Many thanks for sharing your views. Cyclical industries need consistent supervision. I have neither the skills nor the willingness to be able to preempt the top of a commodity up cycle. Hence, I tend to be over cautious.

As always, to each his own.

1 Like

Global Graphite Electrode market is expected to exponentially increase from US $ 5 bn to 27Bn by 2022. GI/HEG in sweet spot. (Coutesy info: Mr Pankaj Singhal)

Hi @deep86 are you referring to earlier post related to China to add GE capacity.

The article does talk about the supply crunch even after the new capacity comes on stream, can you please let me know if there is a disconnect.

Even if new capacities come in China,its not going to export at earlier level as it now requires more GE due to new EAF facilities.

1 Like

Graphite electode company takes two years to start production from plan execution level…so even if any company thinks of adding capacity, there is no worry till two years

This puts these two company in sweet spots…

1 Like

Check HEG concalls. This has been discussed multiple times in it

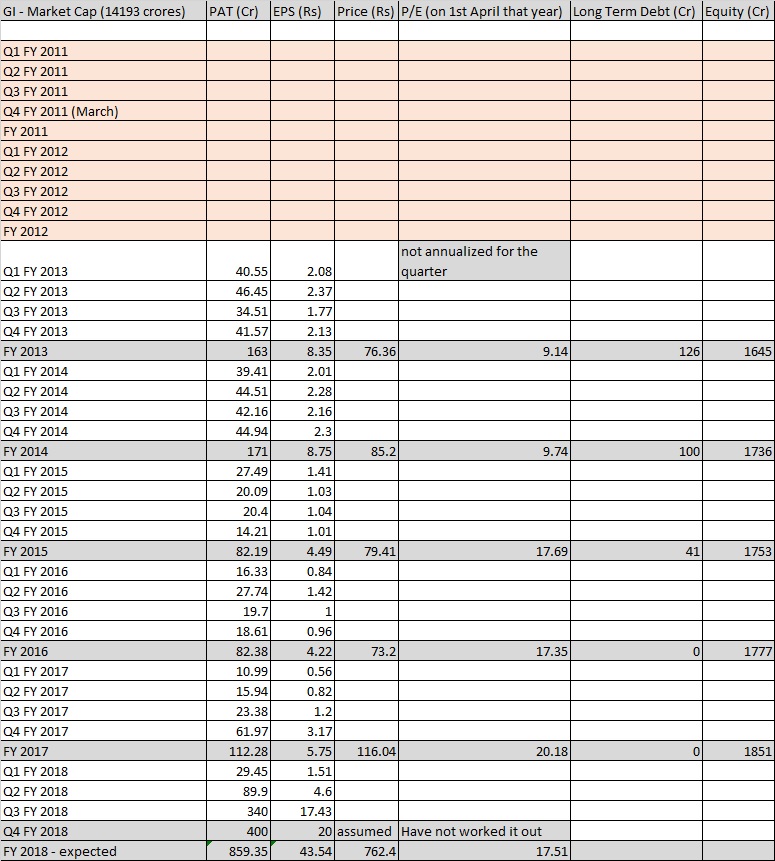

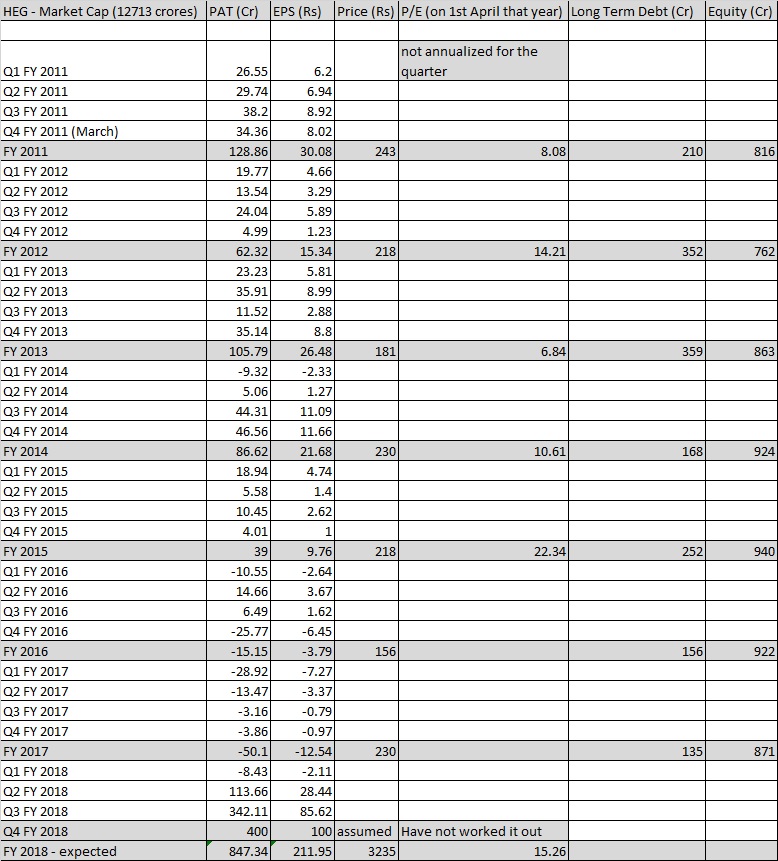

These are HEG historical quarterly numbers, earlier one was GI.

Observations:

- GI has a much better balance sheet, 0 long term debt since FY 16

- Many of HEG financial reports have been signed by different Accounting Firms - should this be a concern? All GI ones are by PwC - though PwC does not cover itself in glory, but atleast its one firm

- Could only find GI reports since FY 2013 on their website, they have never had -ve earnings since then, HEG has had -ve earnings in both FY 16 and FY 17!

- Have just assumed a rough Q4 FY 18 earning and eps based on the Q3 FY 18 trend, based on this HEG is at about 15 PE (TTM), GI is at about 17 PE (TTM)

- Assuming Q4 FY 18 is maintained for all 4 quarters of FY 19, the current price for HEG is about 8 PE (forward), GI is about 9 PE (forward)

- These 8/9 kind of PE multiples have been their multiples in earlier high earning years (earnings were much lower than FY 18, though high for those times (HEG in FY 11, GI in FY 13, FY 14))

… considering the above not sure if a lot of upside is left? For more upside, to me it seems, Q4 FY 18 earnings have to be much higher than Q3 FY18 and then need to sustain for a long time …

… is it time to be careful then instead? …

1 Like

Anyone knows when are the Q4 FY 18 results being announced for HEG and GI? Considering today’s move (GI: 5% up, HEG: 1.5% up) seems like the Q4 2018 results will be good, however the question is how long can these earnings be sustained and how will market price these stocks going forward as ultimately the GE prices will come down and both of them have already run up a lot.

1 Like

Hegs management already said that q4 will be better than q3

Looks like, both Showa Denko and Tokai Carbon down more than 15% today:

2 Likes

Wow! - is this verified news (in terms of China production ramping up faster than expected for Graphite Electrodes)?

Exited Graphite India completely in the morning to preserve profits. Waiting till August for LTCG felt too risky after seeing Showa Denko in the morning.

This looks like a drag on the GE story from GI and HEG standpoint, more production from China would bring down the demand-supply gap.

1 Like

Don’t panic on HEG. NOmura report addresses high powered electrodes. HEG and Graphite are manufacture UHP ( ultra high powered electrodes that China doesn’t manufacture)

No need to panic at all. HEG is still at <5 EV Ebidta and <10 PE one year forward.

Japanese manufactures both:

Tokai carbon & Showa denko are at valuations north of 30x PE.

We checked with local procurers of UHP electrodes prices are still the same and strong.

4 Likes

- So the Japanese producers Tokai and Showa do not produce UHP at all, or they produce a mix?

- when you say Showa and Tokai are at 30x PE, is it one year forward or TTM? Both Graphite and HEG are also at around 30x PE (TTM), I year forward ofcourse they could be around 10 based on the prices in the next 4 quarters …

- Any links you have to the Nomura report?

Following the orderbook today for Graphite India from NSE - only selling happening at LC

| Buy Qty. | Buy Price | Sell Price | Sell Qty. |

|---|---|---|---|

| - | - | 721.75 | 5,41,776 |

2 Likes