Here is some analysis on HEG vs Graphite India on current quarter’s performance as well as what can be expected going forward.

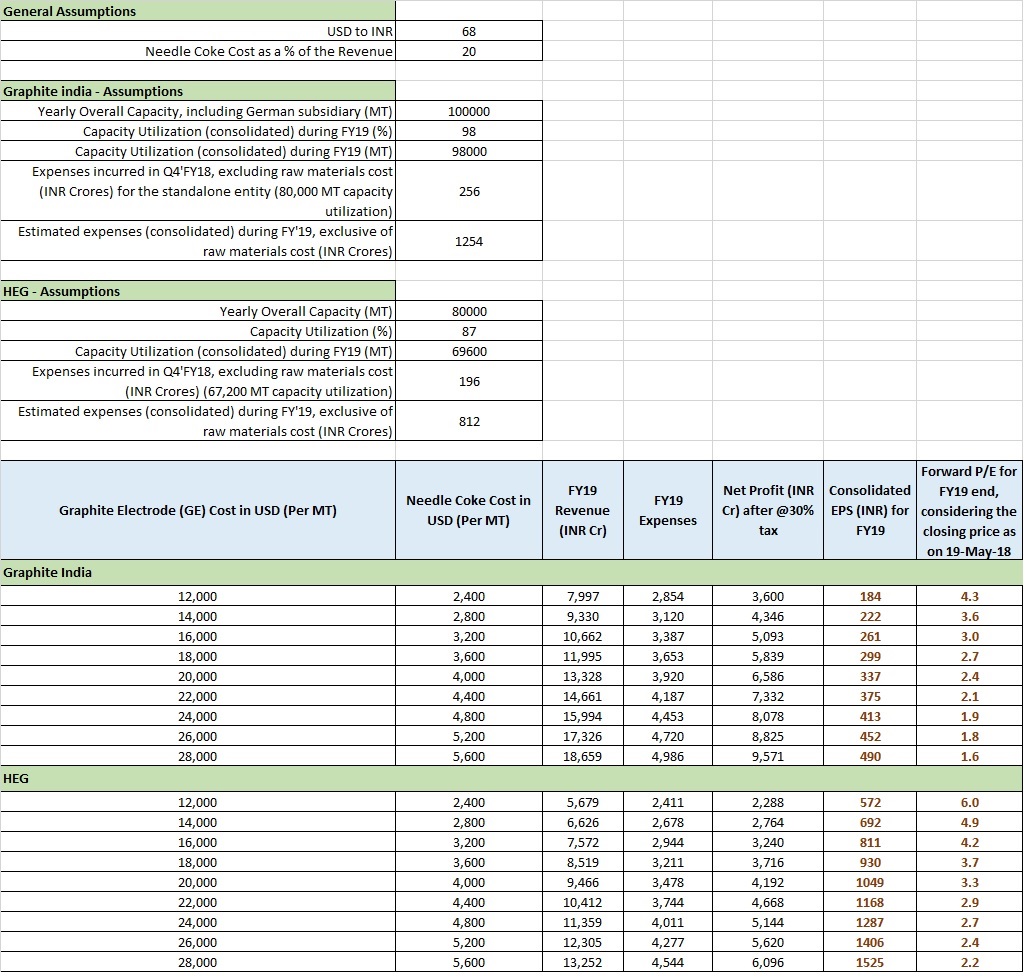

a) Standalone Revenue performance: HEG posted 1293 crores in revenues in Q4. Going by the company specified utilization of 85%, the company has sold 17000 tons of graphite electrodes at a sizable $11700 per ton, which is more than 4 times the price in early-2017.

GI: GI posted revenues of 1152 crores in revenues as pertaining to graphite electrodes. Given the company specified utilization of 100%, it has sold 20000 tons at $8860 a ton. This is what GI was referring to when they said that they have legacy contracts and therefore the lower rates.

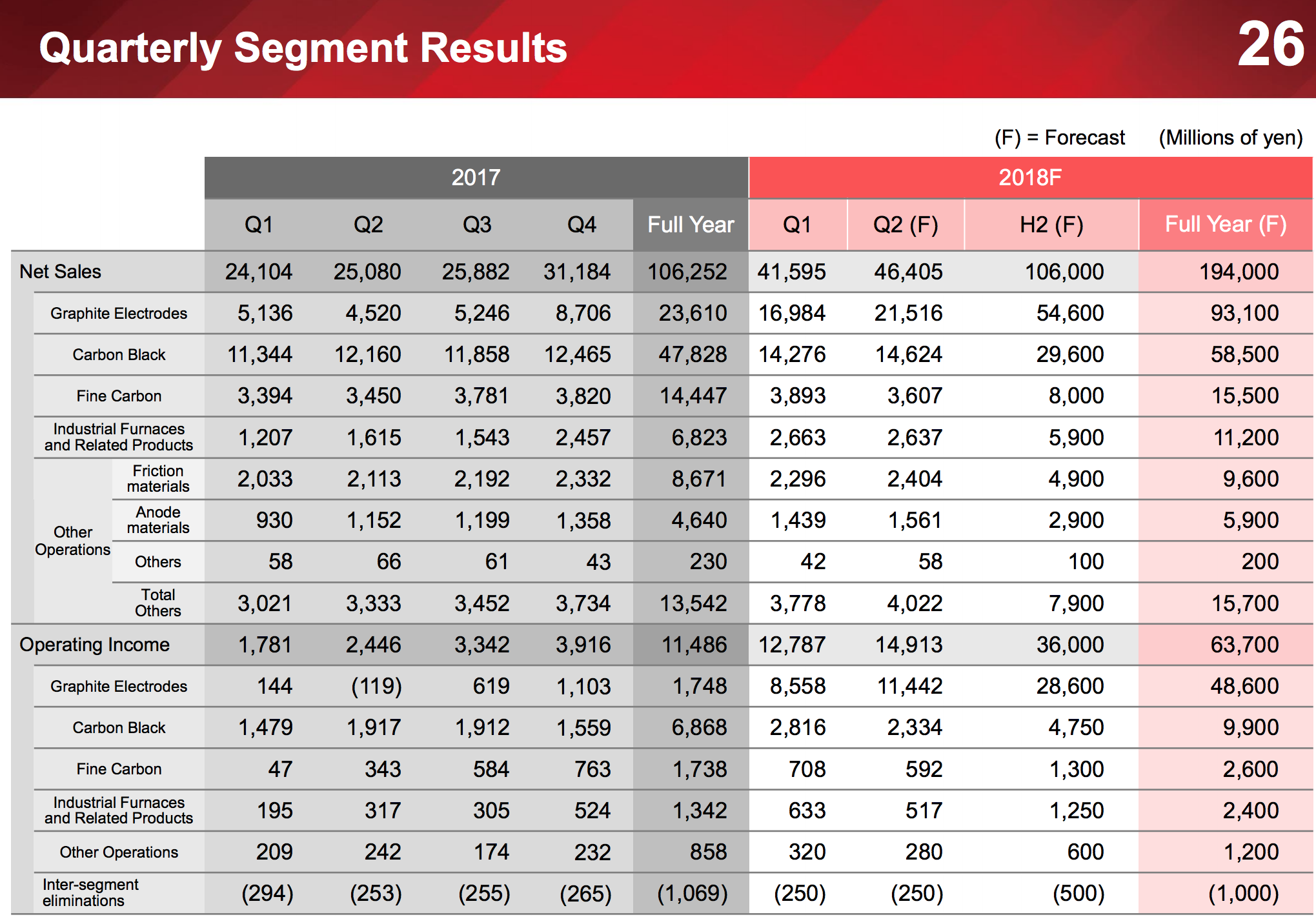

HEG has played the graphite electrode upcycle well. They stopped low priced long-time range contracts much earlier than GI. But starting next quarter, we will see some similarity between HEG and GI

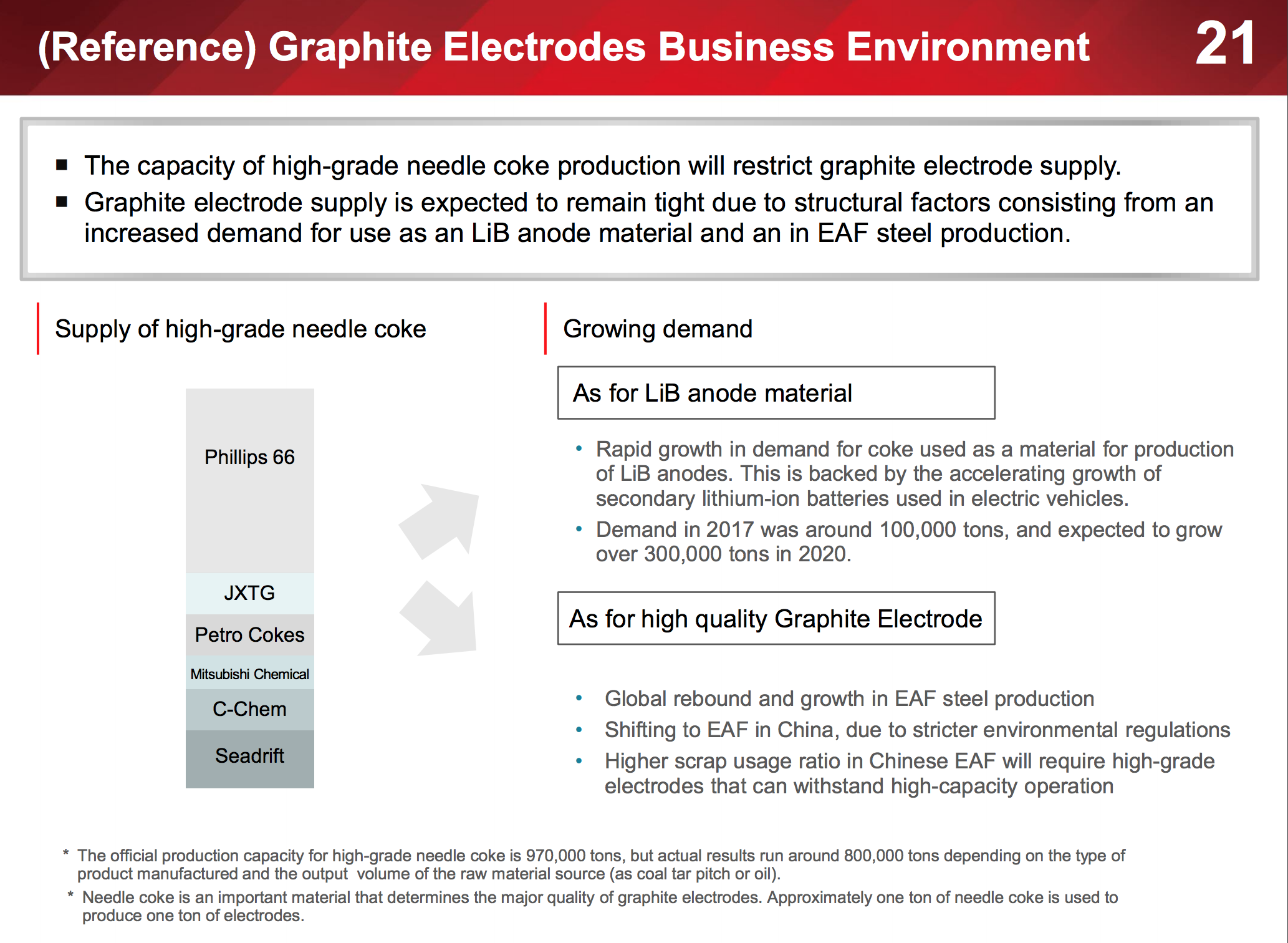

b) Cost of Needle coke: HEG again played this well. They stocked up on needle coke when it was at a low price, identifying the upcycle really well. At a cost base of 150 crores, the price of materials consumed works out to only $ 1320 per ton, which is primarily driven by needle coke

GI: GI, with a cost base of 300 crores, has paid approximately $2300 per ton for the price of materials consumed

c) GI has the same employee benefits as HEG and both are debt free as of today. The depreciation costs are negligible. GI has approx. 20 crores higher fuel and supply costs and an additional 30 crores in other expenses and consumption of spare parts, but this could be driven by the incremental sales of 3000 tons relative to HEG. GI’s subsidiary performance was not upto the mark this quarter but this will change starting next quarter according to the CEO

d) Here is where things will change quite a bit: The cost of graphite electrodes has shot up to $17000 per ton. The spot rates are even higher. This is as per HEG’s CEO. For HEG, even if cost of materials consumed goes up 5 times more than the current quarter, the incremental costs will be taken care of by the incremental revenue, and HEG can still post the same profit and EPS as it posted today.

e) Graphite India’s revenue will increase even more and approximately double as the legacy contracts expire, based on above numbers. The subsidiary will further add 20% to the topline, but will have additional manufacturing costs as it is located in a developed country (Germany). Since the needle coke manufacturers have moved to quarterly contracts due to increased demand, the cost structures of both GI and HEG will remain the same. GI might make more profits due to higher capacity starting next quarter

f) All the above is contingent on graphite electrodes prices being high and this needs to be closely watched.

g) GI has an edge with respect to the following parameters: 1) It has cash and financial assets worth approx. 1275 crores while HEG has 250 crores (Book value of GI is 850 crores higher). 2) It is better vertically integrated and has inhouse Calcined Petroleum Coke manufacturing that is used in electrode manufacturing and 3) It has already invested in value added carbon products used in auto, aerospace, chemical and other industries while HEG has now started doing so.

Disclosure: Hold both HEG and GI in a ratio of 2:1

and not to mention HEG MD coming often on business news TV? IMO i think he should concentrate more on his business

and not to mention HEG MD coming often on business news TV? IMO i think he should concentrate more on his business