Overall the results look quite decent. Despite the BECL write-off the EPS of Rs. 16.84 for FY19 is a positive surprise. Curious about the other income of ~ Rs. 105 cr. What are your views about the results @dakalia.

Good for longterm 2-3 years prospective.Once the power sector picks up it can give u multiple returns.

Out of the total 105 crores Other Income, 94 crores is one-time affair.

However, result seems good to me.

Hi is anyone attending GIPCL AGM - 20th September 2019 12:00pm onwards at Vadodra?

1 Like

GIPCL is nodal agency for carrying out this mega project. Impact of this on GIPCL. If anyone can understand?

1 Like

GIPCL will be a park developer like Adani and NTPC. Essentially each of them are also likely to key tenants. GIPCL will perhaps do 1500mw over 5 years. The equity portion of the project can easily be funded from cash profit of ~400crs (i.e. after deducting dividend of approx 50crs). Other investors in GIPCL park is likely to be the other Gujarat PSUs. Again these are ambitions, not necessarily it will all happen. The good is that the share of renewables will keep rising in GIPCL cashflow, from approx 30%+ now to 50% by Fy23.

1 Like

Comments post GIPCL H1/Fy21 B/S

Approx 450crs debt and 420crs cash after investment of 120crs in cwip.

Cash PAT of 207crs in H1/Fy21 vs 213crs H1/Fy20.

Should do 450crs cash PAT in full year.

Mcap is 1030crs.

EV/Cash PAT is less than 3 years.

Debt could rise if they set up solar parks very aggressively, say 300mw/ annum. Infact that will be a positive as the share of renewables climbing is likely to bring investor attention (30% currently, ~ 50% in Fy23). If they continue doing only 100-150mw solar/annum, then the b/s will remain unlevered.

2 Likes

GIPCL is a Vadodara-based listed public limited company engaged in the business of power generation with an installed capacity of 1,184.40 MW as on June 30, 2023. It was incorporated in 1985 and is promoted by the state government undertakings of Gujarat, viz., GUVNL, GACL and GSFC. GIPCL operates two gas-based power plants in Vadodara, VS-I and VS-II aggregating 310 MW, two lignite-based power plants in Surat, SLPP-I and SLPP-II aggregating 500 MW, a 5-MW solar power plant in Surat and 257-MW solar power plants in various parts of Gujarat (aggregate solar capacity of 262 MW) along with wind capacities of 112.40 MW as on June 30, 2023.

Future Growth Plans

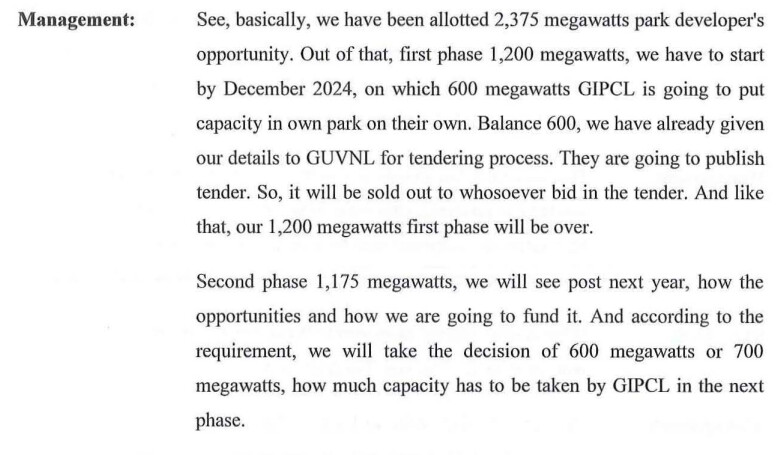

- A leasehold land was allocated in the Great Rann of Kutch near Khavda for setting up a 2375 MW Renewable Energy (RE) Park. This park is part of a larger 30 GW RE Park planned near the International Border in the Great Rann of Kutch.

- The Ministry of New & Renewable Energy (MNRE) has approved the entire RE park under the Ultra Mega Renewable Energy Power Project (UMREPP) Mode-8, allowing it to benefit from Central Financial Assistance (CFA).

- Major work orders for developing RE park infrastructure, such as pooling sub-stations, internal roads, and drains, have been issued, and work on the site is in progress.

- The entire capacity of the RE Park is expected to be completed by December 2026.

- The company successfully bid for a 600 MW Solar Power Project under the Greenshoe option of Gujarat Urja Vikas Nigam Limited (GUVNL) Tender. In May 2023, they received the Letter of Intent (LoI) for the project from GUVNL.

- Tata Consulting Engineers has been appointed as the Project Management Consultant for the 600 MW project. Basic engineering and tendering activities have been initiated.

- The company signed a Power Purchase Agreement (PPA) with GUVNL at a tariff of Rs. 2.73 per unit on August 11, 2023.

- Additionally, the company has signed a PPA for a 500 MW Solar Power Project at Khavda with GUVNL at the same tariff of Rs. 2.73 per unit on October 30, 2023.

Liquidity: Strong GIPCL has sound liquidity position marked by healthy cash accruals, availability of adequate amount of unencumbered cash and bank balance, negligible utilisation of fund-based working capital limits and low average collection period on account of timely realisation of payments from GUVNL, which has a strong financial risk profile and is the largest off-taker of GIPCL. During FY24, GIPCL has sufficient cushion in its scheduled debt repayment of around ₹75 crore against its envisaged GCA. It has adequate unencumbered cash and bank balance to the tune of ₹282 crore as on March 31, 2022 and ₹373 crore as on June 30, 2022. GIPCL has fund-based working capital limits of ₹144.15 crore, average utilisation of which was negligible at 0.64% from July 2022 to June 2023, whereas it has non-fund-based working capital limits of ₹528.71 crore, average utilisation of which was 15.13% from during the same period.

Large upcoming capital expenditure plans in the renewable energy segment GIPCL has been awarded land for implementing 2,375 MW solar park in Khavda, Kutch, which is to be developed over the next 4-5 years. However, as informed by the management, GIPCL plans to develop around 50% of this capacity by itself, while the balance 50% would be sub-let to other developers. GIPCL currently has operational capacity of 1,184.40 MW. CARE Ratings notes that with the completion of proposed solar projects, GIPCL would double its operational capacity, of which majority would be renewable capacity.

Parentage of GUVNL, GACL and GSFC having strong financial risk profile and low counter-party credit risk as GUVNL is GIPCL’s largest off-taker The promoters of GIPCL, state public sector undertakings (PSUs) of Gujarat, viz., GUVNL, GACL and GSFC, have a strong financial risk profile. The low counter party credit risk is signified by GIPCL’s long-term PPAs with GUVNL and its subsidiaries for the purchase of power from its lignite-based (500 MW under SLPP-I and SLPP-II), gas-based (165 MW under VS-II), wind power (112.40) and solar power plants (182 MW) and with SECI for power off-take from its solar power plants (80 MW). It also has an MoU with GUVNL, GACL and GSFC for supply of power being generated by VS-I (145 MW).

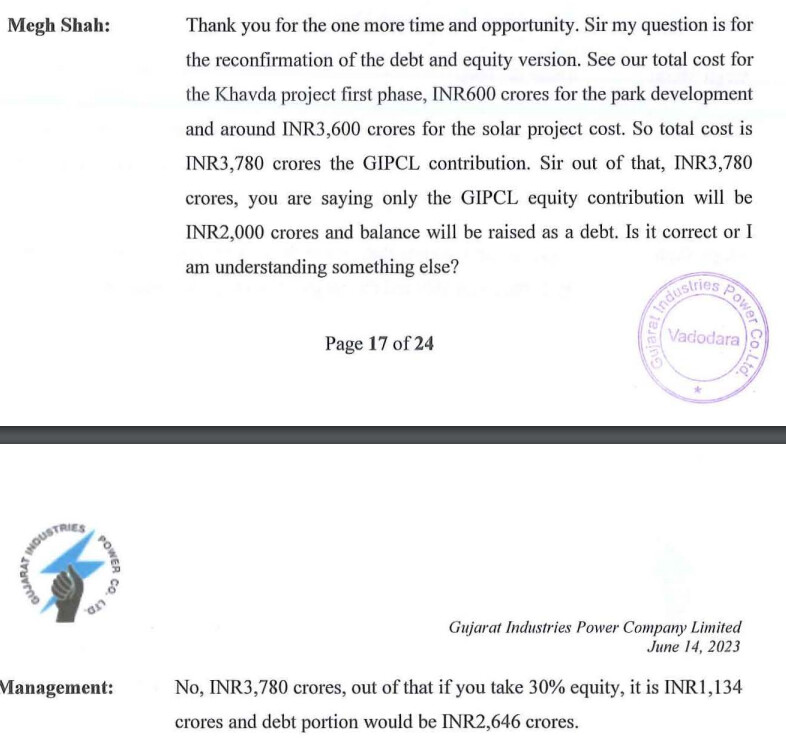

As articulated by the management, the total cost of developing the solar park is estimated at around ₹1,353 crore and the total cost of developing the solar power projects of 1,175.00 MW (around 50% capacity) is estimated at around ₹5.50 crore per MW. Out of the total estimated solar park development cost of ₹1,353 crore, 30% would be funded through subsidy from the Ministry of New and Renewable Energy (MNRE), whereas 40% would be funded through user development charges (UDC) from the project developers. Balance cost is expected to be funded in a debt-to-equity ratio of 20:80. The estimated cost for developing the solar power projects of 1,175.00 MW (around 50% capacity) is expected to be funded in a debt-to-equity ratio of 80:20. Entire equity requirement for the project would be met through internal accruals. GIPCL is exposed to significant project execution risks associated with these projects, including any time and cost overruns. CARE Ratings will continue to monitor the ability of GIPCL to complete this project within the envisaged time and cost parameters and subsequently generate envisaged returns, which will be crucial from the credit perspective.

Key weaknesses Subdued operating performance of gas-based power plants Although the gas-based plants of GIPCL have become debt free, the operations of these plants have been affected due to uncertainty prevailing over supply of natural gas at competitive rates. GIPCL operates its gas-based power plants based on the availability of natural gas under the APM. Earlier, decline in the operating efficiency of gas-based power plants was mainly due to the lower off-take of power from VS-II plant by GUVNL since it operates on a need-based basis. However, the operating performance of VS-I has also been affected due to high natural gas prices. VS-I did not operate in FY23 and Q1FY24 and its PLF in FY22 was 29%.

June 2023 Concall Notes:

- Financial Results: Good revenue and profitability in the March quarter, with normal income and varying Plant Load Factor (PLF) across divisions.

- Insurance Claims: Expecting insurance claims for material loss and loss of profit.

- Renewable Division: Revenue and EBITDA were INR 266 crores and INR 231 crores, respectively. Development of a 600-MW solar project in Khavda is underway, with commercial production expected in November 2024. The estimated cost is over INR 5 crores per MW, and total capex is INR 6,000 crores. The first 600 MW of the solar project is also expected by November 2024. The company is exploring various funding options and expects a post-tax equity IRR of around 12%.

- Non-Renewable Division: Revenue and EBITDA were INR 1,082 crores and INR 269 crores, respectively. The gas plant will restart when gas prices become favorable. No plans for new thermal power plants.

- Dividend Policy: Following the Gujarat Government’s policy, requiring a minimum of 30% of PAT or 5% of net worth as dividends.

- Lignite Production: Based on the power stations’ requirements.

- Solar Capacity: Confident in completing 1,200 MW by December 2024.

November 2022 Concall Notes:

- Capex: Development of the Khavda project in phases with a total capacity of 2,375 MW. Total CAPEX around Rs. 1,100 crores, and funding through a 70:30 debt-equity mix.

- New Products: Exploring opportunities in Green Hydrogen and a mix of wind and solar.

- Guidance: Capacity addition at Khavda Phase-I is 50% of 600 MW. Revenue expected to be flat next year but increase thereafter. Gas-based plants viable at lower gas prices.

- Operations: Lower commercial availability due to maintenance shutdowns. Plans to restart gas plants once prices stabilize.

- Khavda Project: Park development in progress, focusing on a pooling substation for power evacuation. Revenue depends on tariff rates with GUVNL or SECI.

June 2021 Concall Notes:

- Capex and Projects: Development of 1500-1600 MW solar projects, with a total capex of Rs. 6,500-7,000 Crores over five years. The Khavda project will have a capex of Rs.6500-7000 crores for 1500-1600 MW capacity.

- Solar Projects: Awarded 2375 MW capacity at Khavda, to be developed in phases by December 2024.

- Capex and EBITDA: EBITDA for thermal stations at around Rs. 290 Crores, and for renewable, it is Rs. 190 Crores.

- Ownership and Market Capitalization: Focus on increasing transparency and sharing growth plans to improve market value.

- Lignite and Thermal Plants: Started in 1993 with a gas-based plant, expanded to include lignite and renewable sources. Sufficient captive lignite mines to run stations at 80% PLF.

3 Likes

1 Like