The last portfolio update was at the end of Feb and I was thinking about the regularity at which I should share the portfolio performance and updates. Without any scientific reasoning, I feel a monthly update is a decent rhythm in this high-octane market especially when I have a reasonably high portfolio churn as of now.

Before, I delve into the last month performance and portfolio changes - I had these thoughts go through my head, what is my portfolio objective or how would I describe my PF goal?

Portfolio Objective - Generate a minimum 15% compounded portfolio return starting 1st Jan 2021 for a decade with low volatility minimizing the depth of PF drawdowns.

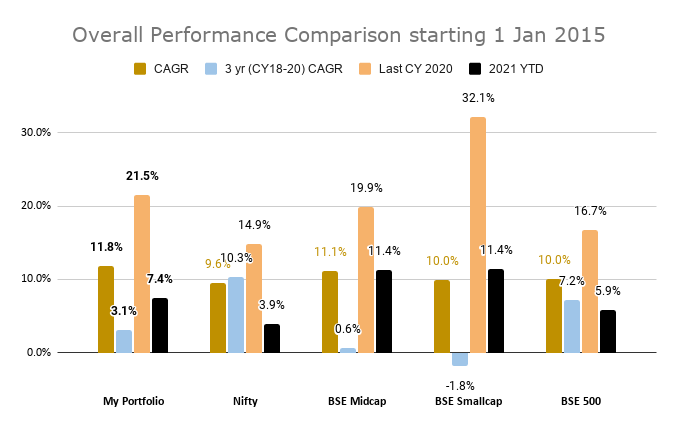

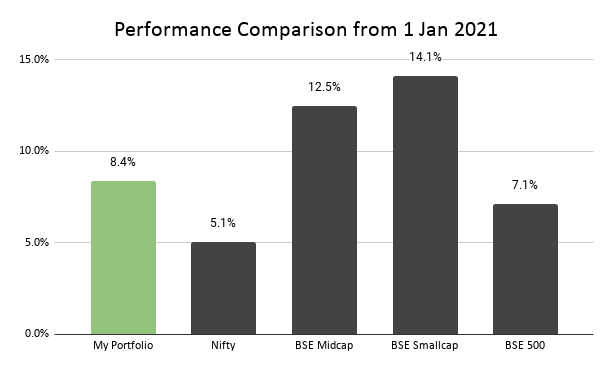

With the above in mind, let me share the ytd Q1CY21 PF performance (along with key benchmark indices):

If I come back to my PF objective now, let me address the second part of the objective first “low volatility minimizing the depth of PF drawdowns” and will come to the 15% compounding part later.

Now there is no better measure of volatility than beta defined as “systematic risk—of a security or portfolio compared to the market as a whole” (Wikipedia).

I’ve been tracking my daily portfolio % change over the past 10 months and based on that data when compared with the Nifty, my PF Beta is 0.78 as of now. Given that I’ve had a rapidly changing portfolio in the past year throwing out lots of leveraged financials and other high beta names, I expect a more reliable measurement of my PF Beta early next year. However, Beta of 0.78 does mean I expect the volatility of my PF to be at ~80% of the market volatility. My target PF Beta would be around 0.50 whilst also not compromising on returns objective.

However, I do want to highlight that the objective here is to minimize PF drawdowns in market downswings along with reasonable participation in market upside.

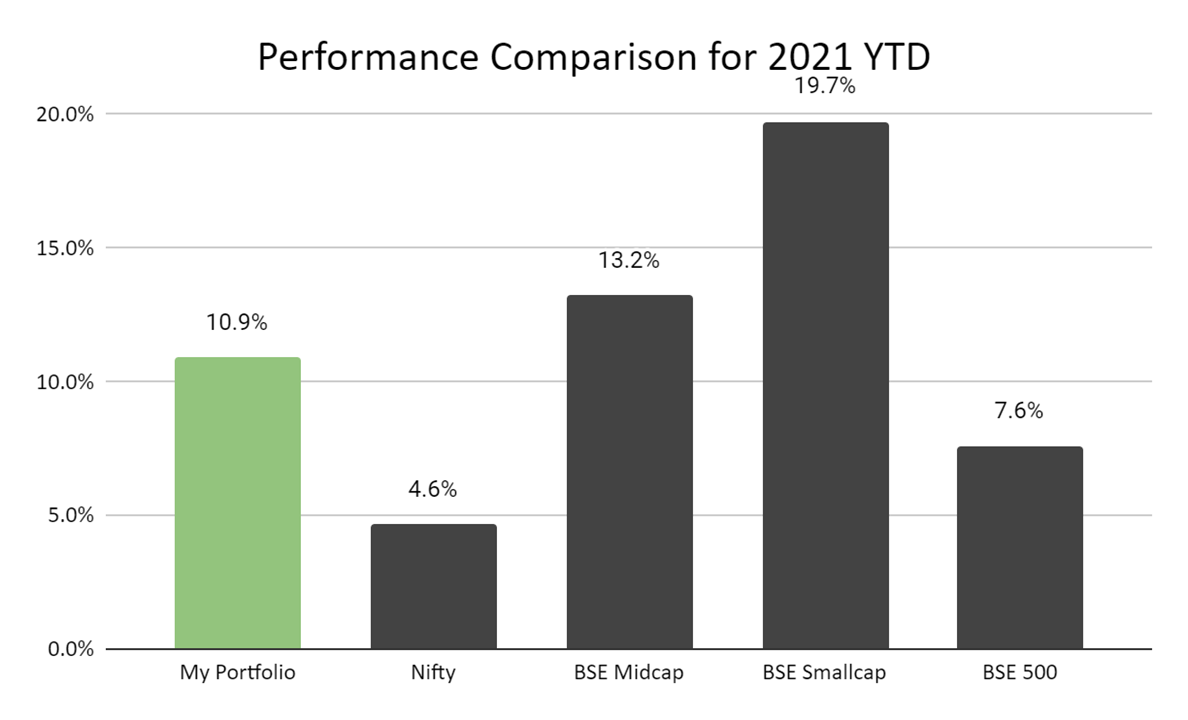

The above chart shows the YTD daily PF performance (orange worm) overlayed on top of all the key benchmark indices. Here we can see the objective I’ve described above being met in terms of the portfolio performance, lower drawdowns and reasonable participation in the upside. The caveat here is the very small time period of observation. Will look to share the PF Beta and the daily performance chart on a quarterly basis to observe how the portfolio is shaping up and whether it is on track to meet defined objectives.

Now coming to the first and most critical part of the objective i.e. getting 15% compounded returns. This requires having a very strong PF focus on growth oriented businesses with good managements may be mixed with a few significantly undervalued businesses with potential future growth. This has led me to making quite a few PF changes off-late and also forcing me to re-think my philosophy of Coffee Can approach.

Portfolio Mindset Change - The time period between Dec-Feb has made me understand the importance of being able to sit on cash irrespective of the market movement leading to FOMO and feeling of last chance saloon. The key difficulty I faced during December - February timeframe was worthy opportunities where I could deploy cash and also meet my portfolio objectives of 15% compounding for 10 years. So while business like Britannia, Abbott, etc. were correcting and offering good min. potential returns of 10-12% over the long term, I realized these businesses still didn’t offer enough MoS to be confident of achieving the 15% return objective. And hence the realization to get out of any such businesses where the conviction of meeting my objective does not stand anymore.

Also, whilst the Coffee Can approach is the best way to identify and select great businesses, I may not be able to sit idle and not take any action for a 10 year timeframe especially if some of the businesses deliver 5/10 year expected returns within a year itself. Hence, have a Core portfolio approach (invest using Coffee Can filters and sell using multiple criteria of recent business performance, valuation re/derating, expected future changes in business / environment, management changes, etc.)

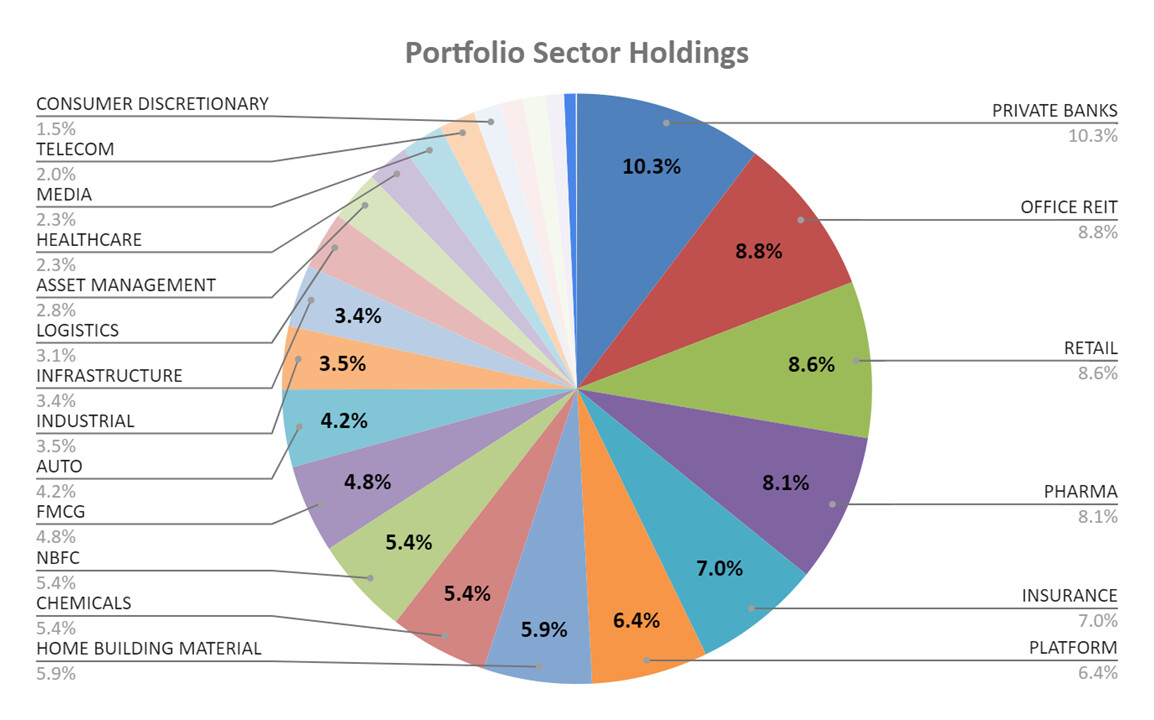

Portfolio Updates over the past quarter

Core Portfolio Exits -

Alkyl Amines (4.5 bagger in 11 months and life high crazy OPMs, valuations)

Chola Finance (90% returns in 1 year, 5x book value and 7x leverage) - In just a year, I’ve seen my investment go down by 65% and then come back up 4.5x from lows to give overall 90% returns). Way too much volatility for me to handle, also reflected in the stock beta of more than 1.75

Berger Paints, Marico - Outcome of the portfolio mindset change. Given me 50-70% returns in the last 1 year somewhat underperforming the Nifty (a clear indicator of the rich valuations these businesses already trade at). Will be exiting all in next few days to lock in LTCG

Abbott India, Britannia - Were recent investments and covered above mostly. Happy to be a buyer of Britannia at 2500 and Abbott at 10-11k levels which gives me MoS for 15% type of compounding. Not that these businesses still won’t do that, but just that I don’t foresee it and don’t want to bet on it

Core Portfolio Entry - I’m still building positions in most of them as they don’t fall a lot even on the worst days

Syngene - Strong industry tailwinds, one of the fastest growing listed businesses in the market with solid execution track record and consistent growth capex over the past 5-7 years expected to continue at least for 1-2 decades.

Valiant Organics - Excellent management track record Aarti group company, industry tailwinds, very good profitability metrics, very strong growth capex expected to come onstream in the next couple of years

Fine Organics - India#1 amongst top 6 global players in a good growing industry with strong tailwinds, strong business growth and management execution track record with excellent return ratios, 75% promoter holding and all leading MF small cap funds invested. Also covered in a recent interview by Saurabh Mukherjea

CAMS - Market leader superb profitability metrics. Best way to play financialization of savings in MF industry. Delivered mid-teens topline growth over the past decade and management guidance of 10-12% growth over next few years as well along with new revenue levers opening up

SBI Life - I think a 100 times before entering any PSU business given the wealth destruction track record. However, SBI Life appears to be amongst the fastest growing LI businesses, have inherent advantage of network distribution via SBI branches, has the lowest opex ratio in the industry and effective Price to EV of 2.6-2.7x on FY21 embedded value growing at 18%+ past few years.

REITs - I have entered in all the 3 REITs now given the tax free nature of significant portion of distributions and huge potential yield in latest listing Brookfield. Given the extremely favorable demographics we have (65% population below 35) and many million youngsters to be added to the workforce every year, I see India as one of the few bright spots for commercial RE in the next decade at least. Would have been happier if I waited a bit more and got the additional 8-10% discount on Embassy REIT currently offered by the market. This is now a very significant allocation ~12% for me, will be trimming to 10% as a little overexposed to Embassy.

Increased allocation - Indian Energy Exchange and ICICI Pru Life

Satellite Portfolio - Exits

Spandana, Indiabulls - 2 leveraged businesses (booked 40% gains and booked 50% loss). One with potential severe crisis in microfinance portfolio and other with honest / clean management and tarnished market reputation.

Airtel - Exited at no profit no loss. Seeing the competitive intensity in the telecom space and never ending capex such as 5G auctions, time to kick this one out as the positive and negatives seemed to be cancelling each other out. Would much rather hold a business with simple books of account and industry tailwinds.

Satellite Portfolio - Entry

Chemcrux - Replaced with Indiabulls holding. Excellent limited business performance, appears honest managemant with well articulated annual reports and management growth vision. Plant closure overhang has stayed longer than expected, good to see the disclosure today on the same and also approval for capex.

Icemake - See huge scope for this business and industry, cold supply chain storage and solutions. Management track record is pretty decent in terms of growth and also given strong growth guidance for next couple of years as well. This can grow multi-multi fold if executed well by the management. Next quarter should be interesting as it’s the best one seasonally and management has guided for normalcy in margins, will contemplate exiting if management doesn’t deliver somewhere near guidance without any major business hindrances.

Jubilant Ingrevia - Given the industry tailwinds of specialty chemicals and pharma, seems an interesting business with good growth guidance and very modest valuations. Management execution should lead to re-rating

Nazara Tech - Hyper growth business in an industry getting strong tailwinds with Covid, No listed peers and digital platform business should get premium multiples once business execution track record is established and recurring revenues. Key risk of very brief product lifecycle for most games.

Allocation Change - Significantly upped allocation in RACL Geartech and Goldiam with super strong business performance and momentum. Don’t like averaging up 3x-4x of buy price but see similar potential even from the current market cap.

Watchlist - Bajaj Healthcare, Indigrid (hoping it corrects 20-25%)

Concluding Thoughts - I want to crush market risk without compromising on returns in order to sleep peacefully every night. Having an all-weather portfolio with a bullet proof core helps achieve that.

PS: Hopefully, next month’s update will be a lot shorter