Fair argument but I don’t see any reason why Mr Market is going to pay premium of more than 30 PE for a company like Granules… It only has an acceptable 27~ 30% growth factor going for it in 2016 & 2017.

Other trigger points for Granules is the acquistion Auctus & the collabration with Omnichem slated to start contributing towards EPS & margin enhancement from next year.

Hi Amit, Omnichem JV will contribute around Rs. 250 crs to GI’s top line. By the time this JV is fully operational it could as be an addition of just 10% of sales. Not huge but definitely helps.

Disc: Invested.

@Rajesh_R At full capacity omnichem joint venture will create 550 crores…probably in FY18 or FY19 which will be more than 20% and will contribute significantly to profit as margins are likely to be better. One reference is below.

http://fundamental-picks.in/2015/08/granules-india-ltd-a-healthy-wealthy-particle/

You can also refer to various research reports.

1 Like

@raj This is a 50:50 JV so you have to divide 550 by 2.You can refer to Q3 concall transcript as well (I made a comment earlier on the same topic, you can check that one too)

Thanks Anindya for correcting me. I missed the point.

Also declared second interim dividend of Rs. 0.15 per share.

Disc - Invested

3 Likes

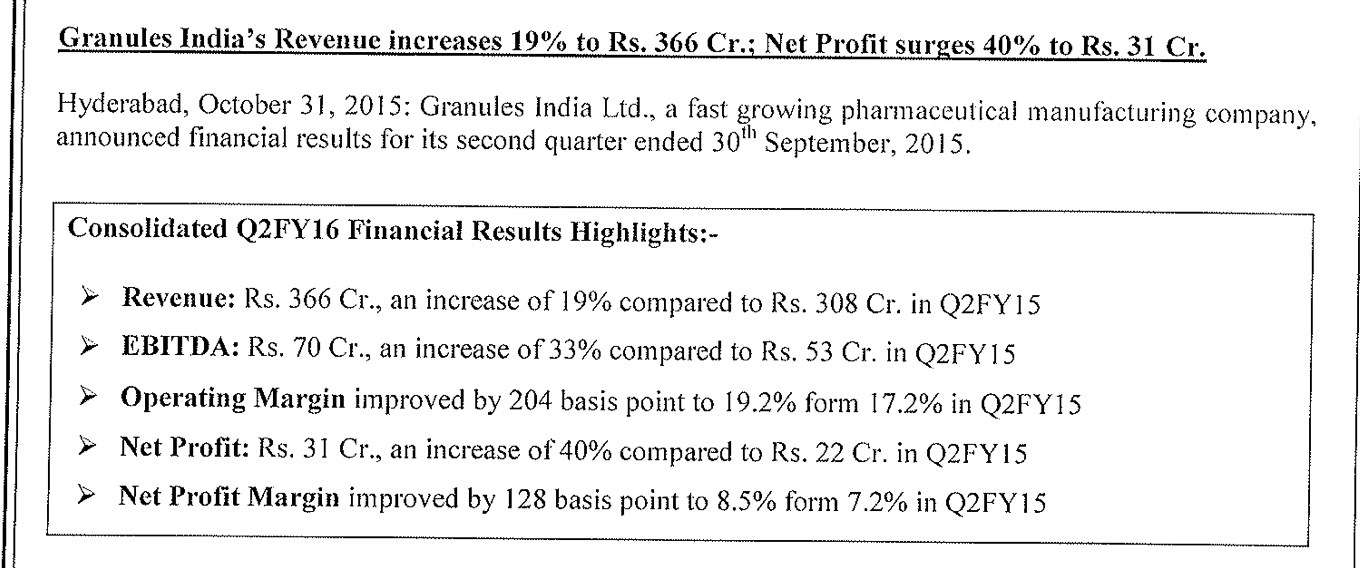

Good consolidated results but a slightly weak standalone results especially on sequential basis.

Promoters have converted warrants to shares. Will need to see the market reaction to that. The price is Rs 85 but that was known to the market. The conversion coming ahead of the schedule does show the confidence of promoters.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=9fd8bcb5-284e-4c74-8c1c-ca1ed18af8e8

Anyone has got any idea of the concall.

Disclosure: Invested

Good numbers.

Can anyone help me with a doubt?

In the April concall, management had mentioned that the total debt (including working capital) is 498cr but in balance sheet long term and short term borrowings were 245cr and 115cr. These add to 390cr. Where to read off the additional 108cr debt?

I think you are looking at standalone numbers.

Were they also talking about standalone numbers?

Also, if you check BS schedule of other current liabilities it also has 'Current maturities of Long term borrowings".

Maybe things will match then.

Some fiis r entering into granules, need to see how they react with results showing gud numbers!

1 Like

Promoter converted his warrants leading to 41 lakhs of shares.

http://www.moneycontrol.com/stocks/stock_market/corp_notices.php?autono=2176301

Granules deliverables is at approx. 30% (source Moneycontrol). How is this to be interpreted? Anyone please.

my guess is that granules will do an eps of 6 for the yr fy 16,thus discounting at current price 24.5times.by looking at the current numbers can they do an eps of 7.8 for fy 17 implying a growth of 30% in which case granules gets discounted 18.8 times.am i underestimating or overestimating or am i right? disc invested at lower levels

when is the con call?

Accumulate Granules India; target of Rs 174:Emkay

Their eps estimates are way too optimistic though

Disc: Invested

It is done. Audio transcript is available on research bytes.