Ameen

Is it right time to invest in gipcl?

CURRENT M/CAP: 1500 Crores

EXISTING CAPACITY: (As of 31/3/18: 1009.4 MW)

Gas Based: 310 MW (Gas Supply Dependent on GAIL & GSPL)

Lignite Based: 500 MW (Captive MIne)

Wind Energy: 112.4 MW (Installed during FY 16-17 in phased manner)

Solar Energy: 87 MW (80 MW new capacity installed during FY 17-18)

EXPANSION: 75 MW Solar Power Plant to be installed during FY 18-19.

Therefore by 31/3/19 Projected Total Capacity will be atleast 1084.4 MW

DEBT POSITION:

As at 31/3/16: 431.70 Crores

As at 31/3/17: 376.58 Crores (No debt increase inspite of huge capex of 661 Crores during FY 16-17)

Plans to reduce debt further.

SALES:

Almost all electricity is sold to GUVNL (One of the Promoter of GIPCL)

2015-16: 4046.597 Million Units Sold @ Rs.3.3257 p.u.(Approx)

2016-17: 4031.365 Million Units Sold @ Rs.3.2341 p.u.(Approx)

Sales were lower due to Gas Supply issues at Vadodra Station 2 (165MW) and expiry of PPA with GUVNL.

At present Spot Power Prices were Rs. 3.98 p.u. on April 2018. And I believe Spot prices will not fall from here as already there is lot of NPA in power sector and govt. do not wants to increase it further.

POFITS:

FY 2015-16: PAT 187 Crores (Depreciation:112 Crores; Cash Profits:300 Crores(Approx)

FY 2016-17: PAT 251 Crores (Depreciation:125 Crores; Cash Profits:375 Crores(Approx)

Therefore 350-400 crores cash profits are reasonable for solar capacity addition without increase of Debt.

ADD-ONS:

GIPCL has 24.36% stake in Bhavnagar Energy Co. Ltd.(500 MW Lignite Based Capacity) whose results are not included in GIPCL Balance Sheet.

Current Dividend Yield is around 2.78%(Better than keeping idle funds in S/B Account Considering the tax benifit on dividends). Further, it has consistency in paying dividend regularly at same rate, irrespective whether its earnings increase or decrease.

At 1500 crore M/Cap it seems a safe long-term bet. Not necessary a multi-bagger but returns better than atleast Nifty can be expected.

1 Like

Great to see a post on this company. Despite a very stable performance, the stock has under-performed for a while. Maybe Q4 results can be a positive trigger for the counter.

Disc: Invested

SJ

Even if the results are average (as expected), what is the downside risk from here.

Adani Power M/Cap 9200 Crores

Capacity 10,000 MW

Debt 50,000 Crores

Means around Rs.5-6 Crores /MW Valuation.

And GIPCL at Rs.1.5-2 Crore/MW Valuation.

What worse can you expect from this level?

1 Like

I agree and if you look at even NTPC its close to 5-6 cr/MW. Why do you think is this company so undervalued? Are we missing something.

SJ

1 Like

As per some insider sources may be ICICI Prudential Life Insurance Co. is selling…though I am not very sure about it…

Gas Based Power plants (310 MW) have not been doing well.

Viability of setting up of Wind Energy and Solar Energy Plants, in India is also not clear. Currently, most of the plants are running at around 15-20% CUF,ie. 1 MW produce roughly around 1.5 million units of electricity.

Do share any information if you get from some where…

3 Likes

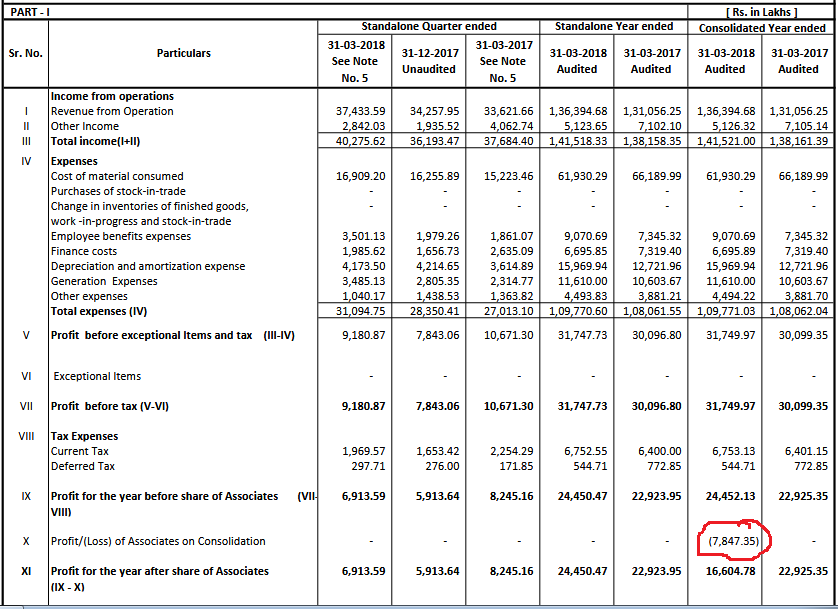

It is the share of losses in its~25% associate company, Bhavnagar Energy co. Ltd. I am not sure but, seems like the company has just commenced its operations.

SJ

are there any more details available why BECL is in loss?

Commercial Operations of Bhavnagar Energy Company Limited commenced in the month of March 2017 and it is the first year of operation post capitalization. As per Equity method, the share of loss of Associate company viz. Bhavnagar Energy Company Limited (BECL) has been captured in the Consolidated Audited Financial Results for the year ended 31st March 2018.

Therefore, carrying value of Investment in BECL has come down from 206.08 crores to 127.61 crores.

2 Likes

I just found credit rating of BECL. It is rated CARE D. It gives some insights into the current situation. We will have to wait to see if the overall performance improves.

http://www.careratings.com/upload/CompanyFiles/PR/Bhavnagar%20Energy%20Company%20Ltd-10-26-2017.pdf

2 Likes

Are financial results of BECL available?

BECL has been merged with Gujarat State Electricity Corporation (GSECL) vide Govt. of Gujarat Order dated 27/8/18, at ZERO VALUE. GMDC has booked Rs.297.65 crores as a one-time loss on Q2 FY18-19. Probably GIPCL will also book its loss on current quarter. Q2 results of GIPCL will be declared o 1/11/18.

Maybe GIPCL will make its bottom very soon. Lets wait and watch.

1 Like

@dakalia GIPCL has also written-off the investments in BECL, as you had indicated. I think BECL’s merger is positive for GIPCL as BECL had a drag on its financials. What are your views on this?. By the way the Q2 results (ex BECL) were good. EBITDA for Q2FY19 came in healthy at ~42% and revenue growth yoy was 12.5%.

Disc: Invested

SJ

1 Like

Yes results of Q2 was good and writting off BECL investment is definitely prudent move by management.

Now if we can get information on PLF for all its power plants- 310MW gas based, 500 MW lignite based, 112.4 MW wind based and 80 MW solar based capacity.

Further, what is the progress of 75 MW solar based capacity it has planned to add up in FY18-19.

GIPCL valuations looks quite cheap compared to its peers and replacement cost, however almost all the Public Sector Undertakings are trading at huge discount to there intrinsic value, so I personally will just HOLD on to my investment and will not make fresh investments till there is more clarity.

2 Likes

@dakalia what are your views on the counter now. The PLF for Vadodara and Surat I unit is likely to be lower in the near future. The stock is currently trading at 2x FY19 FCF, which seems attractive. I stumbled upon this Q3 result review by Emkay

Regards

SJ

@jajushobhit I guess PLF is likely to improve post elections when manufacturing activity picks up.

All thermal stations are paid by GUVNL on Cost Plus Basis therefore with increase in PLF operating profits will increase.

As far as Wind and Thermal projects are concerned, the company had pumped in 1000 crores (650cr for wind and 350cr for solar) but any major impact is not visible in the revenue figures.

Further, the company is investing 350cr more on 75mw solar capacity.

What kind of ROI is coming from above investments is a big question mark.

1 Like

@jajushobhit Sir it apparently seems that GIPCL is dumping money by making aggressively low bids for solar power projects.

EPC cost payable to BHEL for setting up 75 MW solar power plant at Charanka, Gujarat is Rs.305 crores whereas tariff as low as Rs 2.67 / kWH has been quoted by the company in the auction.

Now this is not the end of story. The company is further intending to dump more money by inviting tenders for setting up 150 MW of solar capacity.

https://mercomindia.com/gipcl-tenders-200-mw-wind-gujarat/

I call upon any expert in this forum to help us understand the kind of ROI’s been made in these kind of investments ?

2 Likes

Thanks for the update Kushal. I am not an expert on solar power and will not be able to comment. However, it is difficult for me to believe that the company will be making money by bidding at Rs. 2.67 for solar power projects.

Regards

SJ