I happen to read (again) The Five Rules for Successful Stock Investing by Pat Dorsey who wrote about the now (ab)used term “MOAT.” He believes that AMCs are lucrative business and requires no incremental capital to run. He believes AMC have economic moat and I listing them along with my comments and opinion.

Moat and hallmarks of success of AMCs

1. Diversity

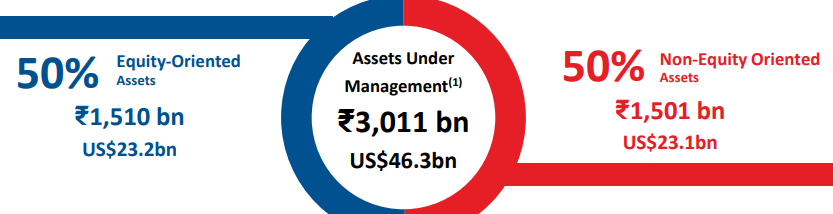

HDFC AMC does not manage only equity based assets. They also manage debt, fixed income, AIFs (including REITs & InvITs), Gold and hybrid (balanced, equity savings & multi) assets. As on June 2018, Debt AUM is 50% of total AUM.

Certain AMCs like PPFAS, Motilal Oswal and Quantum who have a much larger equity AUM will find it difficult when the equity market flatters. While they may be equity focused and it is a good thing for unit holders but it would be a double whammy for investors when market falls and because of this AUM would also fall.

AMFI’s “Mutual Funds Sahi Hai” campaign is now going to cover Debt funds soon to increase awareness among retail investors. News item: AMFI’s new campaign to focus on debt investment benefits.

Debt funds’ share in the total AUM may still fall and it is a lesser margin product but the absolute AUM of debt funds is set to increase over the years.

2. The rise of Direct plans

When we see distributors and aggregators competing among themselves to sell our product, and that too for free, then we know this is indeed a good business to own.

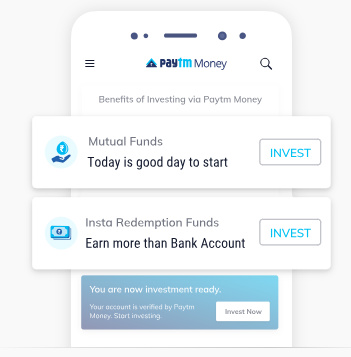

Now PayTM, Zerodha, Kuvera, ET money, etc. are offering (for now) direct plans free. If we listen to what PayTM founder said and what we read, there is going to be a big pool for new investors coming in and they are vying for assets from everyone from rickshaw pullers to corporate CEOs. PayTM wants to aims to double Mutual Fund investors in India and increase penetration in B30 centres which is good for the AMCs. If we open PayTM Money, it suggests alternatives to savings account and FDs.

Direct plans give better margins to AMCs than Regular plans thus increase in direct plans bodes well for the AMCs.

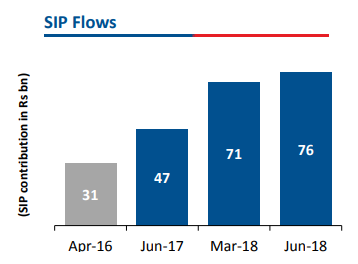

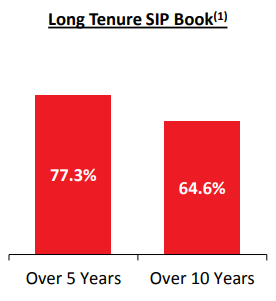

3. Sticky Assets

HDFC AMC who have a increasing SIP book, incremental SIP running for long term, buy-and-hold juntas and retirement/children funds can count on steady earnings in all market conditions.

While investors can stop the SIP, redeem existing units and might not do a fresh SIP on market downturns, nonetheless having a book SIP book is a positive and gives “AUM visibility.”

4. Market Leadership, Trusted brand and strong parentage

Economy of scale in this business is a completive advantage. Larger AMCs do not need more investments in manpower, offices, etc to manage more incremental assets and they have longer track record to show to investors which will further attract more assets. This makes it much difficult for smaller AMCs.

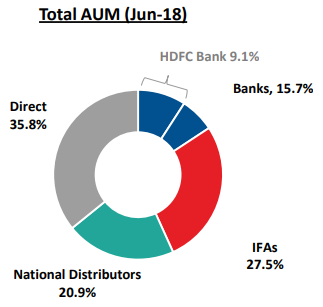

HDFC is a widely know, enhanced appeal and trusted brand which helps even further in gathering assets and manage them profitably. Having a strong parent also helps in distributing and HDFC bank alone distributing 9.1% of HDFC AMC’s total AUM as on June 2018.

HDFC AMC have been a leader in the Indian mutual fund industry as the most profitable, largest equity oriented AUM and second in the total AUM by all AMCs.

Disc: I own HDFC AMC.