Company interest part rose significantly in March qtr and yoy even though its debt is reduced…how to look at it? What could be the reason?

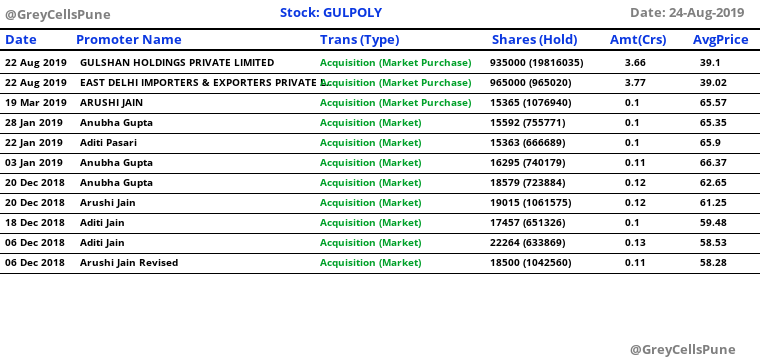

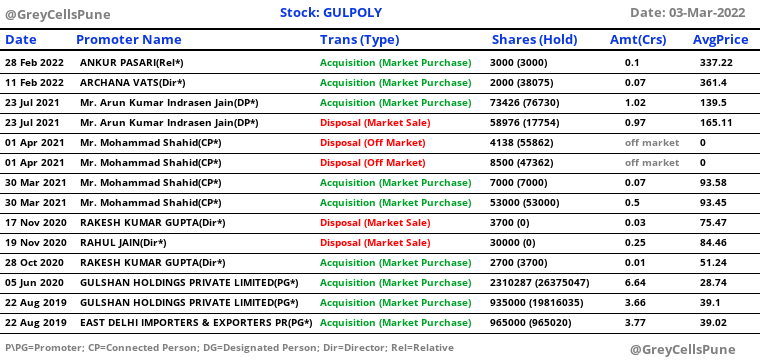

Heartening to see promoter and promoter groups acquiring stocks over the last 6 months… and the 2019 results are also encouraging…

However I am digging deeper on 2 fronts and wondering if some of the experts here can shed light on

-

Gulshan Polyol trust purchased 1cr worth of stock for ESOPs since formulation (2018) but not granted any options yet

-

Promoter Salary is on the higher side vis-a-vis PAT and does not scale appropriately during difficult years. The remuneration structure also seems off given the delta between MD & CEO salary. This is purely a layman observation from my side and haven’t compared the remuneration structure in similar businesses which are founder led at this scale.

1 Like

2 Likes

Very strong results. Outlook for the full year looks very good with high demand for sorbitol and fructose and low RM prices (maize). Distillery which was a drag from past few years will also start contributing positively due to liquor license recently recieved.

3 Likes

Sorbitol and HFRS capacity expansion likely to be operational by March 2021. Besides, native starch should attain higher capacity utilisation in view of school/colleges being opened and main buyers are paper sector.

1 Like

They have just mentioned in their latest presentation that they are evaluating expansion in HFRS and sorbitol. Where have they said anything about completion by March 2021?

For Distillery business for similar revenue profit is tripled. What is driving this ?

They got a license to supply country liquor and margins are much higher in liquor compared to ethanol.

1 Like

Hi can some one give me details on Sorbitol and distillery capex plans ? Sorbitol is 2x and Distillery is 5x ?

How much revenue can Sorbitol capex and Distillery capex add ?

1 Like

Interview on cnbc; guidance of 1000cr top line in this year

2 Likes

Good results from GPL. Based on the mgmt commentary, the company is benefiting from the ethanol blending program.

1 Like

A good set of numbers by the company. The result and management commentary appended.

Gulshan Sep Results.pdf (5.7 MB)

2 Likes

What is update regarding Sorbitol capacity expansion ?

This is where pain was in current Quarter.

Additional land has been purchased at MP Plant to support incremental demand.

2 Likes

Q3FY22 Concall

Disclaimer - I was able to note down only few portions

Capex - Capacity of grain processing Starch,FRUCTOSE and sorbitol increased by 30% at a capex of 100cr

Starch and derivatives capacity raised from 1.75L Mtpa to 2.5L Mtpa and we expect to commercialize in FY23

After the ethanol 500kpld is commercialized, overall revenue will 50-50 revenue contribution between grain

and ethanol

The Ethanol plant of capacity 500klpd Chinbara will give 3x growth in ethanol by FY25.It will be operational by Jan 2023, we immediately target 80% capacity utilization due to the OMC tie up.Ethanol business margin will be 13-14%

Sorbitol , starch , fructose currently operate at 90% capacity

Starch products and derivatives are supplying to semi craft paper industry to make boxes which are seeing good traction due to E commerce tailwind. We are able to sell products within 100kms of the plant

Fructose to food segment 17% growth,Fructose RM is rice and RM is 55% cost of overall production

Sorbitol plant is in Gujarat, the RM here is maize also for starch and derivatives

Similar margins across all verticals of grain processing

5 Likes

Just to understand the Economics: 11.2 Ethanol Production and Economics | EGEE 439: Alternative Fuels from Biomass Sources

Ethanol Journey So far in India: https://static.pib.gov.in/WriteReadData/specificdocs/documents/2021/oct/doc202110441.pdf

Did anyone estimated additional revenue when total 11 cr litre of ethanol will be supplied ? How much will it add to the topline on the current numbers ?