2 Likes

There will be dtl for that particulat FY and not of previous FYs. So the dtl amount will be smaller. By FY17 all arrears will be cleared. Going fwd dtl liability will be lower

1 Like

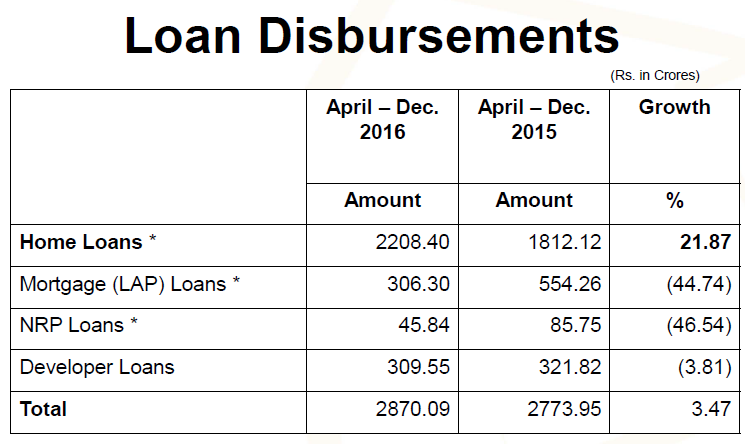

Loan disbursement growth has gone down to 3%. but mainly due to reduction in other than home loan category.

from some earlier research report i could see in fy15 Q2 it was total 20% .

my understanding is there is substantial reduction in disbursement growth this quarter, but understanding that home loan category growth sustains within that, it may be a prudent decision at the moment.

others may comment, if any different view they have or correcting me if necessary.

2 Likes

The latest investor presentation talks about the “RESILIENCE OF GRUH.” Post Lehman Brothers’ Collapse in October 2008, Earthquake of January 2001, Gujarat Riots of February 2002 and now the “demon” quarter.

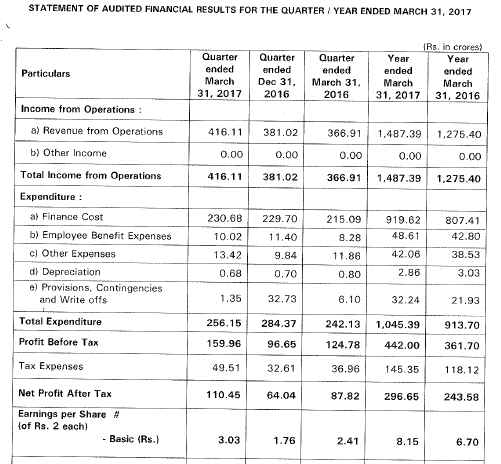

NII is 4.11% and NNPA is 0%.

I feel it is a good show and am thinking to add to my positions.

1 Like

Thank you us121. This is a valuable insight.

It’s a prudent thing to do. LICHF came out with results and they have seen a massive jump in developer loans and LAPs, which has helped it show good disbursements. But this is contrary to what the management said in Q2 FY17 call. They had indicated going forward the focus would be to increase retail home loans.

It is risky to take bet on developer loans and LAPs in the current macro scenario. It is good that Gruh has chosen not to do so.

Discloser: Not invested in Gruh, Hold LICHF- 3% of Portfolio

4 Likes

on the contrary Gruh commentary post last Q1 result was they are substantially reducing the growth in other than Retail loans as they have crossed their internal threshold limit.

This was even before Demonetisation. They exactly did what they said. and that is the secret of Gruh’s high multiples.

6 Likes

Valuation metrics doesn’t work for Gruh!! If we want to be invested in Gruh we have to make our decisions based on price action?

Any specific reason for sudden spike today. At one point it was up +20%

1 Like

Good set of numbers. More than steady this time, almost 30% growth better than expected.

2 Likes

4 Likes

On second thoughts, slightly disappointing results from Gruh. For a company trading at 10x fwd p/b, one expects better than 25% loan growth. Gruh has underdelivered. I doubt the current valuations will sustain. The stock has proved me wrong in the past though. But i feel gruh will down to 7-8x fwd book now very soon

i dont think results are disappointing. herein what i notice in results:

- co has reduced exposure to risky LAP segment. retail home loan in FY16 were 75% of disbursement and grew 31%. this growth shall even pick up further with govt interest rate subsidy.

- NIL NPA

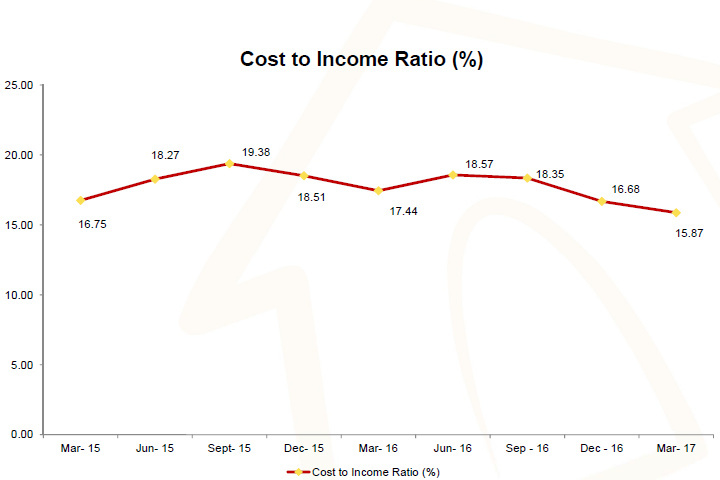

- 18.31% CAR, cost to income down to 15.87% from 17.44%

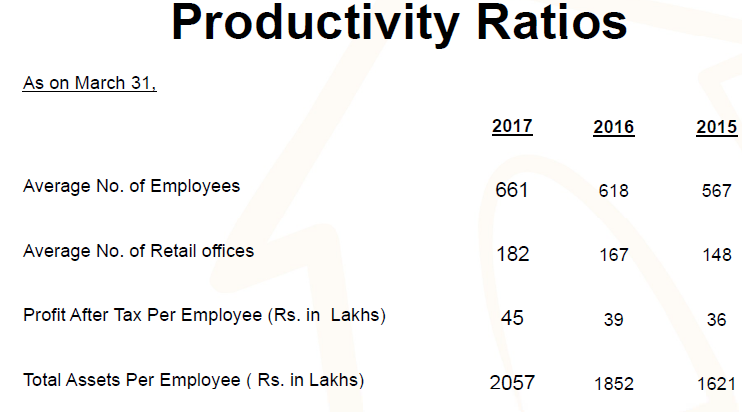

- branch network expanded at 185 from 179

Overall, you have a company growing consistently around 25% PAT growth with 0 NPA and now more or less assured higher growth for next 5 years ( 2022 housing for all and govt interest subsidy scheme). in case, govt doesnt get it right, co has still been able to grow @ 25%.

Gruh is definitely expensive but strong consistent growth, negligible NPA and higher growth potential may means investor may not bail out.

On other hand, we have actually seen higher risk taking across housing finance stocks with valuation multiple expanding for canfin home, pnb housing, indiabulls housing etc.

4 Likes

Granted to all you said but a 10x fwd is not merited by a company growing loan book at 19%. Gruh interest spread is 4% not very different from many other financial companies. What made it tick for the company was >30% cagr in loan growth.

Now that the company has grown to a certain size, it is difficult for it to keep growing loan book at 25-30% at an interest spread of 4%, means a much slower sub 20% loan growth. Why would you pay 10x fwd book for that. A significant derating should happen over the next few months

4 Likes

Is it cheap? No.

Will it go low from here? may be.

But more important is quality of earning and more than that of management.

if one is willing to hold for long term, quality will give both return and peace. Value of quality is rated in tough time and derated in easy money making time.

this stock should be seen in this context more than mathematical equations.

Discl: invested.

6 Likes

Result Press Release from GRUH

3 Likes

This trending is important for efficiency gain and hence important to track:

Source: Company Investor Presentation

5 Likes

FY 17 DTL + NP = 296.65+29.07 = 325.72 Cr.

In latest interview management has shown confidence to grow. In last quarter interview he said that demand was slowing. Still they gave growth of 21.78% in NP. So we expect growth to be above 25% in NP for FY 18. So it comes around 1.25*325.72=407.15 Cr. EPS comes 407/36 =11.3

So Rs 407 cr NP and Rs 11.3 EPS are expected in FY 18. One year forward PE comes 38.8.

For a great company with competent management having all things in place to see in NBFC growing at 25%+, ROE 30%+, Payout 30%+, BV compounding18%+, NPA 0, conservative, experienced management, Sound management systems, processes in place, long runway, this looks overpriced for 9 months only. After 9 months it will be available on fair value. we seldom get these type of businesses at fare value. I believe it is better placed than fast compounder, hyped, HFCs.

Disclosure - Invested and 12.5% of portfolio. No buy sell in one year.

3 Likes

Gruh is optically rich. As and when management decides to dilute at this high P/B it will become cheap at one go! So might not come down in a hurry.

8 Likes