Efforts are ON to stop the carnage

I have a lot of respect for Bharat Shah, ASK Investment Managers. He rode the Infosys growth in the 90’s when he was with Aditya Birla Mutual Fund (left in 2002 to join ASK).

He has a very interesting take on how to value lenders and has a special mention for Gruh and that such stocks should be valued as FMCG stocks since they have not diluted equity for decades, have a high dividend payout ratio, high growth and the large size of the opportunity.

Worth listening from 19 minutes onwards.

As per him: ‘Gruh Finance…always looks high priced…but if you look at all the parameters…is actually reasonably priced…’

1 Like

Like clockwork

3 Likes

Apart from the steady and boring 20% growth year on year…Not to be missed:

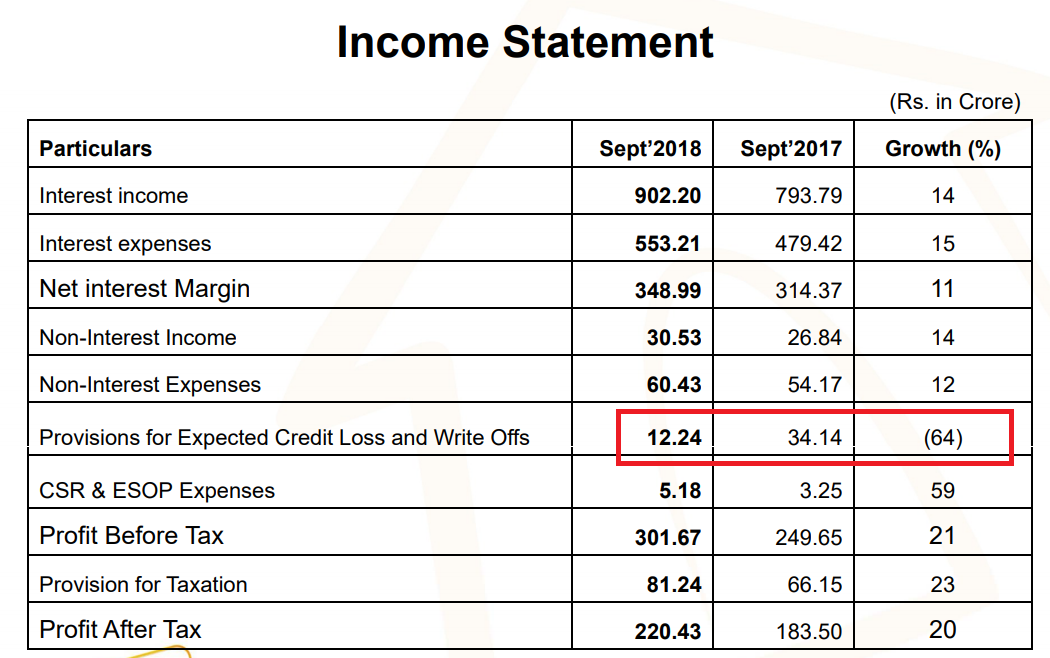

Press Sept 2018.pdf (298.1 KB)

As per accounting standards, Gruh is supposed to carry provisions of Rs 50 cr towards future credit losses. Instead, it is carrying provisions of Rs 129 cr (Page 3).

Over, over conservative. ![]()

3 Likes

Quarterly Net Profit at Rs. 105.49 crore in September 2018 up 35.64% from Rs. 77.77 crore in September 2017.Results show class apart and justify the high valuation.

A correction, s11.

PAT in Sept 2017 was Rs 87.77 cr and not Rs 77.77. So growth in PAT is 20% and not 35.64%.

Nevertheless, steady as ever and a very conservative balance sheet.

Every interview related to housing finance/NBFC Gruh comes into mind of the top investors! We saw that in coffee can investing investing too!

1 Like

I liked everything in this interview but small retail investors should never go for liquidation value of business. There is no way in hell that we will get anything if the company goes into liquidation in India. The company directors will negotiate with the large institutions and fund managers and we will be left holding the bag.

For us the path to winning is identify good businesses with reasonably ethical managements and keep investing for the long haul. As we do that we will find one or two multi-baggers in our lifetimes and lo and behold we make a decent amount of wealth.

3 Likes

Its related to our industry & our company doesn’t figure in it… seems that keeps us out of bunch & ahead of everyone

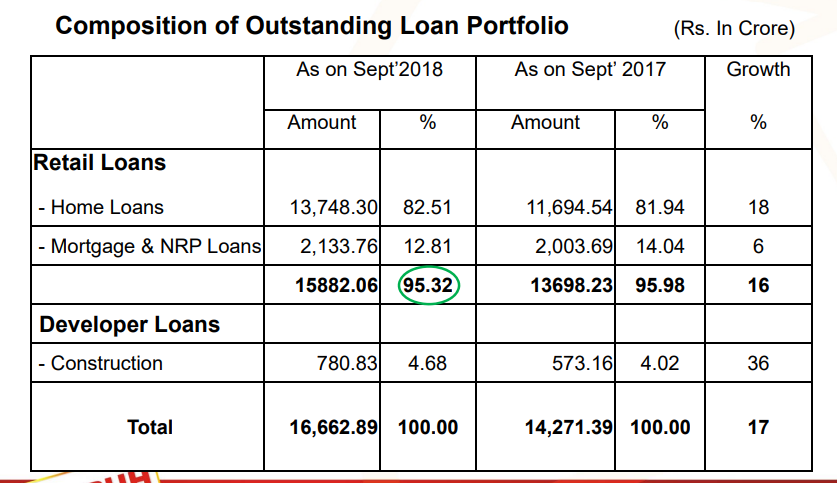

Some notes/thoughts from AR18 & HY19 results →

ASSET SIDE

One of the first things to notice is ticket size, profile of borrowers & location of assets -

- As per HY19 investor deck, 49% of the loans are in the towns with population < 50,000. The number was close to 53% in March’18.

- 39% of the loans have ticket size of < 3L & 86% of the book have ticket size of < 10L

- 91% of the borrowers have monthly income of < 50,000 Rs. & 65% of borrowers have income of < 25,000

What these things do is, it makes it difficult for banks to go after these customers/towns by the virtue of LIG & MIG-1 categories, small towns & smaller ticket sizes.

Despite this, Gruh faced prepayment ratio of 13.87% in FY18, the ratio was close to 11.17% in FY17. If one were to go by commentary of CanFin homes management, these ratio shall come down in rising interest rate scenario.

Another thing to notice is that 71% of the loans are sourced by Gruh Referral Associates (akin to Direct Selling Agents - DSAs by Can Fin). Given that, HDFC group has strong focus on building proprietary selling channels (As seen in HDFC, HDFC Bank & HDFC Life), reliance of Gruh on agents tells that you can’t build entire sales franchise & sell variety of products on asset/liability/insurance/wealth management to these customers.

Further, Gruh has ~17% of assets into LAP, NRP (non-residential properties) & developer loans. This is not a concern yet given the conservative nature of Gruh management.

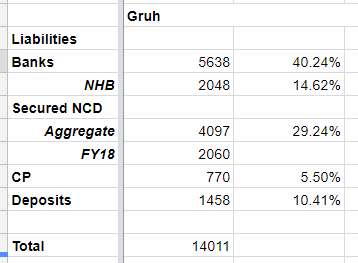

LIABILITIES SIDE

One of the things that Gruh has done better than CanFin is sourcing of public deposits. ~10-11% of total funds are from deposits and renewal rate of deposits is ~50%. Gruh has special deposit referral associates who mobilize deposits. This is one of the low hanging fruits for CanFin to emulate in my opinion and take advantage of permission to have public deposits.

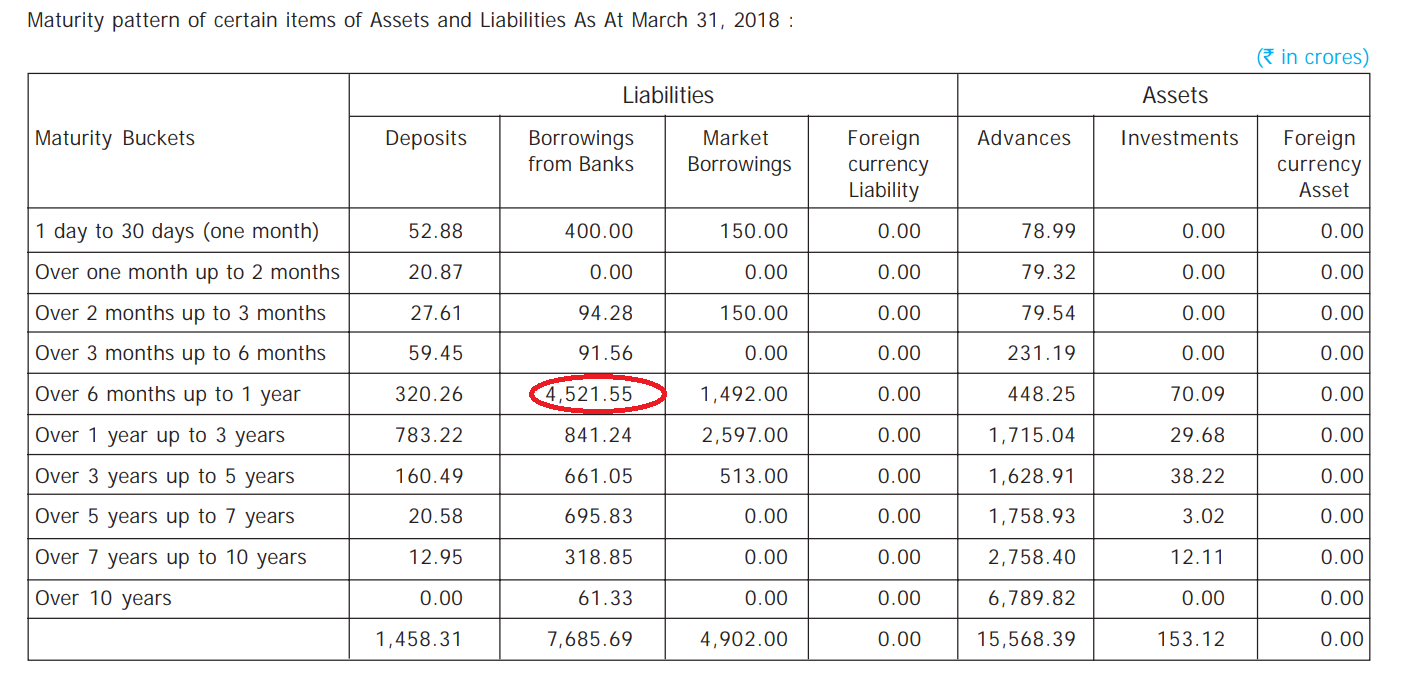

Another interesting thing is ALM disclosure of Gruh →

There is ~4500Cr of bank borrowings that are maturing in 6-12 months from March’18. if one looks at progression of long term & short term liabilities, it looks like Gruh had replaced long term loan with short term loan.

Neither the half year results or investor presentation provide split of current vs. non-current liabilities. I am looking to find out how these liabilities have progressed in FY19.

It is possible that these loans got replaced by another loan which has higher costs & hence spread/NIM got compressed. But I am still looking for details.

Another thing from HY19 results is that 20% profit growth is primarily due to lower provisions on account of conservative provisioning in earlier years.

The core operating parameter of interest income has grown at 14%.

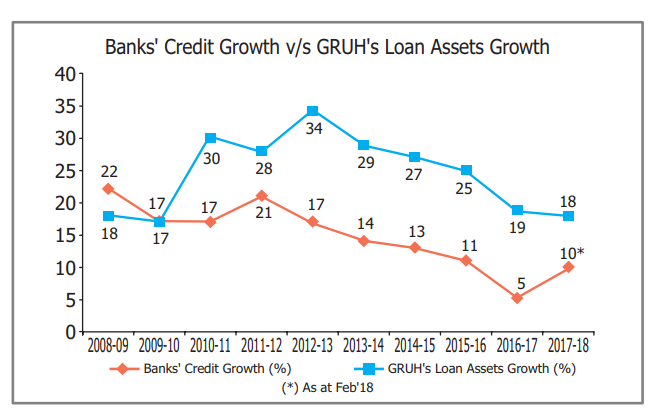

Further Gruh’s assets grew by 25-30% between FY11 to FY16 and the asset growth has come down to 18-19% in last two years & valuations have grown faster than the asset growth.

Although, one can never bet on valuation of HDFC group of companies going down, for me personally, I would need visibility that asset growth can come back to 25-30% to take fresh position at current valuations. I would be okay if spread/NIM compresses in the next 12-18 months if asset growth comes back. Given the record of Gruh, I am confident that over the long term spread/NIMs would revert to historical averages.

Disc - Token position, this is not a buy/sell recommendation. Investors are advised to do their own due diligence.

20 Likes

3 Likes

Faster green norm approval of 20k-50k sqm projects & Lower prices may act as a booster for housing finance companies.

Understand that its good to avoid recent issues & good for long term investors

Good for quality players as others may struggle

#CNBCTV18Exclusive | @bandhanbank_in which is in violation of the @RBI regulations in terms of promoter shareholding is looking at merging a housing finance company as a step to reduce promoters stake, learns @PoddarNisha @HomeLoansByHDFC pic.twitter.com/SrsJXK66BF

— CNBC-TV18 News (@CNBCTV18News) December 21, 2018

Doubt about cnbc carrying out such reports, need to verify, first of why should hdfc part with such classy asset unless they are getting very very good price,

Insider buying recently:

16/12

GRUH Finance insider trade: Acquisition of 75,000 equity shares worth Rs 100.58 lacs by director

I wouldn’t believe anything CNBC says unless confirmed by the related parties.

this is not insider buying, but employee stock option as seen in link below

https://www.bseindia.com/corporates/Insider_Trading_new.aspx?expandable=2

Gruh Finance clarification to BSE. Company says " They would not like to comment on it since news is speculative in nature". But goes on to clarify that they continue to explore opportunities…So its clearly not a denial

2 Likes