very disappointing to say the least! clearly Pharma bull run is over for the time being.

Disc: Invested

very disappointing to say the least! clearly Pharma bull run is over for the time being.

Disc: Invested

Granules QIP has closed. They have sold 2.47,54,792 shares at 121.25 per share for a gross amount of 300 cr.

BSE document link -

http://www.bseindia.com/xml-data/corpfiling/AttachLive/2bf1d081-b7f6-4c58-b1cf-e62799cc934c.pdf

Motilal Oswal report on Granules -

Granules has got the approval for Prasugrel and they seem prepared to launch it anytime. It would be interesting to see how this first launch goes.

MOSL is promoting this stock aggressively.

Motilal Oswal comes out with 100 bagger study and then goes out and promotes aggressively the stock listed in that study … I am sure it may be just a coincidence

“Be fearful when others are greedy and be greedy when others are fearful”-- Easy to say, difficult to implement. Happy Diwali guys and wish more fortune during the year.

Discl. Recently exited (small allocation + no time to track ;no other reason)

2017 Q2 Results are out.

Results are okay… nothing exceptional. Looks like we need to wait till Q3 results.

Investor earnings call -on 10th NOV.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=bc1b1ad1-2c54-41fb-879f-3e0cc3928e93

Repeat performance requested from you for summary of con call.

Highlights of Management interview with CNBC:

The short-term uncertainty with respect to the Omnichem JV is unfortunate. It is probably the cause for Granules stock price to drift down post-earnings.

thanks for the interview link. For me i heard 3 key points in the interview.

I think all 3 are positive moves for the company, although in the past for me constant dilution of equity by either QIP or Warrants to promoters has been an issue. The quality of the business was never a question due to the multiple growth levers available. If the mgmt delivers on the above 3 statements then there is scope for outperformance that many have been expecting from Granules.

Does anybody know the amount equity dilution since FY17 till now as a result of QIPs? (I recall they wanted to raise 500Cr via QIP post FY17…)

This is 11%. So I guess per guidance, all we can expect is an EPS increase of about 9-10% for FY18.

Q2 Concall Transcript

http://www.granulesindia.com/uploads/3974GranulesIndia-Earnings-Nov10-2017.pdf

Market size of Metformin ER tab? From which facility? Market has ignored this ANDA, why?

Promoter pledging has reached 78% now. Granules USA was supposed to have 1ANDA approved last month & another by March18.

Despite larger indices are southward due to external / internal reasons, few scrips have managed to remain in green / stable but our company couldn’t hold despite bulk of good news in last 8-10 days

Does any one feel that to keep the average cost of acquisition down, the prices are managed. I don’t have proof or even don’t doubt integrity of promoters.

Anyone having similar view with more documentary proof are welcome

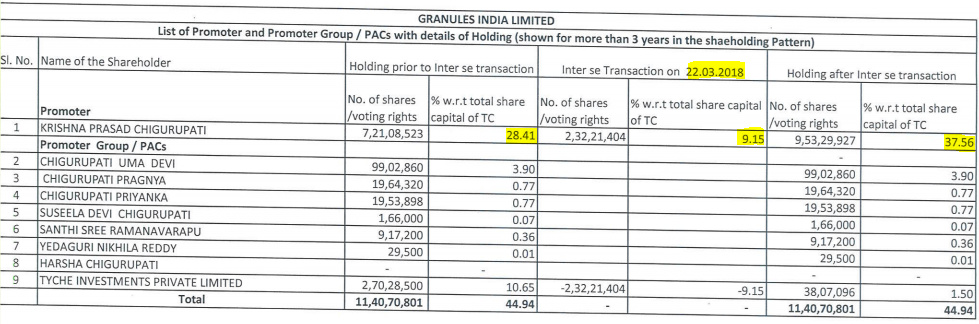

I think promoters have rejigged their shareholding and I believe Promoters have bought shares from other group company. But it looks like they have taken a huge loan as shown by below screenshot from the screener.in.

If the market corrects further, which seems more probable now, promoters, who has pledged considerable shareholding may face trouble as they have to either pledge more and more share or sell shares in the market at a depressed price.

I do not remember exactly, how much promoters shareholding is pledged, but I think it will be substantial now taking into account that has pledge shares worth 784 cr at least. In my view this is negative for the company as a further correction in price could trigger force sell (may or may not).