21st of March: Release of 3.59 crore pedged shares.

22nd of March: Pledge of 4.76 crore pledged shares

Looks like transfer of pledge and additional pledging.

Pledging had come down materially from Sep to Dec.Previously, the management had guided that they will bring down the pledge by Q4FY18. Thus the status as of March will throw more light.

The Gagillapur and Jeedimetla facilities located at Hyderabad, Telangana has completed the USFDA inspection from 19th March to 23rd March 2018 with zero Form 483 observations for Gagillapur facility and with One Form 483 observation for Jeedimetla facility.

We have seen granules digested all good news in recent past without any impact on price movement. It will be interesting to see how it behaves on the observation received for Jeedimetla.

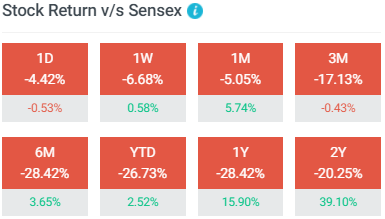

Touching 52 week low just ahead of annual result announcement is not a good sign & that too with following data which shows consistent negative performance v/s major indices for last 2 years.

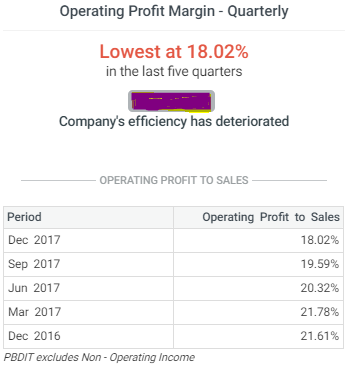

It was considered to be a good bet for long term & many fundamental and technical analysts spent sleepless nights analyzing it from various aspects. Below data shows that profit margin has also dropped consistently for last 5 or more quarters. If price movement is any indicator of upcoming result, we may see this negativity continuing in near future as well

We are regularly under performing sector as well. The FII holding has gone down considerably along with promoter pledging increasing, although pledging has seen a jig-jag movement in recent years.

Despite having so many negatives, we still see retail participation increasing in the company. While I feel that breaking psychological level of 100 will create major negativity & it may find tough to scale back in 3 digits. I will keep fingers crossed for upcoming result & next 2-4 quarters and have a keen watch before taking decision of dumping it & moving forward with bitter costly learning

My opinion is there reports Wich are available for free to everyone are not actually research reports, but an indirect recommendations predecided and report made accordingly.I have lost in most of these buy out done on the basis of these reports, sprtulsian and Gujral recommendations.Till the other day, everyone was recommending pcjewellers.They just recommend on the basis of reported financials and nothing else

Yes. Breakdown below 100 is definitely a strong sign of impending downfall. But Incase the story is there, it’s a buy.

Recent stock price move prompted me to go back to the transcript. Raw material price pressure, omnichem slowdown and high debt are here to stay, although the management tries to dance around this promising growth after 2020…which no one can predict.

I hope this doesn’t become another Kwality… High on promise n hype. The only silver lining is that the addressable opportunity is huge and Granules has good processes in place and succession planning

In the transcript, the management mentioned that they’re not diluting capital further, focus will be on cash flows and things will fall in place albeit on delayed basis relative to initial expectations. Incase the management is honest and can achieve this, the stock is cheap currently.

Granuels API capacity utlization is running at 100%. With new API capacity, it is expected margin to improve as most of it will be consumed in house to manufacture finished dosage. But with now crude oil prices moving north, there could be pressure on raw material cost.

I don’t know how they’ve built their projections. Ideally they shudve forecast crude at at least 67. Plus the forex impacts. These are important factors in capital budgeting

The management has indicated in last few conference call, that they pass on the cost to the client. However, it may take few quarters before the higher raw material cost passed on.

I think increase in oil prices seems to the reason why the stock is trending lower currently.

One of the concerns I always have is how much to believe the management’s words from concalls. Secondly we don’t know what is cooking inside the company until news comes out in public domain. Hope that this management is actually sound. Seems to be doing the right things with patience and focus

Granules has always had poor pricing action due to fairly high promoter pledging, many punters constantly sell down the stock without knowing the reasons for pledging. this is not a reason to sell.

while the forecasted growth from new ventures has been delayed , the core business is very much intact and is more than sufficient to justify current valuation, important to remember that For Lupin, Aurobindo etc. the core business was/ is getting hammered.

a big positive is that management has clearly said that they will neither be taking debt nor raising equity in the near future, full focus will be on executing current business.

interest cover for q3fy18 was 8x, debt is not an issue and will be reduced further in coming quarters

one needs to study their annual reports from late nineties to see how they have delivered against promises, my read is that while they do have a tendency to get carried away, they ultimately deliver.

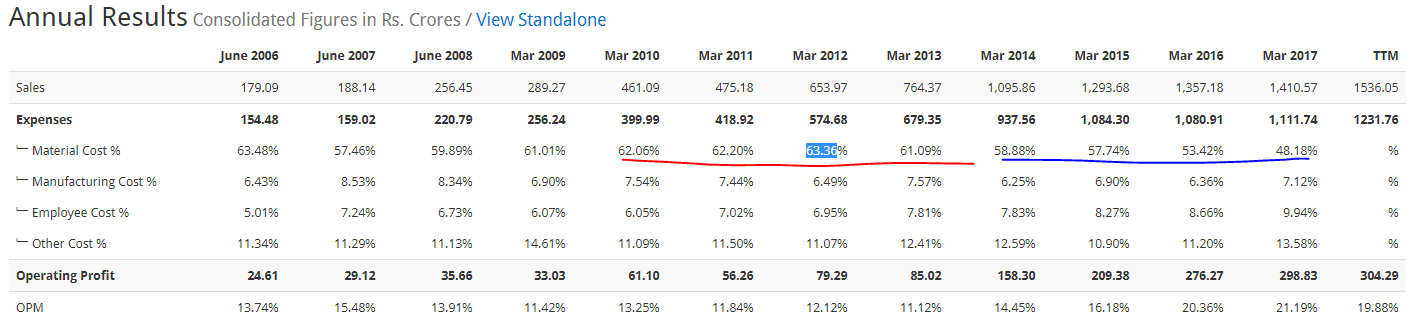

Granules raw material is derriavative of crude oil. Between year 2011 to 2013 and most of 2014, the crude was above $110. In year 2015, 2016 and 2017, it was hovering around range of $40 to $55. Look at the trend of Material cost and margin. Do remember during these years, Granules product composition has also changed significantly. Now more contribution from high margin products compared to low margin API’s.

With Crude oil going up, I think it will impact the margins unless company can pass on to customers.

Can the margins go below 16% if Crude stays above 80 to $90 range? What’s the probability? Your thoughts please

I have read at least 6/7 conference call details and I have not heard management worried about oil prices. Of course, when Oil prices go down, they benefit, but it is compensated when oil price go higher, as is the case now.

I have heard management talking about passing on the higher cost to the client. Although, there may be a delay in passing, eventually, I think, they would recover the higher cost.

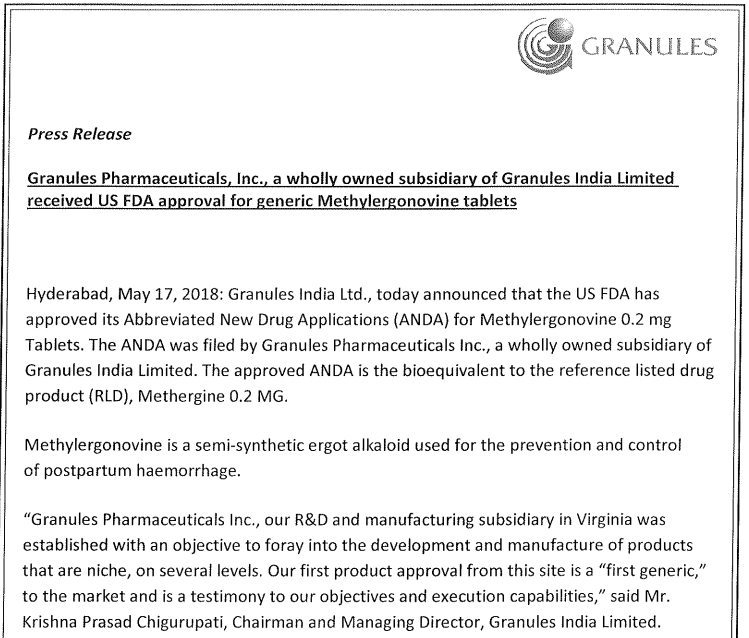

Granules has informed that the US health regulator has issued Establishment Inspection Report (EIR) after audit of its Telangana facility.

“The United States Food and Drug Administration (USFDA) has issued Establishment Inspection Report (EIR) for the company’s Jeedimetla facility located at Hyderabad, Telangana, India,” Granules said in a BSE filing.

The facility was inspected by the USFDA in March 2018 and there was one observation during the inspection. Granules had responded to the observation within the stipulated time frame.

Jeedimetla facility manufactures active pharmaceutical ingredients (APIs) and pharmaceutical formulation intermediates (PFIs).

The USFDA issues an EIR to the establishment that is the subject of an FDA or FDA-contracted inspection when the agency decides to close the inspection.