Overall a bad set of numbers. The bad loan assets have increased far too much for my comfort and super premium valuation it commands. Gruh is valued far far too higher as compared to any other HFCs. Till past few quarters it used to deliver super normal growth with impeccable quality but now that the growth has normalized and the asset quality is not 24 karat gold (as best 22 Karat) not sure if the the stock has potential to go up, although it may not fall.

Link to presentation for Q1FY17.

1 Like

PF money in housing …

Since I’ve been reasonably bullish on Financials and shared my views across a number of threads, just want to share - sold my entire holding (7% of portfolio) in Gruh today at 350. 15 times P/B and 50 P/E seems pretty unjustified with ~20% growth in earnings over the past 2 years.

Even assuming that the bumper moonsoon and 7th Pay Commission consumption kicks in and results in ~26% CAGR in earnings over a three-year period - that would still bring the P/B to 7.5 and 25 P/E at the current price (which is still bordering on expensive)

So to actually make decent money from these levels I’m betting on a 30%+ CAGR for 3 years minimum - a bet I’m not willing to make.

So I’m happily exiting with a 75% absolute return + dividends in 1.6 yrs (avg holding period)

3 Likes

it will always command premium valuation, p/b is not right way to look in for gruh p/e is much better

Gruh is not at 50 PE nor it is growing at 20%. Add 72 cr for DTL in this financial year to arrive at real EPS and growth. Next year EPS will be Rs 12 as No DTL.so Gruh is at fair value with high growth ahead for very very long time. Still it is wealth creator stock.

One more point, Payout ratio is 30% + so next year dividend should be more than Rs 3.6. In next ten years it might be 36 i.e. 10% of cost. In fact we are lucky that we have HDFC Trio stocks in India. Risk free compounders.

6 Likes

Are you sure that profit is lower on account of 72 crores for DTL? That is, whether DTL for previous years that is being provided til FY17 is being routed through P&L? I don’t think so. Also, my understanding is that the DTL that is being routed through P&L is for current period and will continue post FY17 also.

1 Like

No DTL next year? Why? Can you please explain? Thanks

Firstly, thanks for sharing the point on DTL. I didn’t take that into account when making my sell decision. I did remember however that it wasn’t something to be profited from when I was trying to understand the concept of this DTL on special reserve introduced for HFCs.

So now I’ve studied this in a bit more detail. Thanks for making me do that - helped me understand it a lot better as well.

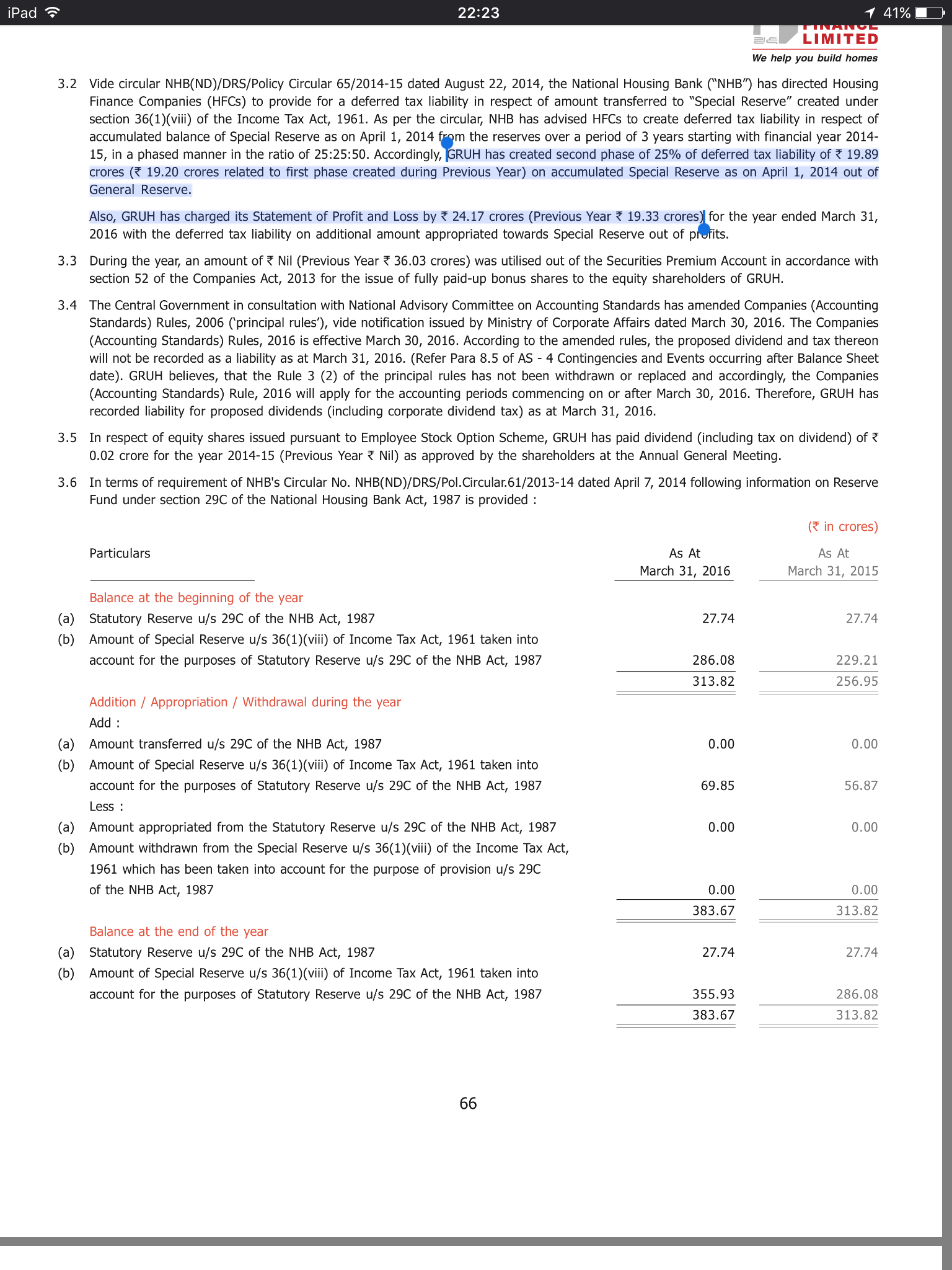

As per Sec 29C(i) of NHB Act, 1987 mandates that all HFCs must transfer atleast 20% of their net profit of that year into a special reserve before any dividend can be declared. (And HFCs from what I understand, have been deducting this 20% from their taxable incomes for the year and then arriving on net profit for that year.)

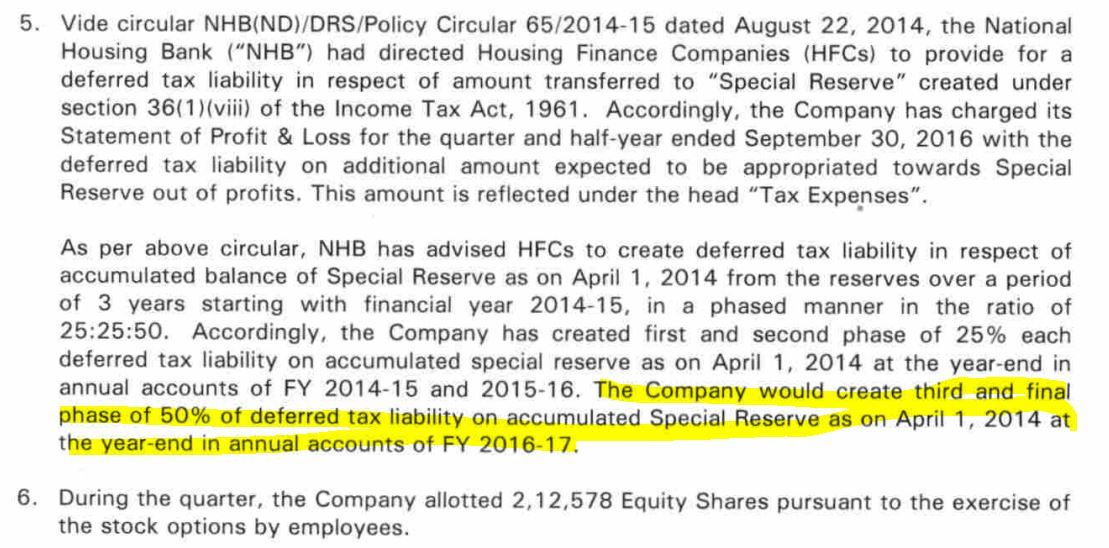

Post that, NHB has mandated via their circular in Aug 2014 that all HFCs who haven’t already accounted for DTL, need to account for DTL on their accumulated special reserves as of April 1,2014. Since this would have a big impact on profitability if it were done directly out of P&L and B/S, it has allowed this DTL to be created in a phased ratio of 25:25:50 from general reserves till FY17.

However, the above pertains only to the past i.e. DTL on accumulated special reserves till April 1,2014.

Since HFCs will be transferring 20% amount to Special Reserves every year, I’m quoting the below from NHB’s circular from Aug 2014 -

“DTL for amounts transferred to Special Reserve from the year ending March 31, 2015 onwards should be charged to the Statement of Profit and Loss of that year.”

Hence if you go through the Annual Report for any HFC who hasn’t accounted for DTL previously - you would see them accounting for DTL across 2 separate line items for FY15, 16 and till 17. One is through the General Reserves and other is from the yearly P&L.

See highlighted text from Gruh’s 2015-16 Annual Report.

So based on my understanding, Gruh would be accounting for DTL every year from their P&L post FY17 as well. It’s just that the transfer from General Reserve into Special Reserve will stop after FY17.

So based on this - I don’t think there’s anything wrong in my understanding of Gruh’s P/E or EPS. And thankfully doesn’t alter my sell decision in anyway.

Would love to hear from you if I’m understanding this incorrectly.

3 Likes

However, you can say that about 10% of profit of the company that is being deducted from profits on account of DTL, is a notional cost. Gruh may have sufficient Tier I capital even after providing for DTL in future. So, the actual P/E ratio should be about 10% higher. Depending on the current valuations, this brings a P/E of about 50x down to about 45X or P/E of 45x down to about 40x.

1 Like

Deferred tax liability (DTL) will continue post FY17 as well. Can anyone please confirm?

This ship continues its robotic march forward… 20% earnings growth without equity dilution… Trading at rich valuation currently…

3 Likes

GRUH and HDFC Banks are superb alternatives for FDs. They should be accumulated as and when marked mood swings negative and to be hiold for next 5 years without losing sleep. While putting money here following needs to be thought:

- An unpredictable bet with >20% EPS growth

- A predictable bet for near guaranteed 20+% growth

Above criteria should be used to put a % of PF towards such rock solid stories.

5 Likes

@lustkills : Sandeep bhai, Your notes are always a treat to read and easy to digest.Not only succinct but also does not leave much to say. Thank you!

@okhade …Manish Bhai, your words are a gem which reminds that investing is simple but not easy…I think people have lust for thrill forgetting that lust kills and do not ponder much on this sound advice.

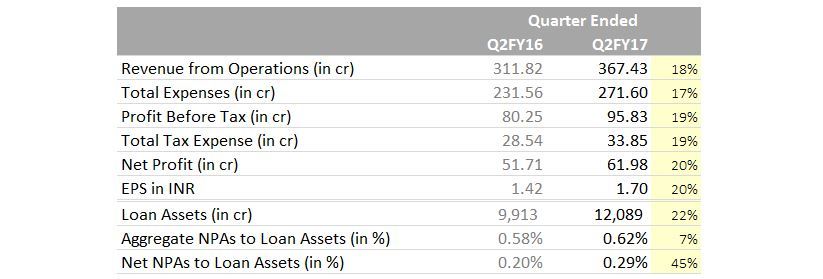

Need more understanding on Note 5 and 6 of today’s results (refer below image) and I am sure that you folks are the right brains who could help.

Note 6 : Equity dilution Via ESOP’s. Your 2 paisa’s on the same. How do you see it?

Note 5 : 50% deferred tax liability creation on Special reserves at the year end…Would that slow the 20% QoQ EPS growth?

1 Like

Yes, DTL will dent FY17 earnings to an extent.

Per Note 5, this amount is reflected under the head “Tax Expenses” of Q2FY17 results i.e. the co. has charged its P&L with the DTL amount. What percentage? Back of the envelope calculation says Gruh’s normal tax rate is ~27%. Anything higher is going to DTL kitty I guess. If true, then 20% earnings growth is after factoring DTL for half year (DTL deduction ratio is debatable though).

As Hiteshbhai says “in fy 17, provision is to be made of a higher magnitude but I guess by now most of market participants are cognizant of these facts. As long as growth comes about in topline I wouldn’t be too much worried about the other aspects. Much of these things ultimately even out over time.”

Market is forward looking. May as well start factoring relatively better earnings growth rate post DTL normalization period i.e. FY18 onwards.

Cheers,

3 Likes

So no DTL from FY18 for GRUH and REPCO?

Can’t say about figures, but for my 1st house loan Hdfc took 3 months. For my 2nd loan I went to Gruh and they sanctioned in just 10 days. Smooth, isn’t it?

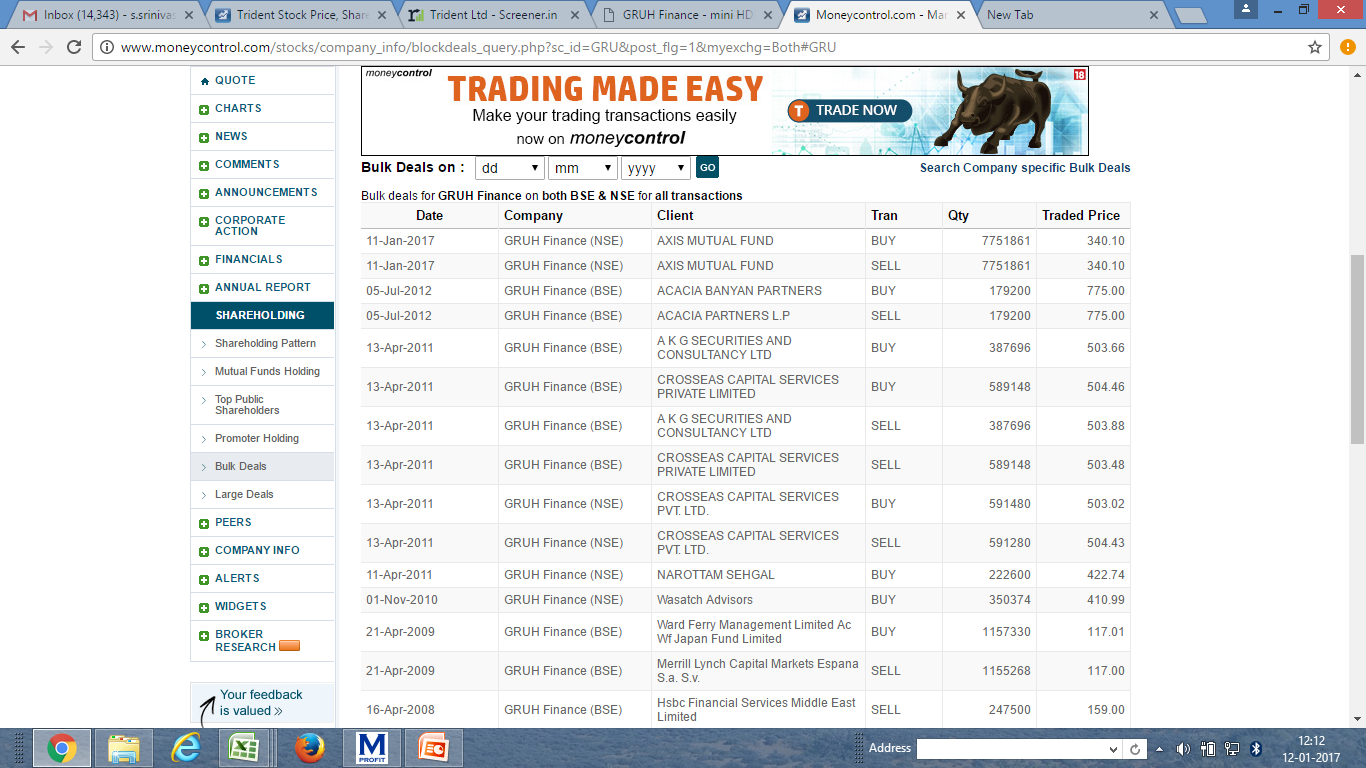

We saw a major block deal of 7821047 shares, which is approx 2.5% of available share for trading. The deal was Rs 344.60 per share, valued at Rs 269.51 crore on NSE. Can experts share their views on this huge change of hands? I understand that if BIG guys are investing @344.60, then obviously we have a better future

I think Govt is going to focus majorly on Rural Housing. That is buzz in the market and also PM also mentioned 2022 housing for all. There is a talk of giving Interest Rate subvention for 12L to 18 L income category too. All are speculations. Please apply your judgement.