HEG seems to have stabilized at around Rs 2915, so about 9% down.

Does GI management never give an interview? Have not been able to find any from them, interviews from Mr Jhunjhunwala (HEG) though can be found a lot …

HEG seems to have stabilized at around Rs 2915, so about 9% down.

Does GI management never give an interview? Have not been able to find any from them, interviews from Mr Jhunjhunwala (HEG) though can be found a lot …

Both do manufacture UHP Electrodes. See this where it says “Your source for world class UHP Electrodes”

and this for Showa Denko where it says “our company is committed to developing a production of Ultra-High Power (UHP) graphite electrodes of Φ600mm and above diameters”.

Tomorrow one will witness a vertical recovery in HEG. There is no high grade needle coke (the stuff you need for UHP) available in the market. As a result of this no one has the stomach to setup new capacity. Things are going to stay like this for a very long period of time indeed. Anyone missing this dip today is going to rue it 15 days from now. my 2 cents

Really different and interesting views from both of you - my questions are:

a) Do you disagree vastly with the price estimates given by Nomura in their report, the price/MT is way lower in those and estimates on this thread

b) If the original thesis for GE stocks going up was pollution crack down in China and if now the information is that output is being ramped up again, then that thesis now is broken right?

c) If Showa Denko and Tokai Carbon were also manufacturing UHP electrodes and they saw a 15/16% correction today and if Nomura’s report is to be believed more correction should be expected, then why would HEG/GI not also see steep fall going forward?

d) Mr Jhunjhunwala is his video sounds confident - but I find it difficult to believe that Nomura’s report is not a big red flag for both GI and HEG

@Gaurav_Agarwal @madhavikkutti @pandi.rao @phreakv6 your views also please …

PS: I want to believe that the story is still alive, but unable to convince myself and hence asking

Factors why we are in a structural supercycle

Needle coke is the most important input here and since it is so scarce (and in a supercycle of its own driven more by demand side factors and hence unlikely to turn soon) manufacturers are not exapnding capacity

There is a shift from blast furnace to EAF which is aiding growth in electrode consumption. It is not only supply side change

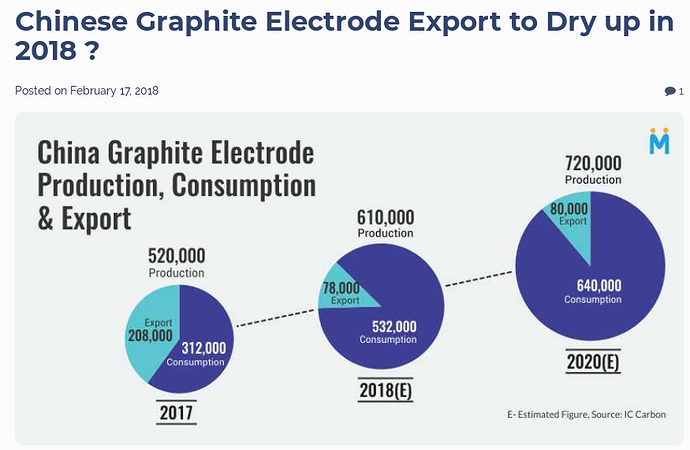

China is predominantly non UHP and hence an increase in output here does not affect anything

Needle coke shortage -

a) can it not actually lead to a reduction in spread for GE players? (though Mr Jhunjhunwala clarified that HEG expects spread to go up)

b) If no one can add UHP GE capacity in the next 2/3 years, then yes the expectation that prices will go up in the next 2/3 years is right. In that case why Nomura so bearish on prices in their report?

There is a shift from blast furnace to EAF which is aiding growth in electrode consumption. It is not only supply side change

if I understand this right

a) Rest of the world is already on EAF, only China is moving to EAFs now. Also, EAFs can use HF GEs as well (though not as efficient as UHF GEs - EAFs can still use HF GEs)So if China HF GE capacity is restarting (the reason why UHF GEs from GI and HEG increased in price) then will this not certainly lead to price erosion - exactly as predicted by Nomura?

a) if this is the case then why did China GE facilities shutting down, increase GI and HEG UHP GE prices - in that case, prices would have remained the same as in say 2015. So the inference is that China output whether HP/UHP does have a major impact on UHP GE prices? Is this inference wrong?

a) How can one disagree with Nomura’s view when they claim to have visited China to come up with their estimates and we are sitting in the comfort of our living room? If it was some other source, their agenda might be questionable but since its Nomura, its at least relatively a trustworthy source.

b) There is still a pollution crackdown and China is moving to EAF for manufacturing steel and I don’t think there is any change in that. However, China seems to be ramping up needle coke capacities and that should bring down the main raw material cost in manufacturing UHP electrodes. This should bring down the prices in the interim.

c) This was my thesis as well for exiting today.

d) (I saw Jhunjhunwala’s video after I had sold so my interpretation might be biased.) I don’t think he knows the latest from China and he is going by near-term prices (next couple of quarters) whereas Nomura is talking about 2019 and 2020 prices. Cyclical commodities are very sensitive to peak and knowledge of peak earnings and it looks like peak earnings is going to come in 2018. Market will have to price that in putting in a top based on that knowledge.

China seems to be ramping up needle coke capacities and also setting up manufacturing for electrodes (I don’t see why China can’t setup UHP electrode capacities by 2020 even if they don’t have any currently). Also, if needle coke is scarce and is priced high, I don’t see how Graphite India/HEG can benefit from it since its their raw material. At best they can pass on the cost to customer. It can make their topline look good but I don’t know if they can squeeze the Customers further on an already higher price.

I sold in the morning today so views could be extremely biased. It was easy for me to make the decision since I was averse to losing my profits and was alright even if there was more steam left here, being a Satisficer and not a Maximiser.

Hi @VP_amit, I completely exited Graphite India today morning, immediately after I observed the meltdown in the prices of Showa Denko and Tokai Carbon. I exited not because I blindly believed in what Nomura said, but I was expecting GI and HEG also to correct massively, as a reaction to the above event as a knee-jerk reaction (I don’t believe that the correction is fully done yet).

Though I sold off my positions, my unbiased opinion is this: What Nomura said may be applicable to Showa Denko and Tokai Carbon, but may not be applicable to GI and HEG to that degree, as Nomura was possibly refering to lower grades of both Graphite electrode and needle coke, which the Indian GE producers are not concerned with.

Nomura_910466.pdf (202.9 KB)

Nomura’s report on GE.

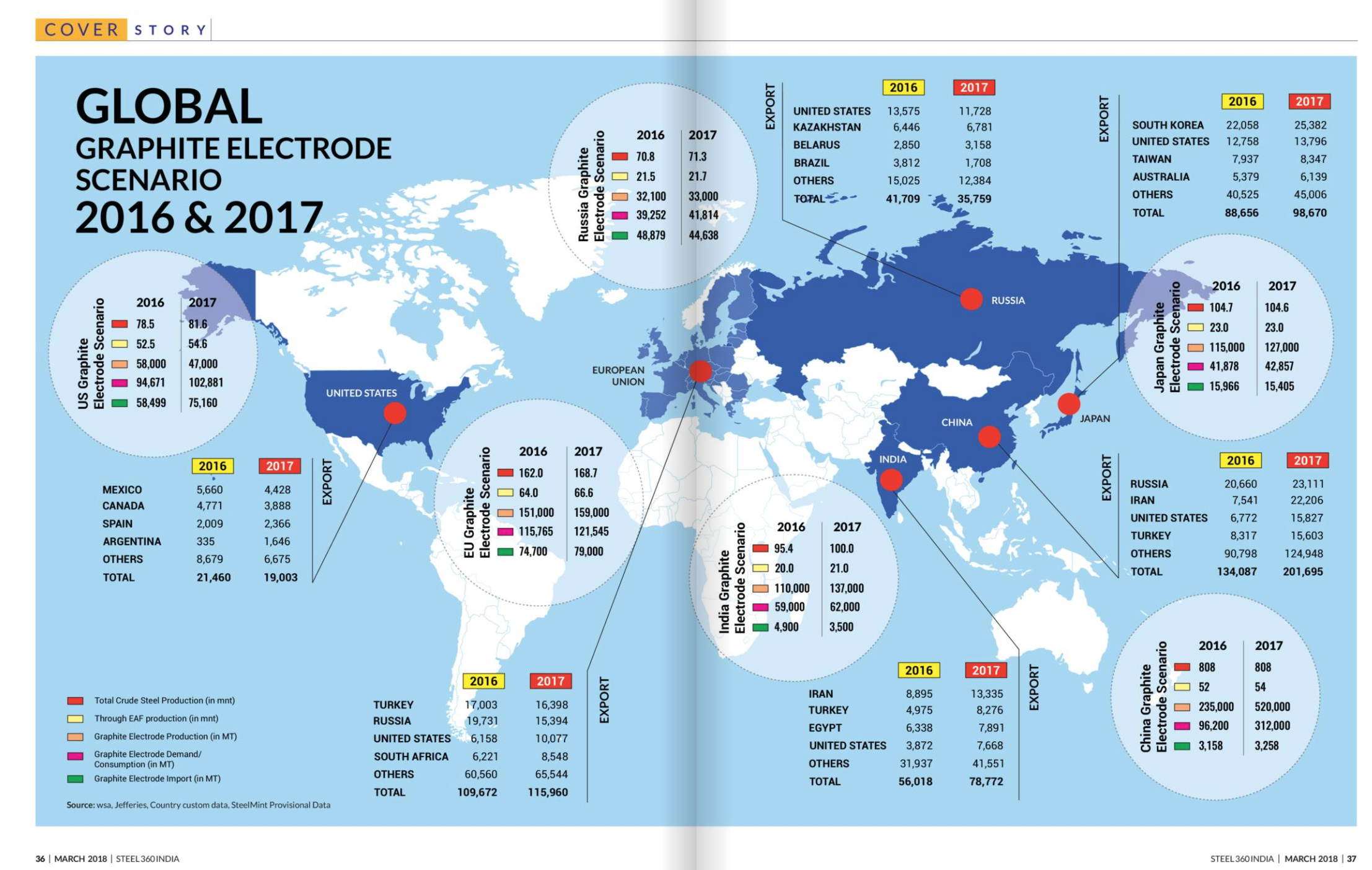

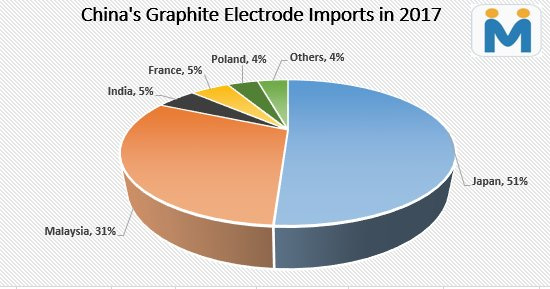

China is importing 51% of its requirement from Japan and India’s share is only 5%. In the event of China capacity coming on stream, Japan is most likely to be afftected more than India. As Global steel demand is in upswing, there maynot be crash of prices for next 2 to 3 years. HEG management is reitrating this point that India will be least afftected. Nevethless the sentiment is dented and we may expect price volatality going forward.

Unfortunately this is not how global commodity trade works. If we export to US and Japan exports to US as well, in the event of Japan not being able to export as much to China, it will then look to export more to US and this will drive prices down for Indian exports to US and the commodity prices worldwide would stabilise then at a level downward. This is of course assuming countries don’t have export and import levies which distorts the Supply-demand scenarios. But overall supply-demand of the world will dictate the commodity price even if Indian supply meets Indian demand as long as there are no additional levies.

good point.

Also @Raj_A_A

a) What is the source of the info you shared?

b) in KT - how much is the 5% of China import? i.e if HEG and GI are combined producing say 160KT/annum, how much are they exporting to China. 5% of China imports could be a very high % of India exports? Mr Jhunjhunwala in yesterday’s video though said nothing was being exported to China by HEG

@VP_amit

It is a tweet by Steelmint (@SteelMint)

Are Chinese Steel Mills Eyeing Indian Market to Import Graphite Electrode …

6:04 AM - 30 Mar 2018

Are Chinese Steel Mills Eyeing Indian Market to Import Graphite Electrode ... pic.twitter.com/qkoLoVkbrx

— SteelMint (@SteelMint) March 30, 2018

Here is what Graftech mentions in its Form-S1 (https://www.nasdaq.com/markets/ipos/filing.ashx?filingid=12660117): “Electrode production globally (excluding China) is focused on the manufacture of ultra-high power (or UHP) electrodes for EAFs, while the majority of Chinese production is of ladle electrodes for BOFs. The production of UHP electrodes requires an extensive proprietary manufacturing process and material science knowledge, including the use of superior needle coke blends. As a result, graphite electrode producers inside and outside of China are generally not in direct competition with each other for major product lines.”

Excellent read. They have sold out most of their capacity at ~9-10K per MT for the next 5 years

Here is my two cents on possibly trying to arrive at some sort of fair value for Graphite India using comparable.

Graftech is about to get listed on the NYSE starting 19th april. In the prospectus as part of the forward looking statement, they estimate first quarter which is Jan-March 2018 ebitda to be 275 million dollars with a 43000-44000 tonnage of volume. Quarterly volume for Graphite India should be 22500 assuming 92 per utilisation for the entire year. Graftech’s revenue per tonne as they estimate is 10250 dollars per tonne as they sold most of their capacity as long 3-5 year contracted rates of 9800-10000 dollars a tonne. It is safe to assume Graphite’s per tonne revenue will be a bit higher they have booked more aggressively.

On the other hand, Graftech’s captive needle coke lends them to a lower cost of goods sold. They have pencilled in 2600 dollars per tonne of needle coke cost for the 1st quarter.

Assuming these two counter forces, it will be safe to extrapolate a similar revenue/absoute ebitda profile for Graphite India.

44000 tonnes - 275 million dollars

22500 - approx 140 million dollars

If we annualise these numbers for just fy19, we get a ebitda of 560 million dollars for Graphite India.

Graftech at the mid range of its ipo price is asking for a 7.5x ev/ebitda. Giving a 25 per discount to the indian players since they are not backward integrated,

target ev for graphite india comes to around 560 * 5.5 = 3.1 biillion dollars.

Target market cap of 3.2 billion dollars because they have 100 million dollars net cash.

That still gives us a target price of 50 % higher than the cmp.

Ofcourse this is just a very simplistic way of trying to arrive at a fair value. Key will be how sustainable these sort of spreads are. These numbers would entail a gross spread of 8000 dollars a tonne. If the market is confident that 8000 gross spread is achievable for atleast 2-3 years, slowly and steadily it can possibly trade at 5.5x ev/ ebitda.