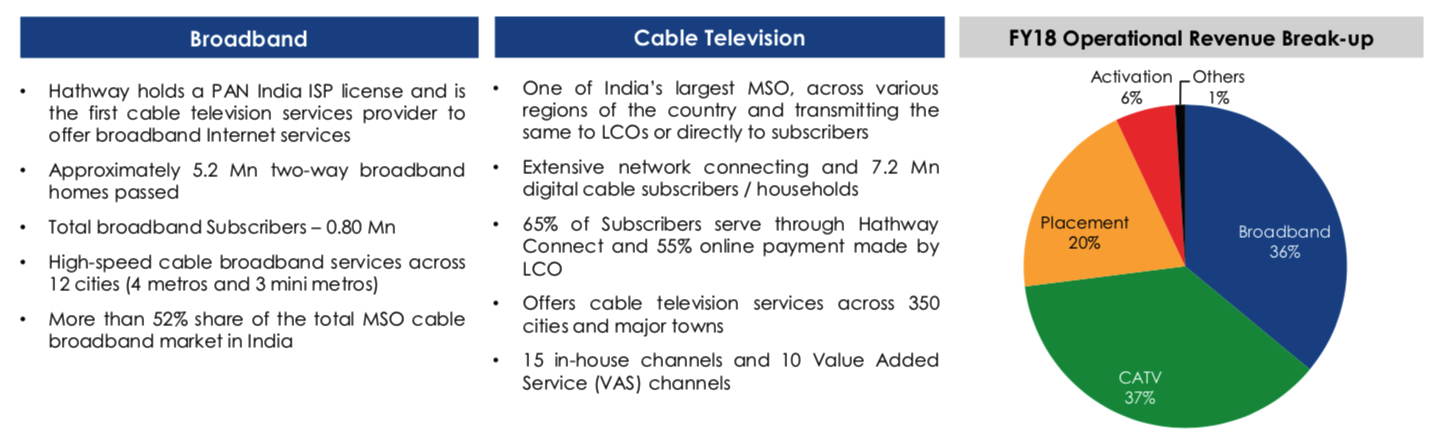

Hathway Cable & Datacom Limited (Hathway) promoted by Raheja Group, is one

of the largest Multi System Operator (MSO) & Cable Broadband service providers in

India today.

The company’s vision is to be a single point access provider, bringing into the home

and workplace a converged world of information, entertainment, and services.

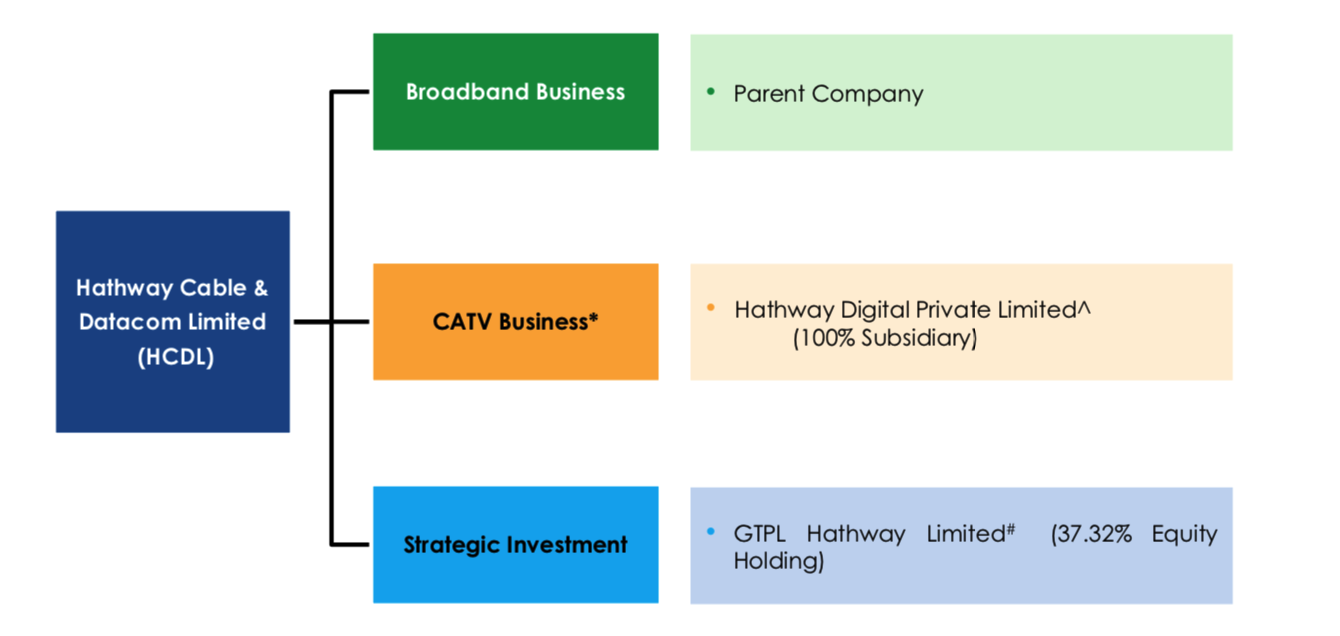

Hathway recently got demerged as per below setup:

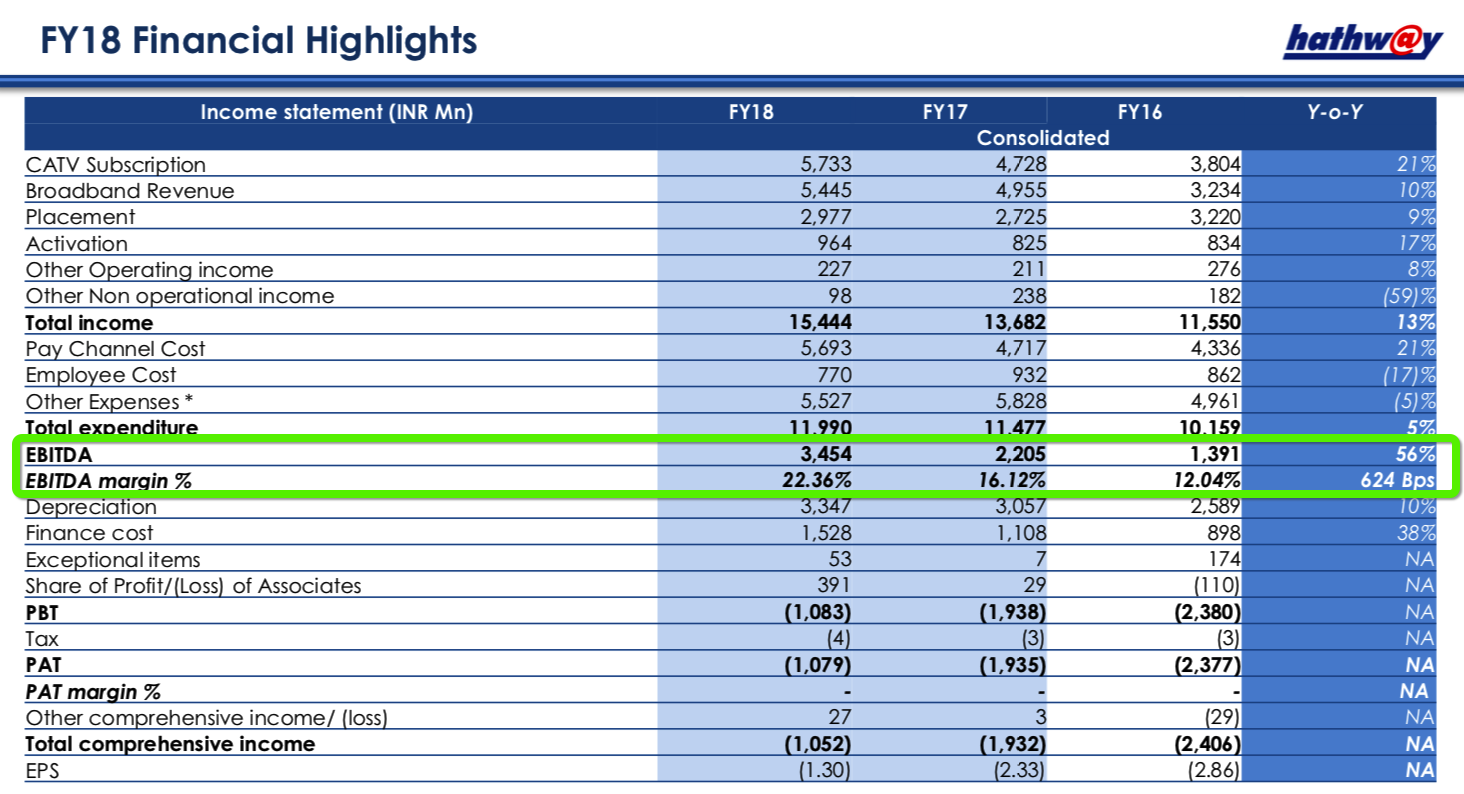

HCDL – FY18 Standalone Key Highlights:

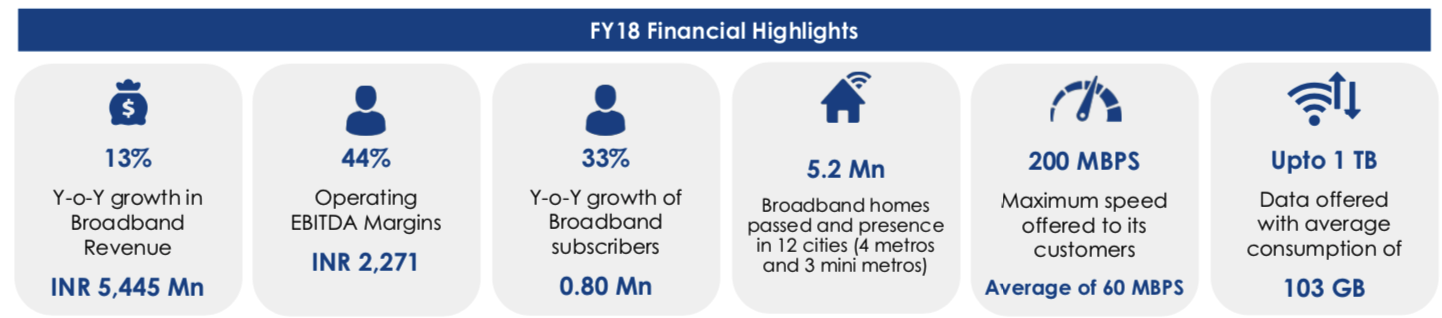

- 160k Net adds during the year (50K in Q4-FY18) with New customer ARPU of INR 720/- (Excluding Taxes)

- 0.8 Mn Homes Passes added during the year, Homes passes reached 5.2 Mn through constant focus on Network expansion

- Broadband Subscription Revenue increased by 13% Y-o-Y to INR 5,445 Mn in FY18 from INR 4,803 Mn in FY17

- Subscription Revenue increased by 5% Q-o-Q to INR 1,457 Mn in Q4-FY18 and Operating EBITDA INR 639 Mn in Q4-FY18

- Average GB / consumer / month has increased to 103 GB in the month of March. Strong indicator of demand side potential of high-speed wireline broadband.

- TCS has been appointed as System Integrator to automate various Processes and Improve Quality of Service

- In association with Microsoft 1 TB cloud storage being offered free to all yearly pay term consumers (This is initiative to protect High ARPU custmores from competition)

- Upgraded Tech infrastructure enables 50% increase in speed and 200% increase in data capacity. Opportunity to delight our consumers by offering better value for money

- Minimum data limits across country increased to 200 GB / consumer / month. 54% of our consumers have monthly data limits of 1,000 GB

- GPON FTTH Parallel network being deployed in High Potential High Penetrated Docsis home passes. Opportunity to increase market share by offering 200mbps - 500mbps speed to premium consumers

- • Docsis 3.0 technology to Docsis 3.1 technology upgradation work in progress to further enhance customer experience. Docsis 3.1 is the latest global technology for offering high speed broadband over cable

HDPL – FY18 Standalone Key Highlights

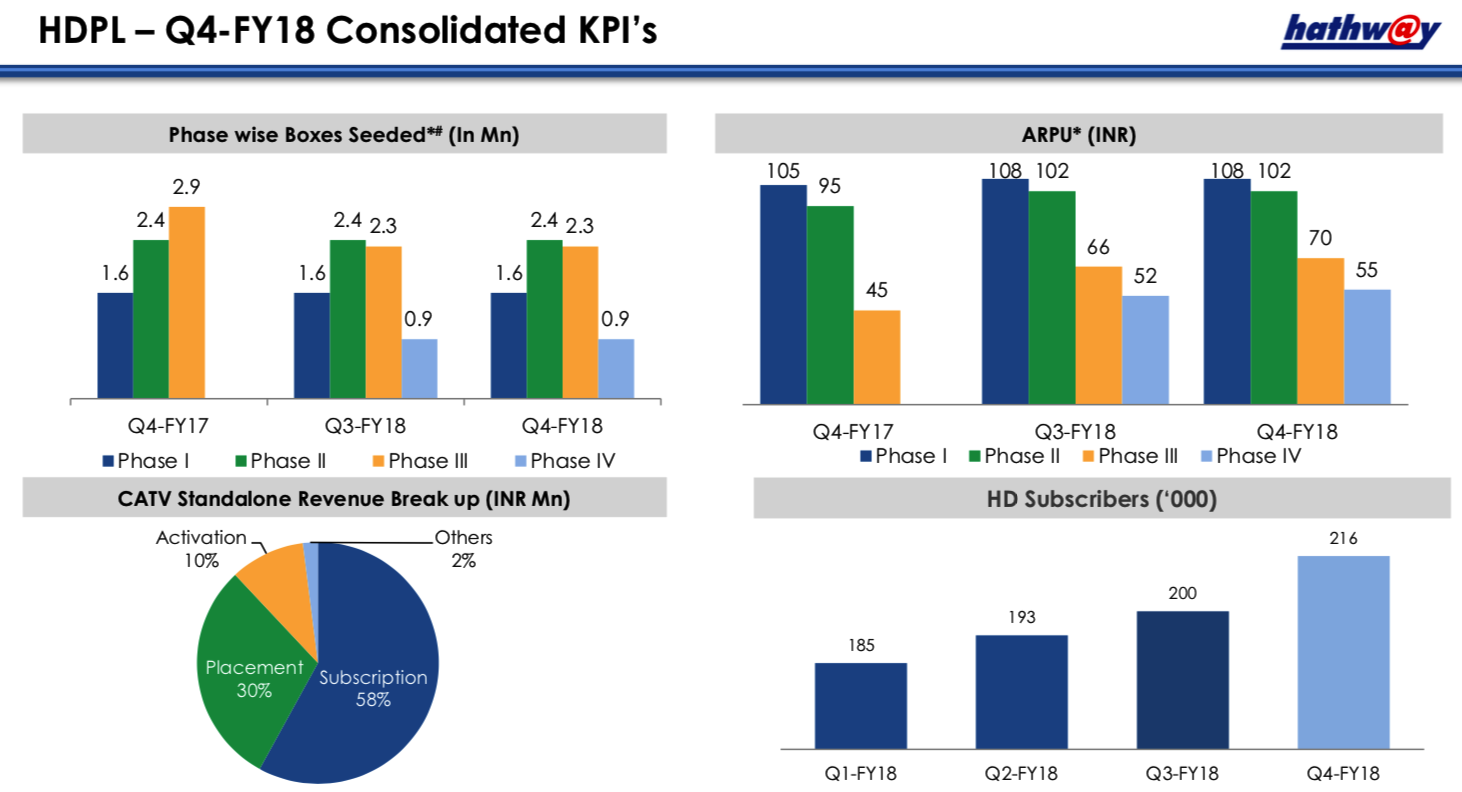

- Consolidated CATV Subscription Revenue increase by 21% to INR 5,734 Mn from 4,728 Mn in FY17

- Standalone Subscription Revenue continues to grow by 3% to INR 1,526 Mn in Q4-FY18 from INR 1,483 Mn in Q3-FY18

- Standalone Operating EBITDA increased by 11% Q-o-Q to INR 401 Mn in Q4-FY18 from INR 360 Mn in Q3-FY18

- Collections have grown by 5% QoQ and 24% YoY demonstrating strong improvement in efficiency. Q4-FY18 Collection efficiency is at 98%

- Effective monetization have resulted in significant ARPU increase: Phase I INR 108/-, Phase II INR 102/-, Phase III INR 70/-, Phase IV INR 55/-

- Hathway Connect penetration reached to 2/3rd of our base in Q3-FY18 with 55% of online payment by LCO(local cable operator) assuring stable growth in business

Overall: Financials & Balance Sheet

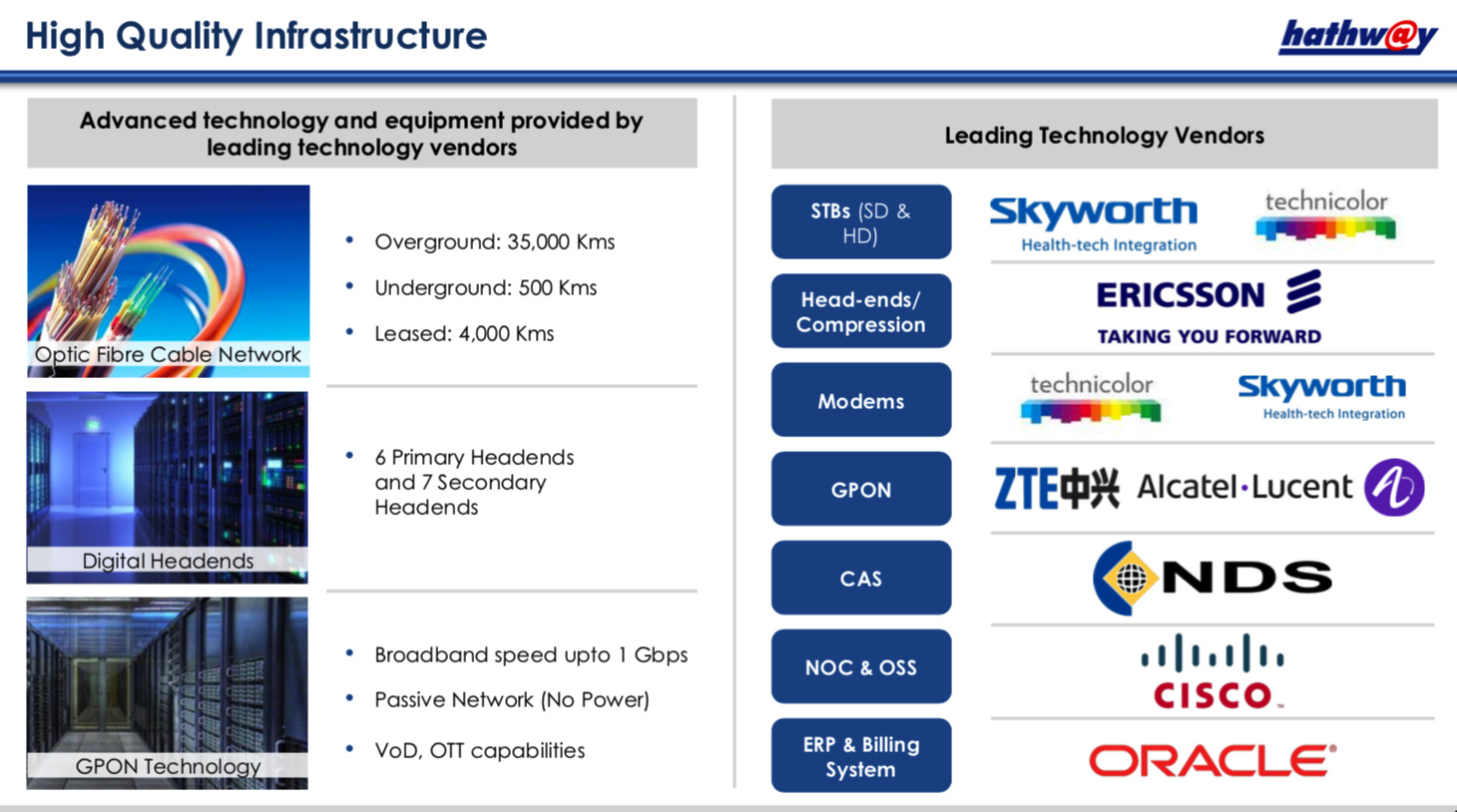

Thoughts on their Network Setup:

As I am from the same field and I understand network architecture, to my understanding they have a very well structured network, specially GPON(Passive Network).

Fiber Networks are of basically 2 types: Active & Passive.

- Active networks need electricity throughout the network, hence hight running cost & more point of failures.

- Passive networks need electricity only from starting and receiving devices.

Passive networks(GPON) are low cost to operate and provide higher availability, but the main drawback of passive is its hard to troubleshoot in case of failure.

For India, specifically passive networks are better suited, as electricity supply is not reliable.

rest for more details refer below link.

rest all other networks vendors are reputed and recently they appointed TCS as principle integrator also work in progress with Microsoft for their CMS.

Managment Guidance on key points

As per the management Guidance from attached concall, management had stated that company won’t go for expansion beyond current cities, as it doesn’t make economic sense to venture in low ARPU area with high initial costs, rather they will expand in existing major cities where they already did the capex and have a lot of room to grow.

On Cost Reduction:

“In Q1 concall, I have shared with you all full year plan of saving Rs.50 Crores in non- content costs put together for both HDPL and HCDL. I am happy to share plan is on track and we have achieved our target for Q3.”

On Subscriber Chrun

The churn currently for the broadband is around 1.5% month-on-month.

On Content cost:

Content cost, so currently negotiations are going on with the most of the broadcasters, so I think it is premature to comment upon that, but industry wide there is a general consensus that content cost will increase by around 10%, but we are yet to close on that.

Focus on Customer delight(protecting them from churn to competition) rather on ARPU:

currently as you see without increasing ARPU we are delighting consumers by giving more and more GBs and to be very frank Sanjay, we also do not see need for increase APRU currently with the kind of EBITDA margins we have and they are continuously growing, I think the focus has to be on ring-fencing consumer by delighting them rather than looking for an ARPU increase, but yes in future when consumers are used to much higher monthly data limits there is a case for ARPU increase.

Future readiness

this year was all about build up for the future, so last nine months we have been updating each quarter that we are doing lot of things to make sure the business model is sustainable for the next three to five years, which means we have added capacity in the data center, when we say data centre that is a generic term that involves a lot of our infra to make sure we are able to give each and every consumer more than 200 GB of monthly data limits, for many consumers going up to 1000 GB, so essentially we are saying there is a lot of one-time capex, which we have incurred and you know we could have avoided that, but the idea is to build up the business for the future and specifically business which is so attractive in terms and EBITDA and ROIs, so if you see when we have mentioned that kind of capex we also mentioned lets model on 40% EBITDA, but currently already the EBITDA levels ,even if leave aside the non-operating income, they will reach more than 44%, also the EBITDA have been higher than projected then such a scenario it is good to invest for the future that is what exactly we have done.

Last concall: Q3 FY18

Hathway_Q3FY18 Concall transcript.pdf (364.7 KB)

One on one discussion with Jagdish Kumar M D & CEO, Hathway, although its bit old interview but still useful to understand business dynamics.

One on one discussion with Jagdish Kumar M D & CEO, Hathway - YouTube.

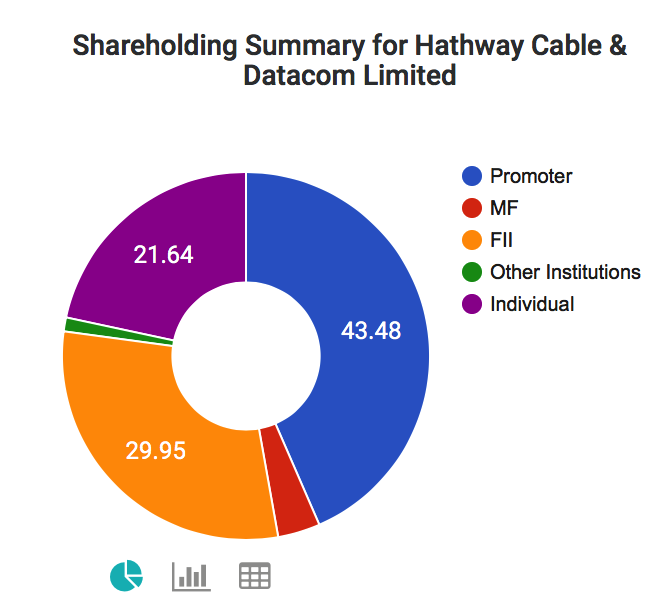

Shareholding:

Notable investors:

- On 19th April 2018, his Old Bridge Capital PMS Fund(Managed by Kenneth Andrade) bought 164,58,492 shares at Rs. 39.50 each

- In last quarter Akash Bhanshali name appeared in the 1%+

Valuations

As per Kenneth Andrade from a price point and from a replacement cycle also, the company is trading at virtually replacement cost, and I am buying his argument.

rest below are key ratio’s, which are generally used to value a telecom or ISP company.

Price to Cash Flow: 7.62

EVEBITDA: 12.72

I also took comfort as the stock price is near all-time low also 52 weeks low.

Investment Rational:

-

Company already done with major CapEx phase and current CapEx is sufficient for next 3-5 years of growth, as per management.

-

EBITDA margins are continuously improving despite Jio’s freebies in last 2-3 years.

-

Cost is falling, due to efficiency measures, automation and continuous improvement in process, implemented best in class billing system, dunning process, for ex: for Digital Tv LCO can bar subscriber with delayed payment with a click on mobile, once payment is a collected, immediately connection can be enabled from LCO mobile.

-

Uptrend in online payments, 70% of the broadband payments are online and for TV more than 50% of payments are online.

-

High margin in the broadband business, which gives enough room to compete with new disruptive entrant like Jio.

-

Broadband business is more sticky than the mobile handset.

-

Broadband Penetration going to increase over time, as data consumption habits are rapidly growing.

-

As per Ericsson’s mobility report for India, data consumption is going to grow roughly 8 times from 2017 to 2023.

-

The rise of OTT, streaming consumption will push the high-end user’s from Mobile to the stable Broadband connection.

-

Rest I feel after Jio disruption, no other big player would be investing in India for data/broadband.

So if supply is limited, and demand is robust, at some point demand should takeover supply and survivors would get profitable growth. -

One of the main reason I think broadband business is better in comparison to telecom is that: telecom has too many dying revenue streams but they have mandatory maintenance capex for all such dying services.

for ex: Roaming Revenue(local + International) + SMS + Interconnect + Even local Voice

all these revenue streams are being eaten by Whatsup & other digital apps.

Data is the only saving grace for telecom operators and Broadband service are focused only on data, also service quality of a broadband is much better than mobile. -

Regarding Digital cable Tv business, growth is fine(14% in revenue), as all the 4 phases of digitization mandated by Govt of India is complete, now ARPU is in an uptrend as well.

Key Risks: Competition

https://www.bloomberg.com/news/articles/2018-04-12/reliance-may-roil-broadband-next-as-clsa-sees-valuation-boost

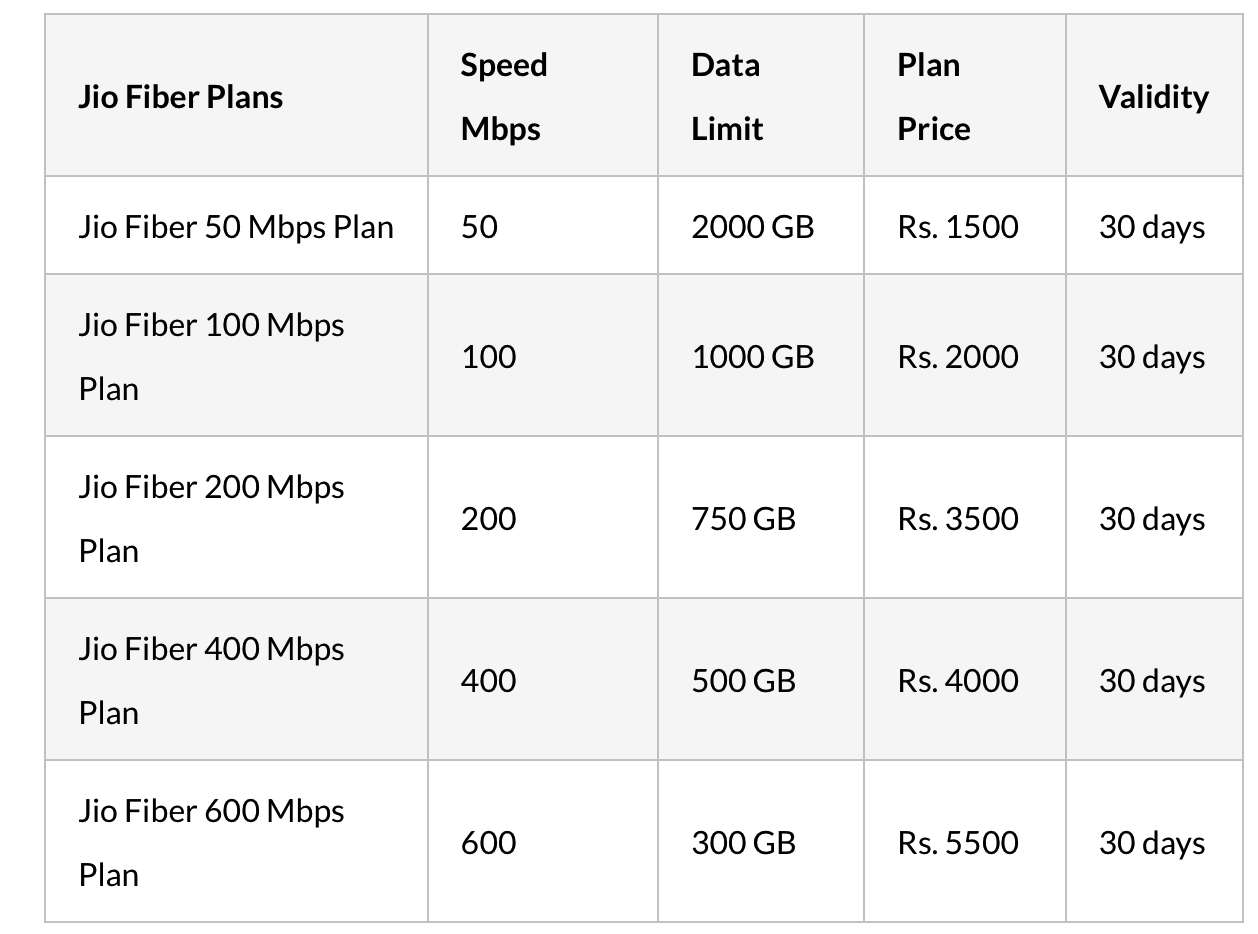

https://jiofiber.co.in/jio-fiber-plans.

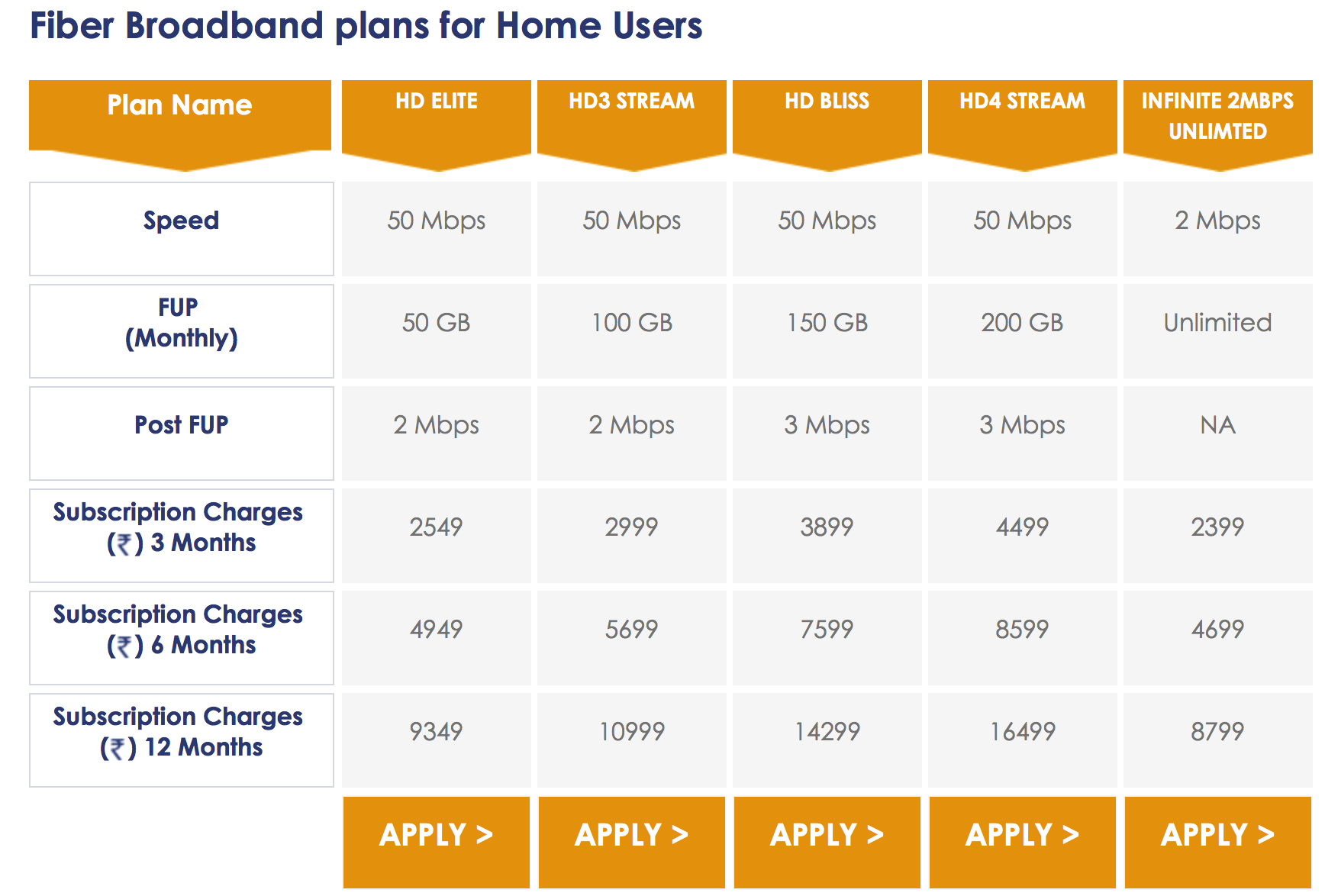

however upon checking the mentioned pricing of both Jio Broadband & Hathway Broadband, Hathway is still cheaper, as Jio is tricking on minimum charge for monthly plans, the minimum charge is 1500 Monthly, so minimum total 18000 yearly, where they are mentioning 2000GB quota(for a home subscriber such big quota is unconsumable, altough for business users its good plan), current avg consumption is around 100GB, and most user’s will fall below 200GB monthly usage, So lets take Hathway biggest plan 200GB monthly plan which is at 16499 yearly.

and for a normal user 100GB monthly would be fine which can be bought @10999, whereas Jio’s basic plan is @18000.

Still, there is the probability of Jio taking away the incremental growth from Hathway, but we will have to check market size & other competitors as well in order to know if the market can sustain many profitable players or not.

Open points: Any help from seniors/members would be appreciated

Checking valuation: as all the telecom & broadband business seems to be on cyclically low earnings thanks to Jio, P/E doesn’t make any sense, so I am not sure how to value this business.

also need to factor in debt.

Depreciation: I am not sure how long the high depreciation will continue, basically depreciation and interest are eating all the earning.

as I understood if assets are well depreciated and still retain their earning power, the return on assets will be higher, but the key is to know when the current majority of assets will depreciate.

Competitive analysis: Still need to check about other competitors, comfort is that Hathway is a leader in their market.

Disclosure: 7% of PF @avg price of 25.6, I am a novice investor, this is not a recommendation, please do your homework before investing, this post is still work in progress.

Refrences:

Hathway-Earnings Presentation.pdf (931.8 KB)

, just pointing out that cable Tv business has been under transition since many years and now all the phases of digitization forced by Govt are complete, so there is a good probability of upturn in industry.

, just pointing out that cable Tv business has been under transition since many years and now all the phases of digitization forced by Govt are complete, so there is a good probability of upturn in industry.