Granules India Ltd has received eleven observations from Infarmed, the Portuguese drug

regulator, for its facility located at Gagillapur, Telangana. These observations were issued by Infarmed after it conducted a renewal inspection on the company’s Gagillapur facility, which manufactures pharmaceutical formulation intermediates (PFIs) and finished dosages (FDs).

“The company has initiated necessary and preventive action plan within the stipulated time. It will also be requesting the Infarmed for re-inspection of the Gagillapur facility at the earliest. The company is committed to comply with all the required regulatory requirements and follow the best practices of the industry. The company acknowledges the observations as area of continuous improvements,”

It seems like an irony that FDA cleared inspection has met with 11 obs fm portugal authorities. And the price today seems to take this harshly (I know the voting vs weighing machine theory but still the news has been viewed serious)

Either Granules materially altered (or became lax post FDA ins.) their functioning at the plant or Portugal has stricter norms? Both seem less likely. Am I missing seeing something here?

Also, if some experienced members may share, is there a case wherein pharma facilities’ areas are demarcated country wise? (seems unlikely to me but just want to understand better)

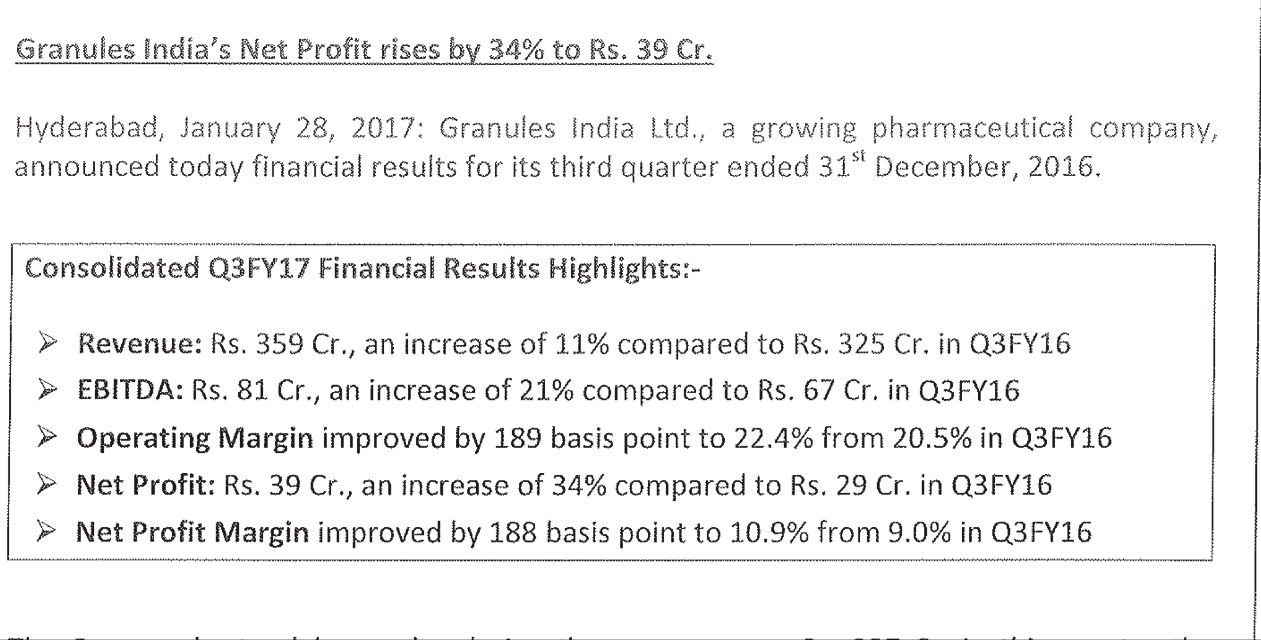

The headline is slightly misleading as the worst case scenario is 28cr for a quarter. They have suspended sales In Portugal from Granules. I didn’t understand why there is a confusion regarding eGMP certificate. Overall minor hit to revenue/PAT but slightly higher hit on clean regulatory record.

Any idea when equity dilution of about 10% due to promoter warrants will be complete and its status ?

Did they stop manufacturing only to Portugal or entire Europe which brings the question does portugal has a different regulator from Europe ?

The Vizag plant which received 7 observations is continuing sales. The mgmt said “We also produce only intermediates in that plant so there is no effect on sales and there is no impact on revenues”. I have a question here. Does impact varies depending upon whether they manufacture API, CRAMPS or formulations in a plant ? Can some pharma expert enlighten on this.

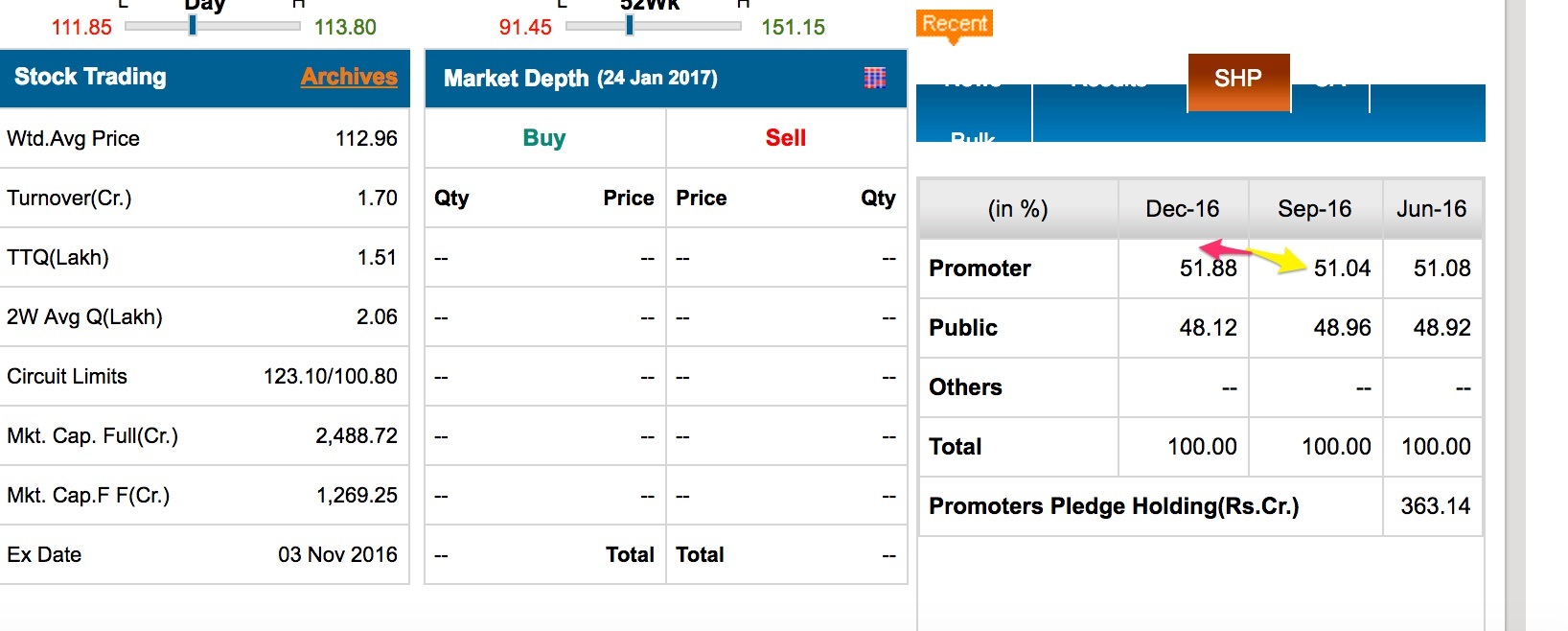

Looks like promoter stake slightly up with insider buying. Good signs?

Name of Person Category of Person * Securities held pre Transaction Securities Acquired / Disposed Securities held post Transaction Period ## Mode of Acquisition # Trading in Derivatives Reported to Exchange

Type of Securities ** Number Value Transaction Type Type of Contract Buy Value (Units~) Sale Value (Units~)

Ramanavarapu Vidya Promoter 422604 (0.19) Equity Shares 1450 1.52 Lakhs Acquisition 424054 (0.19) 10/01/2017 10/01/2017 Market 18/01/2017

Priyanka Chigurupati Promoter 1947898 (0.88) Equity Shares 2500 2.62 Lakhs Acquisition 1950398 (0.88) 10/01/2017 10/01/2017 Market 12/01/2017

Pragnya Chigurupati Promoter 1959520 (0.89) Equity Shares 4800 5.01 Lakhs Acquisition 1964320 (0.89) 10/01/2017 10/01/2017 Market 11/01/2017

Gagillapur unit observations by Portugal authority - clarified in ConCAll by Granules management that the observations were quite procedural and nothing realted to quality and Granules have taken measures on that already and expect the Portugal authority to re-inspect in next 1-3 days. They expect these to be cleared.

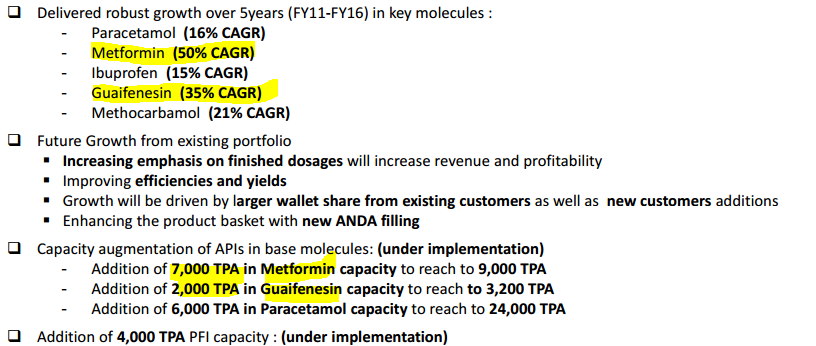

Capacity addition (under implementation) is Metformin and Guaifenesin is a high growth CAGR business and no more capacity expanision highlighted for ibuprofen.

Still a student.

Still a student.