Can anyone share the link for q3fy22 concall. I checked but could not find any concall link.

1 Like

Are they doing a concall for Q4FY22??

1 Like

Bad numbers for the quarter, with inflation and rising raw material cost, company unable to sustain margins. Revenue growth only positive.

Hi Seniors,

Anyone still tracking this company. They have embarked on significant. capex for both grain processing and ethanol segments, this will change the revenue mix to almost 50:50. Given the ethanol blending push, this should be positive in long term. however i am not sure about other capacity coming for ethanol and if that could impact the future prospects. Any thoughts on that?

2 Likes

Hi

I track the company closely. Posted decent results

Results : https://archives.nseindia.com/corporate/GULPOLY_12052023193226_Outcomeofbm120523.pdf

recommended a Final dividend @ 50% 0.50 per equity share

recommended the Issue of Bonus Equity Shares in the ratio of One (1) new fully paid up equity share for every Five (5) existing fully paid up equity shares of Re 1/- each held

Next two years should be bumper for the company. With 500KLPD going on stream I expect them to double their sales this year to 2200 crores and 3300 crores next year.

1 Like

Yes, as commodity prices are softening, basic business will get stronger as well apart from ethanol business, might be a future multibagger.

Update from the company

500 KLPD has almost reached to the final stage. Announcement expected anytime soon.

Once the official announcement is out as can expect 100% rise in Revenues on YoY basis

1 Like

@Dhaval_Parikh - This may be possible only if plant runs every day of the year and company is able to sell the entire new capacity of 500KLPD. Per AR of 2022, offtake agreement with OMCs are in place only for more than 50% of the capacity.

What’s the math behind your expectation?

Revenue increase of 50% is reasonable this year, next year for sure it will be100% as 230 KLPD plant in assam will also contribute. Ethanol blending will be top priority from govt as it saves direct forex.

1 Like

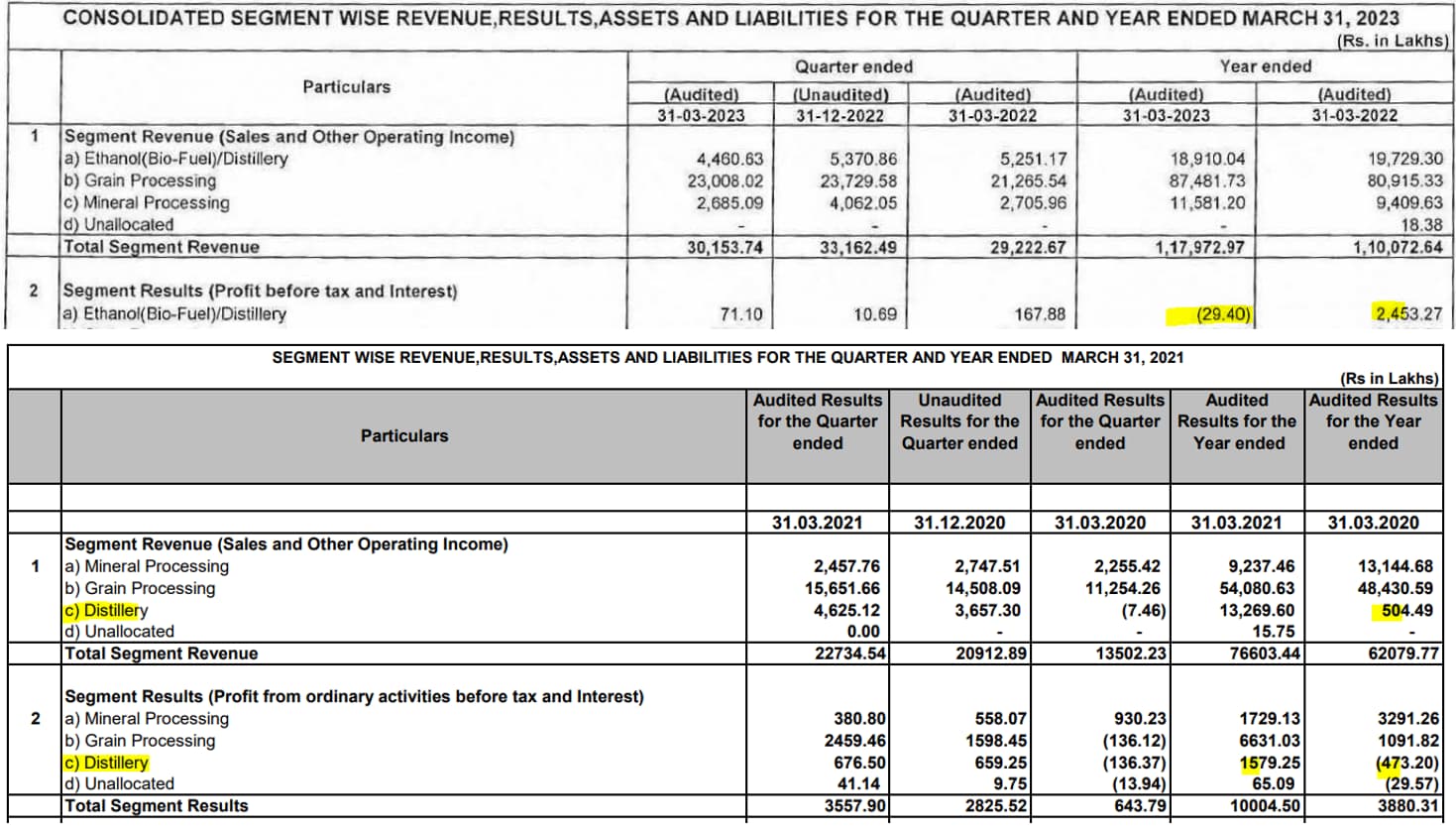

Why profitability of the Distillery business got impacted in FY23 although it did well in FY21 and FY22? Are those factors beyond management’ss control? If yes, the immense topline growth (expected from distillery) will not reach to the bottomline?

Press release of Q1FY24 provides a reasonable ground to answer the above questions.

I understand that the business has no power to dictate either selling price of finished goods or cost price of raw materials for Grain Processing and Ethanol Mfg. Divisions. Although Ethanol Division is expected to become the major contributor to the overall revenue, it has 2 additional constraints:

- No concrete source of raw material. Recently, FCI stopped the supply of broken rice even for the old plant (60KLPD). If not addressed soon, profitability will be further strained as they have recently capitalized 500 KLPD plant.

- Profits ought to be managed with in the regulatory pricing of both the finished goods and raw materials.

Disc- No position.

1 Like

@Surender The overall demand for ethanol is much higher than the supply. They have purposely kept the contract for upto 50% because if there is a delay in supply their reputation is not impacted. Once the plant becomes operational (which it is now) the company will again apply for tender. Note that these tenders are on ongoing basis and just procedural in nature so the supply can start in 2 weeks time. Assam capacity is also going live by the end of the year. So I am confident that they will be able to grow their revenues.

The only concern here is the RM prices as it keeps flucutation. But with the recent decisions made by the govt I Dont think companies will be much impacted as govt will increase the rates if the RM prices goes up to ensure that they get steady supply.

1 Like

I think there is still some opportunity left in this script.

FY25 could be very big, distillery segment itself can generate 1700-1800 Cr revenue.

Margins may improve from Q3FY24 onwards due to new crops and increase in the ethanol price, with avg margins of 10% on very conservative side FY25 PAT should be > 2X FY23 PAT.

In between any FCI rice release would be a great advantage, Govt is supporting the ethanol producers by increasing the price if there is any inflation in the RM, so this final product price risk can be mitigated with some lag

1 Like

Here’s My Take

Industry Overview

The size of the global ethanol market was estimated at USD 99.06 billion in 2022 and is expected to reach approximately USD 162.12 billion by 2032, expanding at a compound annual growth rate (CAGR) of 5.1% between 2023 and 2032.

The projected value of the ethanol market in India in 2022 was USD 2.27 billion. India’s ethanol market is expected to grow at a compound annual growth rate (CAGR) of 9.16% between 2023 and 2029, with a projected value of USD 4.15 billion by that year.

Globally, India is the fourth-largest producer of agrochemicals after the United States, Japan and China. India accounts for 16-18% of the world production of dyestuffs and dye intermediates.

The size of the India agrochemicals market is anticipated to increase at a compound annual growth rate (CAGR) of 9.75% from USD 7.90 billion in 2023 to USD 12.58 billion by 2028.

The Indian chemicals industry stood at US$ 178 billion in 2019 and is expected to reach US$ 304 billion by 2025 registering a CAGR of 9.3%. The demand for chemicals is expected to expand by 9% per annum by 2025.

Company Profile

Founded in 1981, GPL is a multi-site, multi-product manufacturing company that operates in Grain processing, ethanol (biofuel)/distillery, and mineral processing make up its three primary business segments with global presence in 35+ countries, across 3 continents

Gulshan’s product portfolio comprises of starch sugars and native starches, calcium carbonate; agro based animal feed, alcohol business & on-site PCC plants. Gulshan is providing solution to diverse range of Industries & niche markets in core sector i.e., from toothpaste to alcohol, from sweeteners to paints, from paper to medicines, from plastics to personal care.

Gulshan has an impressive clientele comprising of the nation’s Top FMCG’s, Leading paint manufactures and many reputed brands.

Why We Are Studying?

- 20% Ethanol Blending by FY25 i.e 1000 Cr Lit may leads to save Rs 30,000cr

- Expanding its ethanol capacity to 810 KLPD from current 60 KLPD

- Company received an order worth Rs 572 crore to supply ethanol to OMC

- Mean Reversion likely To Happen

Business Model

Gulshan Polyols Ltd. (GPL) is an Indian company specializing in grain processing, biofuel (ethanol) production, and mineral processing. Here’s a breakdown of their business model

Manufacturing Units & Business Segment

- Grain Processing Unit

- Gujarat – (Sorbitol 70% Solution and Liquid Glucose)- This unit is largest production Center of Gulshan for export of Starch Derivatives using Corn as raw material and has attained the Star Export House certificate. Captive Power Plant Capacity:7 MW (Two turbines of 3+4 MW

- Uttar Pradesh – (Native Starch, MDP, DMH and Liquid Glucose)- company process NON-GMO Rice to make Dextrose Monohydrate, Malto Dextrin Powder, Glucose Powder, Rice Gluten for food and pharmaceutical applications.

- Company has facilities with a combined capacity of 1,81,800 MTPA for producing starch sugars and for Sorbitol with capacity of 72,000 MTPA with leading market share.

- Mineral Processing Unit

- Uttar Pradesh – (Calcium Carbonate (WGCC)) Captive power plant capacity: 8 MW .

- Himachal Pradesh – (GNCC and CCPG) This Unit is engaged in manufacturing of Ground Natural Calcium Carbonate (GNCC) in powder form and Calcium Carbonate Pigment Grade (CCPG) in slurry form by using limestone as raw materia.

- Rajasthan – (GCC – Coated and Uncoated) Unit of Gulshan manufactures different grades of Ground Calcium Carbonate (GCC) – Coated and Uncoated. It caters the demand of Polymer Industry and mainly supply in Central and southern part of India.

- Ethanol & Distillery Units

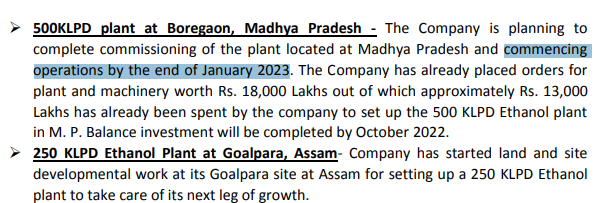

- Madhya Pradesh – (Ethanol/Extra Neutral Alcohol) Company had an existing set up of producing 60 KLPD ethanol at Chhindwara (Madhya Pradesh) since May 2020. Company is constantly suppling ethanol to OMC’s.

- The Company has successfully achieved another milestone by running commercial operations of its 500 KLPD Grain based Ethanol Plant at Boregaon, Distt. Chhindwara, Madhya Pradesh at 25% capacity utilization to begin with.

- Key Clients : Britannia,Yahoo Foods,Asian Paint,Colgate ,Wipro,Paragon,Dabour etc

- Company generates major chunk of its revenue from Domestic Market which is 90% & remaining from export.

Competitive Strength

- Softening of Key Input Costs Will Aid our Margins Going Forward

- Grain-based ethanol has a distinct cost advantage over sugarcane-based ethanol & there is Possibility of higher production capacity for native starch.

- For its new ethanol plants in Madhya Pradesh and Assam, the company will be eligible for Production-Linked Fiscal Assistance from multiple state governments.

- The decision of advancing 20% blending target by 2030 has created huge opportunities in the ethanol sector. Ethanol plants based on Starchy feedstock are going to drive the new capacities.

- The company has 3 decades of the Experience with experience Management Team.

Future Outlook

- By FY25 the Company plans to expand its ethanol capacity to 810 KLPD from current 60 KLPD.

- The company received an order worth Rs 572 crore to supply ethanol to OMC. The company will supply 89,404 KL of ethanol to BPCL, IOCL, and HPCL.

- The revenue mix will shift as a result of the ethanol segment’s capacity addition. The grain processing segment currently accounts for about 75% of revenue, followed by the ethanol processing segment at 17% and the mineral processing segment at 8%.

- After commissioning new facilities, management anticipates that the ethanol segment will generate about 50% of revenue, with the grain processing segment accounting for the remaining 50%. The segment responsible for processing minerals will eventually contribute less.

- The management expects EBITDA margin to improve in Q4 FY23 due to softening of basic raw material prices and declining coal prices which will lower our power and fuel cost.

- Assam – (Ethanol/Extra Neutral Alcohol). Assam for setting up of a 250 KLPD grain-based ethanol (distillery) unit expected to commission by the end of H2 FY24.

- Out of the INR 600 crore total CAPEX, the company has spent INR 250 crore, with INR 350 crore still outstanding. By the fourth quarter of this fiscal year, the ethanol plant should be operating at maximum capacity.

- The Company has entered into long term Contract with Western Coalfields Limited for procurement of Coal for its plant at Madhya Pradesh for 84000 metric ton p.a to get stability in coal price procurement.

- Companies 500 KLPD Grain Based Ethanol manufacturing unit has started commercial operations and now successfully running at 25 % capacity utilization, which should go upto 50% capacity utilization in coming quarter

Risk

- Over the last two quarters, the grain processing segment’s margins have been impacted by the increase in grain and coal prices.

- lacking a reliable raw material source. Broken rice was recently discontinued by FCI, even for the 60KLPD old plant. They recently capitalized a 500 KLPD plant, so if this issue is not resolved quickly, profitability will be worse.

- Due to rice supply halted by the Food Corporation of India (FCI) for ethanol production, the ethanol segment witnessed a marginal disruption in its operations.

- Delay in Contract /over capacity of Ethanol

Dis: Educational Purpose Only***

Liink :https://www.youtube.com/watch?v=rTRz0WbGui4&feature=youtu.be

3 Likes

Thanks for the detailed post. I am not invested in GPL but one of its competitor BCL Industries. IMHO, before one invests in a Ethanol producer whose feedstock is not sugarcane, one should find out whether the company is hooked on FCI rice for its feedstock or whether its management had the foresight to know that FCI rice was a short term dole given by Govt and they have already de-risked the business by having factories which can process multiple feedstocks like rice, maize, millets etc.

Any non-sugarcane Ethanol player need to be able to process Maize for it to have long term sustainable advantage as the Govt wants players to not rely on FCI Rice and reduce dependence on other water guzzling crops like Cane.

If you find that GPL’s new units can indeed process maize and they are able to secure enough maize to manufacture most of its Ethanol from it, then GPL can be a good value creator indeed.

3 Likes

Now GPL is also producing ethanol through Maize & damaged food grains.

I am also invested in BCL but i feel more value is left in GPL now, FY25 could be a game changer for GPL as they get 800 KLPD on stream, this 800 KLPD can generate 2000 Cr revenue.

3 Likes

Great insights.

I feel only risk is RM prices, if they can maintain the margins then everything will be good.

They should focus more on RM inventory/procurement management. Demand for ethanol would be there, no question about softening of demand.

3 Likes

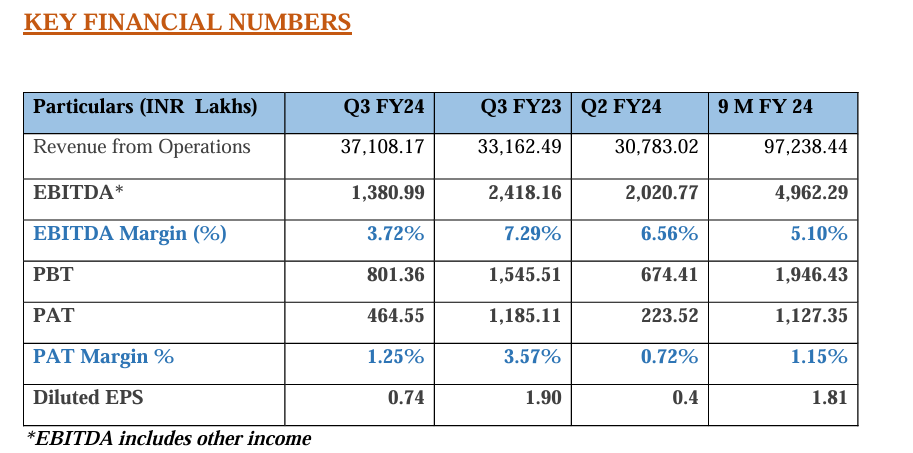

Q3FY24 could be the lowest ever margins in the companies history.

Even though margins are down, absolute number is increased as compared to Q2 due to incremental ethanol revenues.

Q4 can add 50-60 cr due to increase in capacity utilizations and increase in the ethanol selling price. PAT can double in Q4 as compared to Q3.

1 Like