@Gaurav_Agarwal,

The rate of $15000 per ton is an assumption made on the basis of the conference call conducted by HEG mgmt in the following link. (Page 21 has some details)

With respect to Tokai Carbon, their realisations on the basis of your calculations are quite low. While their website mentions annual capacity of 96k tons, I suspect capacity utilisation is lower than 90%.

I was not able to find details on how many tons they have sold, however, I did get some data on the price realisation as of Dec 2017 in the link below (which should have been realised in Q2 and later)

32-28 inch 24-18 inch

920,000 Japanese Yen / metric ton 900,000 Japanese Yen / metric ton

(d) Others:

16 inch and below 1,300,000 Japanese Yen / metric ton Shortening of payment term

The above works out to $8275 and $11700 per ton but the data is dated. This also leads me to believe that capacity utilisation is lower than 90%.

1 Like

I think, recent listing of Graftech has helped in getting the attention of many major research firms on the Graphite story. As per the following article, brokers have set a twelve-month consensus target price of $25.67 for the company. JPMorgan has even set an “overweight” rating and a $29.00 price target on the stock. Stock price has increased almost by 30÷ since its listing last month. Other Graphite companies like Showa Denko and Tokai Carbon also have increased by more than 20÷ last month.

GI/HEG will be in ASM from June 1st with 5% circuit and 100% margins levied with other bunch of stocks

HEG Investor presentation 19 June 2018.

1 Like

Indian graphite electrode sector - Macquarie.pdf (2.6 MB)

Recent report from Macquaire on Graphite stocks

1 Like

Please find my Earnings calculations for Graphite India (GI) and HEG in the attached pdf. For various Graphite Electrode (GE) price realizations and two scenarios of Raw Material prices, the pdf will provide you the corresponding earnings for 3 separate years- FY19, FY20 and FY21. The two scenarios are the following:

Scenario 1: Raw Material price assumed to be 15% of the revenue, as it was the case for HEG in Q4’ FY18. This would get us the most liberal estimates

Scenario 2: Raw Material price assumed to be 32% of the revenue. This would get us the most conservative estimates

The pdf contains all the assumptions made by me in an elaborate way, which we can discuss, if you have any inputs:

Graphite India & HEG Earnings Calculations.pdf (359.6 KB)

Please note that, these are just calculations and no way I am recommending these stocks.

Disc: Invested in both Graphite India and HEG

2 Likes

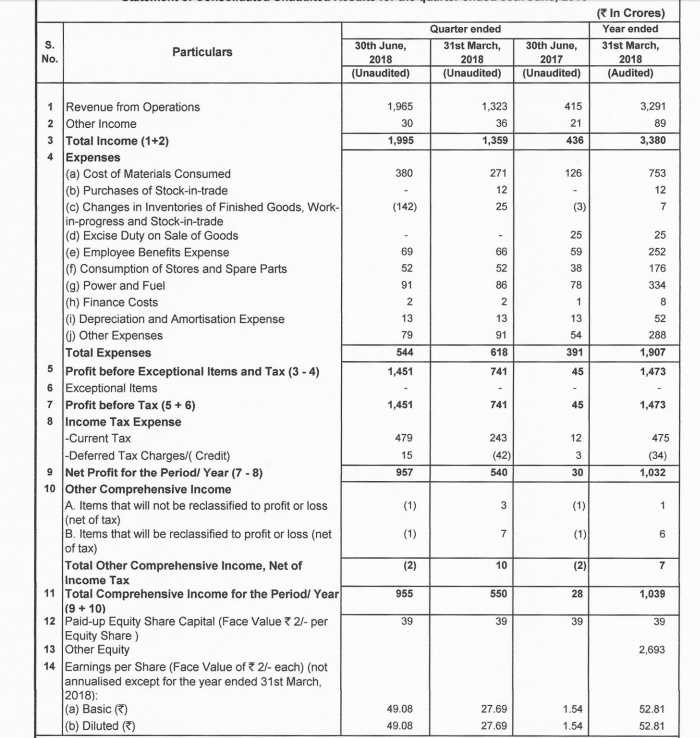

Unaudited results for Q1FY19.

QoQ compared to March 2018.

22.8% increase in revenue

21.5% increase in PAT

21.5% increase in EPS.

OPM increased to 74.12% from 71.12%

HEG’s operating profit shot up 4975 percent year-on-year to Rs 1,187.6 crore and margin expanded sharply to 74.8 percent in Q1FY19 from 11.4 percent in Q1FY18 and 73.6 percent in Q4FY18.

BloombergQuint

HEG Says On Track To Meet Growth Forecast

HEG is out of ASM from today

Disclosure: Not invested

Hello Sir,

How do you see this move by GI?

Knoxville, Tennessee-based General Graphene has developed a proprietary technology to produce large, low-cost graphene sheets for commercial applications. The material is currently not available in commercial volumes.

SIR in present time how can we evaluate the company particularly in context of cost- benefit metrics and future risks

Difficult to comment without knowing further details about the Graphene and its product acceptability in the market or its market size and margin profile.

2 Likes

Please find attached, my estimates for Q2 and the projections for the period till Mar-21 results.

Graphite India & HEG Earnings Calculations (9-Sep-18).pdf (407.1 KB)

Please find below (for your easy reading) , the Summary, as provided in the above pdf:

The only 4 key variables that majorly influence the earnings for GI and HEG are the following:

- Graphite Electrode (GE) price realization

- Raw material cost (primarily influenced by the needle coke cost)

- Capacity utilization

- INR to USD conversion rate.

Rest of the parameters are more or less fixed in nature and will not make a major influence on revenues/profits from quarter to quarter.

Expenses side of these companies include following two categories:

- Raw materials, including needle coke. Like GE prices, needle coke prices also have risen significantly over the past one year. Corresponding to a GE spot price of USD 2,500/MT in early 2017, needle coke price was around USD 450/MT (18% of GE price). By May-18, GE spot price touched $25,000/MT and needle coke was 3,200/MT (13% of GE price). Hence, the trend for the past year has been that, GE price increases at a faster rate than needle coke price.

- Non-raw materials related expenses (Employee, Power, Manufacturing etc.). These expenses are somewhat proportional to the capacity utilization, and do not drastically vary from quarter to quarter.

As per my best judgement, GI and HEG will be able to keep on increasing their GE price for the next few quarters, without any difficulty. Given below are the key reasons. I also judge that, HEG will have an average GE price realization of at least $16,000 per ton in Q2 and at least $17000 in Q3. GI should have a price realization of at least $15,300 in Q2 (as they sell more domestically currently) and at least $16,500 in Q3:

-

Needle coke prices are likely to increase. Any increase in raw materials prices will be passed on to the customers. Also, these companies are likely to use formula-based pricing in their contracts to take care of the raw material price increase (GI has already pioneered that). Raw materials cost increase can reduce the EBIDTA margin slightly, but the earnings are likely to increase still. For example, for a $300 increase in raw materials cost, GE pricing may be increased by $1000. This is possible, since we are in a supplier’s market, and EAF usage is expected to increase for the next many years (even China estimated to migrate to more than 30% EAF by 2030, from the 6-7% in 2017) and there is no real substitute for the UHP, and increasing of capacities will require high investments and also will be very difficult (given that, the technology is not shared) and time-consuming.

-

From the Commerce Dept. data, it looks like, GI and HEG still had some contracts with low price realizations in Q1 (between $10,000 and $15,000). I expect them to completely come out of those contracts in Q2, and have all the contracts in the range of $15,000 to $20,000

-

Spot prices for 600mm diameter GE, as per Graftech last earnings call was between $15,000 and $20,000. HEG and GI also produce GE with more than 600mm diameter (and also, electrodes made to suit customer specifications), for which the prices will be much higher. In general, these companies are expected to sell at least 30% of their product on spot

-

Also, as per the Outlook provided in the Graphite India subsidiaries results (Foreign Subsidiary Accounts - IV.pdf) available at their website (http://www.graphiteindia.com/View/investor_relation.aspx), they are expecting 200 Million Euro sales in FY19, for sales of 15,775 MT, which translates to approximately USD 15,000/MT.

-

As the CMD of HEG reiterated many times, China is unlikely to have the capability to produce the same quality grade of UHP which GI and HEG produce. As per my calculations using the 2017 data, about 6 to 6.5 kg of the low quality GE produced by China is required for producing 1 MT of steel, as against only 1.5 to 2 kg of the GE produced by GI and HEG

-

As the antidumping duty on GE has been revoked by India recently, GI and HEG will be able to export more of UHP grade GE for much higher prices, going forward. Currently, they are selling HP grade GE to small scale steel producers in Indian market for subsidized rates. With these domestic manufacturers being able to import HP grade GE from outside, pressure will be less on GI and HEG to sell domestically. We can expect at least $3000 higher realizations per MT of GE, due to the above advantage, on the quantity they are able to export more

-

Russia, just recently renewed their anti-dumping duty on import of GE from GI and HEG, mentioning that, they are selling a sizable quantity for a price of more than $20,000 per ton

-

If we study the Commerce Dept. data published recently, there are big quantities of GE sold to countries like Spain, Turkey etc. for average prices more than $17,000, $16,000 etc. in Q1 itself. As per a recent news article, prices have been increased by at least $1000 in Q2.

-

As per the anti-dumping Final Findings report from Department of Commerce (published on 8-Aug-18, available at http://www.dgtr.gov.in/sites/default/files/FF_NCV.pdf),average selling price range of GE in India (which includes HP grade also), is from $14,700 to $16,500 per ton

-

MD’s of both the companies, in their interviews on TV channels had expressed confidence of increasing prices quarter by quarter for the next few quarters

-

Winter is nearing in China, when GE production will be curbed. As it happened during FY18, there is a chance of GE spot prices sky-rocketing

-

Based on the scrap iron availability, McKensie in early 2017 had estimated that, China EAF steel production will reach 30% by 2030 (as against 6-7% in 2017). Subsequently, China intensified its crackdown on pollution and has even set a target of achieving 20% EAG by 2020 itself. Effectively, this could mean that, more than 30% EAF would be possible by 2030. This means, effectively, around 270MnT of steel. As about 6kg of China low quality GE is consumed for production of 1 Ton of steel, this would require that, China would consume around 1,620,000 MT of GE in 2030, if it has to reach 30% EAF production. Even in India, EAF usage is increasing. As per the anti-dumping Final Findings report from Department of Commerce, demand for GE in India will rise to 120,971 MT in 2019 (from 105,066 in 2017)

For HEG, in Q1’19, raw material cost was just below 18% of the GE price. Even if I expect the GE prices also to increase in tune with the raw materials cost in the future, we would also like to understand the impact in earnings, if the raw materials costs increase significantly in the future in a disproportional way. Hence, the estimates provided below cover two separate scenarios: Scenario-1 assumes a raw material cost to be as 18% of the GE price and the Scenario-2 assumes it to be as 25%.

17 Likes