple of well known CEO’s today in execution heavy businesses and not much will change, not so in the case of an AMC.

Fund management business is all about the fund manager unless the AMC has actively steered clear of that approach by “corporatizing” the fund management process and mindset. This is clearly not the case with HDFC AMC on their equity AUM for the large cap and diversified categories where their reliance on Prashant Jain is huge even today. You will see countless examples of AUM’s taking a hit as soon as a star fund manager decides to move on - this is across the world.

The impact due to the fund manager leaving is much higher in HDFC AMC and not so high for other AMC’s - that is my central point. I have pitched MF to 100’s of customers, most customers who invest/stick with HDFC equity funds do so for Prashant Jain and his track record. Of course not every customer is going to redeem if he leaves but there will be a material impact for some quarters for sure in my assessment, this coming from ground up. The man’s cult status in Mumbai circles is unbelievable, Mumbai has 44% of the country’s MF AUM.

This risk cannot be quantified but one needs to think more about risk than reward when a story looks well valued. If the stock were trading at say 900 Rs, I would think more about the positives that can materialize